Reports - Mississippi Renewal

Reports - Mississippi Renewal

Reports - Mississippi Renewal

- No tags were found...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

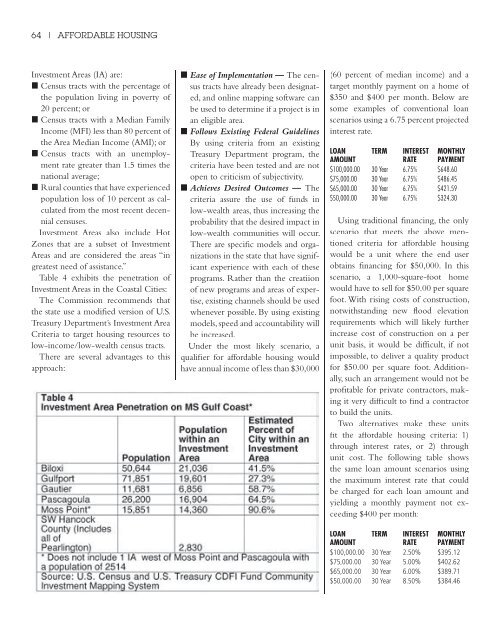

64 | AFFORDABLE HOUSINGInvestment Areas (IA) are:■ Census tracts with the percentage ofthe population living in poverty of20 percent; or■ Census tracts with a Median FamilyIncome (MFI) less than 80 percent ofthe Area Median Income (AMI); or■ Census tracts with an unemploymentrate greater than 1.5 times thenational average;■ Rural counties that have experiencedpopulation loss of 10 percent as calculatedfrom the most recent decennialcensuses.Investment Areas also include HotZones that are a subset of InvestmentAreas and are considered the areas “ingreatest need of assistance.”Table 4 exhibits the penetration ofInvestment Areas in the Coastal Cities:The Commission recommends thatthe state use a modified version of U.S.Treasury Department’s Investment AreaCriteria to target housing resources tolow-income/low-wealth census tracts.There are several advantages to thisapproach:■ Ease of Implementation — The censustracts have already been designated,and online mapping software canbe used to determine if a project is inan eligible area.■ Follows Existing Federal GuidelinesBy using criteria from an existingTreasury Department program, thecriteria have been tested and are notopen to criticism of subjectivity.■ Achieves Desired Outcomes — Thecriteria assure the use of funds inlow-wealth areas, thus increasing theprobability that the desired impact inlow-wealth communities will occur.There are specific models and organizationsin the state that have significantexperience with each of theseprograms. Rather than the creatiionof new programs and areas of expertise,existing channels should be usedwhenever possible. By using existingmodels, speed and accountability willbe increased.Under the most likely scenario, aqualifier for affordable housing wouldhave annual income of less than $30,000(60 percent of median income) and atarget monthly payment on a home of$350 and $400 per month. Below aresome examples of conventional loanscenarios using a 6.75 percent projectedinterest rate.LOAN TERM INTEREST MONTHLYAMOUNT RATE PAYMENT$100,000.00 30 Year 6.75% $648.60$75,000.00 30 Year 6.75% $486.45$65,000.00 30 Year 6.75% $421.59$50,000.00 30 Year 6.75% $324.30Using traditional financing, the onlyscenario that meets the above mentionedcriteria for affordable housingwould be a unit where the end userobtains financing for $50,000. In thisscenario, a 1,000-square-foot homewould have to sell for $50.00 per squarefoot. With rising costs of construction,notwithstanding new flood elevationrequirements which will likely furtherincrease cost of construction on a perunit basis, it would be difficult, if notimpossible, to deliver a quality productfor $50.00 per square foot. Additionally,such an arrangement would not beprofitable for private contractors, makingit very difficult to find a contractorto build the units.Two alternatives make these unitsfit the affordable housing criteria: 1)through interest rates, or 2) throughunit cost. The following table showsthe same loan amount scenarios usingthe maximum interest rate that couldbe charged for each loan amount andyielding a monthly payment not exceeding$400 per month:LOAN TERM INTEREST MONTHLYAMOUNT RATE PAYMENT$100,000.00 30 Year 2.50% $395.12$75,000.00 30 Year 5.00% $402.62$65,000.00 30 Year 6.00% $389.71$50,000.00 30 Year 8.50% $384.46