- Page 1 and 2:

9Annual report 2009

- Page 3 and 4:

9Annual report 2009Management repor

- Page 5 and 6:

9Management report

- Page 7 and 8:

Group profi leSIMPLIFIED GROUP STRU

- Page 9 and 10:

Group profi leQUALITY OF RISKS Dexi

- Page 11 and 12:

In accordance with the agreement wi

- Page 13 and 14:

2009 and early 2010 highlightsExit

- Page 15 and 16:

2009 and early 2010 highlightsCreat

- Page 17 and 18:

Corporate governanceIntroduction: t

- Page 19 and 20:

Corporate governanceThe European Ad

- Page 21 and 22:

Corporate governanceNAMEPIERREMARIA

- Page 23 and 24:

Corporate governanceNAMEROBERTDE ME

- Page 25 and 26:

Corporate governanceNAMESPECIALISTC

- Page 27 and 28:

Corporate governanceNAMEKOEN VAN LO

- Page 29 and 30:

Corporate governanceNew directors a

- Page 31 and 32:

Corporate governanceConsidering tho

- Page 33 and 34:

Corporate governancemade and the fi

- Page 35 and 36:

Corporate governanceDIRECTORS’ AN

- Page 37 and 38:

Corporate governanceOperation and a

- Page 39 and 40:

Corporate governanceThe Appointment

- Page 41 and 42:

Corporate governanceResponsibilitie

- Page 43 and 44:

Corporate governanceVariable compen

- Page 45 and 46:

Corporate governancetional entities

- Page 47 and 48:

Corporate governance• It identifi

- Page 49 and 50:

Shareholder informationStock market

- Page 51 and 52:

Shareholder informationPRINCIPAL DE

- Page 53 and 54:

Human resourcesAGE PYRAMID> 5955-59

- Page 55 and 56:

Sustainable developmentThe 2009 Dex

- Page 57 and 58:

Risk managementIntroductionIn 2009,

- Page 59 and 60:

Risk managementThe Rating Committee

- Page 61 and 62:

Risk managementAsset qualityBy the

- Page 63 and 64:

Risk managementBond portfolioDexia

- Page 65 and 66:

Risk managementThis good performanc

- Page 67 and 68:

Risk managementRisk and control sel

- Page 69 and 70:

Risk managementECONOMIC CAPITALBY T

- Page 71 and 72:

Financial resultsPreliminary notes

- Page 73 and 74:

Financial resultsSolvency31/12/08 3

- Page 75 and 76:

Financial resultsAssetsLoans and ad

- Page 77 and 78:

Activity and results of the busines

- Page 79 and 80:

Activity and results of the busines

- Page 81 and 82:

Activity and results of the busines

- Page 83 and 84:

Activity and results of the busines

- Page 85 and 86:

Activity and results of the busines

- Page 87 and 88:

Activity and results of the busines

- Page 89 and 90:

General information3. Overview of t

- Page 91 and 92:

General informationAll the above-me

- Page 93 and 94:

General information4.5. Dexia banka

- Page 95 and 96:

General information6.3. Notificatio

- Page 98 and 99:

Consolidated balance sheet ........

- Page 100 and 101:

Consolidated balance sheetManagemen

- Page 102 and 103:

Consolidated statementof incomeMana

- Page 104 and 105:

Management reportConsolidatedfinanc

- Page 106 and 107:

Consolidated statementof comprehens

- Page 108 and 109:

Notes to the consolidated financial

- Page 110 and 111:

Notes to the consolidated fi nancia

- Page 112 and 113:

Notes to the consolidated fi nancia

- Page 114 and 115:

Notes to the consolidated fi nancia

- Page 116 and 117:

Notes to the consolidated fi nancia

- Page 118 and 119:

Notes to the consolidated fi nancia

- Page 120 and 121:

Notes to the consolidated fi nancia

- Page 122 and 123:

Notes to the consolidated fi nancia

- Page 124 and 125:

Notes to the consolidated fi nancia

- Page 126 and 127:

Notes to the consolidated fi nancia

- Page 128 and 129:

Notes to the consolidated fi nancia

- Page 130 and 131:

Notes to the consolidated fi nancia

- Page 132 and 133:

Notes to the consolidated fi nancia

- Page 134 and 135:

Notes to the consolidated fi nancia

- Page 136 and 137:

Notes to the consolidated fi nancia

- Page 138 and 139:

Notes to the consolidated fi nancia

- Page 140 and 141:

Notes to the consolidated fi nancia

- Page 142 and 143:

Notes to the consolidated fi nancia

- Page 144 and 145:

Notes to the consolidated fi nancia

- Page 146 and 147:

Notes to the consolidated fi nancia

- Page 148 and 149:

Notes to the consolidated fi nancia

- Page 150 and 151:

Notes to the consolidated fi nancia

- Page 152 and 153:

Notes to the consolidated fi nancia

- Page 154 and 155:

Notes to the consolidated fi nancia

- Page 156 and 157: Notes to the consolidated fi nancia

- Page 158 and 159: Notes to the consolidated fi nancia

- Page 160 and 161: Notes to the consolidated fi nancia

- Page 162 and 163: Notes to the consolidated fi nancia

- Page 164 and 165: Notes to the consolidated fi nancia

- Page 166 and 167: Notes to the consolidated fi nancia

- Page 168 and 169: Notes to the consolidated fi nancia

- Page 170 and 171: Notes to the consolidated fi nancia

- Page 172 and 173: Notes to the consolidated fi nancia

- Page 174 and 175: Notes to the consolidated fi nancia

- Page 176 and 177: Notes to the consolidated fi nancia

- Page 178 and 179: Notes to the consolidated fi nancia

- Page 180 and 181: Notes to the consolidated fi nancia

- Page 182 and 183: Notes to the consolidated fi nancia

- Page 184 and 185: Notes to the consolidated fi nancia

- Page 186 and 187: Notes to the consolidated fi nancia

- Page 188 and 189: Notes to the consolidated fi nancia

- Page 190 and 191: Notes to the consolidated fi nancia

- Page 192 and 193: Notes to the consolidated fi nancia

- Page 194 and 195: Notes to the consolidated fi nancia

- Page 196 and 197: Notes to the consolidated fi nancia

- Page 198 and 199: Notes to the consolidated fi nancia

- Page 200 and 201: Notes to the consolidated fi nancia

- Page 202 and 203: Notes to the consolidated fi nancia

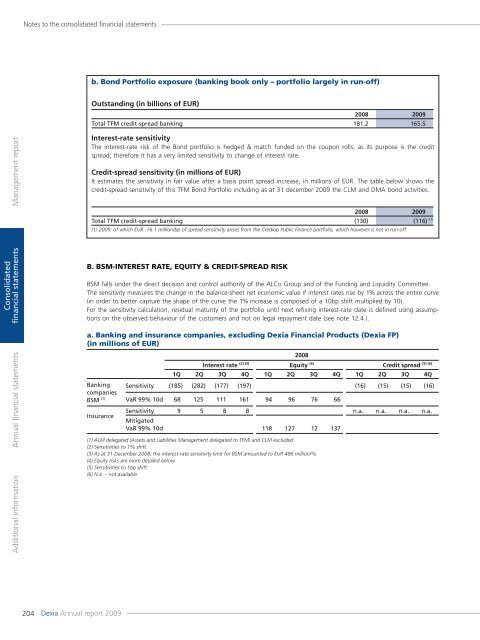

- Page 204 and 205: Notes to the consolidated fi nancia

- Page 208 and 209: Notes to the consolidated fi nancia

- Page 210 and 211: Notes to the consolidated fi nancia

- Page 212 and 213: Notes to the consolidated fi nancia

- Page 214: Statutory Auditor’s reportManagem

- Page 217 and 218: 9Annual financial statementsFINANCI

- Page 219 and 220: SHAREHOLDERS’ EQUITY AND LIABILIT

- Page 221 and 222: Notes to the annualfinancial statem

- Page 223 and 224: Notes to the annual fi nancial stat

- Page 225 and 226: Notes to the annual fi nancial stat

- Page 227 and 228: Notes to the annual fi nancial stat

- Page 229 and 230: Notes to the annual fi nancial stat

- Page 231 and 232: Notes to the annual fi nancial stat

- Page 233 and 234: Notes to the annual fi nancial stat

- Page 235 and 236: Notes to the annual fi nancial stat

- Page 237 and 238: Notes to the annual fi nancial stat

- Page 239 and 240: Notes to the annual fi nancial stat

- Page 241 and 242: Notes to the annual fi nancial stat

- Page 243 and 244: Notes to the annual fi nancial stat

- Page 245 and 246: Statutory Auditor’s report• Wit

- Page 247 and 248: Additional informationGeneral dataN

- Page 249 and 250: Additional informationDexia FP Hold

- Page 251 and 252: Dexia’s annual report 2009 has be