Galfar Engineering & Contracting (GECS.OM)

Galfar Engineering & Contracting (GECS.OM)

Galfar Engineering & Contracting (GECS.OM)

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

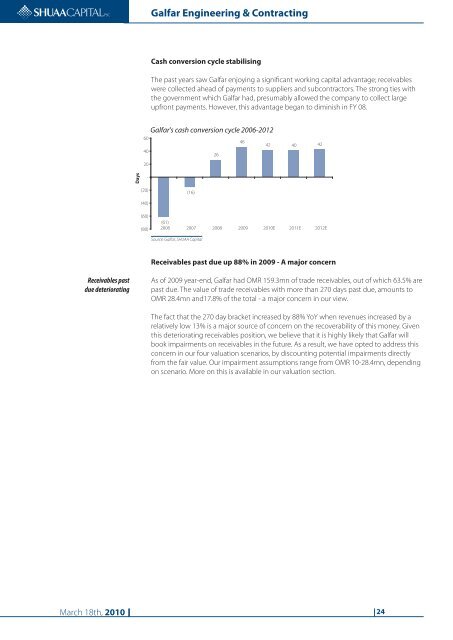

<strong>Galfar</strong> <strong>Engineering</strong> & <strong>Contracting</strong>Cash conversion cycle stabilisingThe past years saw <strong>Galfar</strong> enjoying a significant working capital advantage; receivableswere collected ahead of payments to suppliers and subcontractors. The strong ties withthe government which <strong>Galfar</strong> had, presumably allowed the company to collect largeupfront payments. However, this advantage began to diminish in FY 08.<strong>Galfar</strong>'s cash conversion cycle 2006-2012604642 40 42402620Days-(20)(16)(40)(60)(80)(61)2006 2007 2008 2009 2010E 2011E 2012ESource: <strong>Galfar</strong>, SHUAA CapitalReceivables past due up 88% in 2009 - A major concernReceivables pastdue deterioratingAs of 2009 year-end, <strong>Galfar</strong> had <strong>OM</strong>R 159.3mn of trade receivables, out of which 63.5% arepast due. The value of trade receivables with more than 270 days past due, amounts to<strong>OM</strong>R 28.4mn and17.8% of the total - a major concern in our view.The fact that the 270 day bracket increased by 88% YoY when revenues increased by arelatively low 13% is a major source of concern on the recoverability of this money. Giventhis deteriorating receivables position, we believe that it is highly likely that <strong>Galfar</strong> willbook impairments on receivables in the future. As a result, we have opted to address thisconcern in our four valuation scenarios, by discounting potential impairments directlyfrom the fair value. Our impairment assumptions range from <strong>OM</strong>R 10-28.4mn, dependingon scenario. More on this is available in our valuation section.March 18th, 2010 24