Annual Report 2001 - KSPG AG

Annual Report 2001 - KSPG AG

Annual Report 2001 - KSPG AG

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

76<br />

Consolidated financial statements <strong>2001</strong> of Kolbenschmidt Pierburg <strong>AG</strong><br />

Notes<br />

Accounting principles<br />

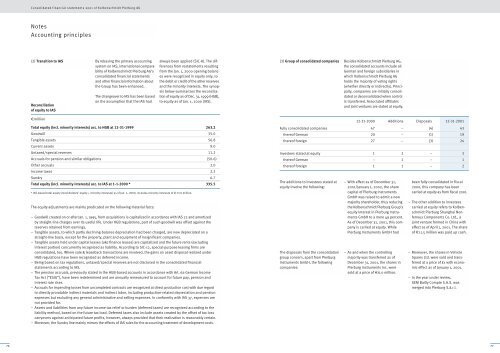

(2) Transition to IAS By rebasing the primary accounting<br />

system on IAS, international comparability<br />

of Kolbenschmidt Pierburg <strong>AG</strong>’s<br />

consolidated financial statements<br />

and other financial information about<br />

the Group has been enhanced.<br />

Reconciliation<br />

of equity to IAS<br />

€million<br />

The changeover to IAS has been based<br />

on the assumption that the IAS had<br />

The equity adjustments are mainly predicated on the following material facts:<br />

always been applied (SIC-8). The differences<br />

from restatements resulting<br />

from the Jan. 1, 2000 opening balances<br />

were recognized in equity only, to<br />

the debit or credit of the other reserves<br />

and the minority interests. The synopsis<br />

below summarizes the reconciliation<br />

of equity as of Dec. 31, 1999 (HGB),<br />

to equity as of Jan. 1, 2000 (IAS).<br />

Total equity (incl. minority interests) acc. to HGB at 12-31-1999 263.2<br />

Goodwill 35.0<br />

Tangible assets 56.8<br />

Current assets 9.0<br />

Untaxed/special reserves 11.2<br />

Accruals for pension and similar obligations (50.6)<br />

Other accruals 2.0<br />

Income taxes 2.2<br />

Sundry 6.7<br />

Total equity (incl. minority interests) acc. to IAS at 1-1-2000 * 335.5<br />

* IAS-based total equity (stockholders’ equity + minority interests) as of Jan. 1, 2000, includes minority interests of €13.0 million.<br />

– Goodwill created on or after Jan. 1, 1995, from acquisitions is capitalized in accordance with IAS 22 and amortized<br />

by straight-line charges over its useful life. Under HGB regulations, part of such goodwill was offset against the<br />

reserves retained from earnings.<br />

– Tangible assets, to which partly declining-balance depreciation had been charged, are now depreciated on a<br />

straight-line basis, except for the property, plant and equipment of insignificant companies.<br />

– Tangible assets held under capital leases (aka finance leases) are capitalized and the future rents (excluding<br />

interest portion) concurrently recognized as liability. According to SIC-12, special-purpose leasing firms are<br />

consolidated, too. Where sale & leaseback transactions are involved, the gains on asset disposal realized under<br />

HGB regulations have been recognized as deferred income.<br />

– Being based on tax regulations, untaxed/special reserves are not disclosed in the consolidated financial<br />

statements according to IAS.<br />

– The pension accruals, previously stated in the HGB-based accounts in accordance with Art. 6a German Income<br />

Tax Act (“EStG”), have been redetermined and are annually remeasured to account for future pay, pension and<br />

interest rate rises.<br />

–Accruals for impending losses from uncompleted contracts are recognized at direct production cost with due regard<br />

to directly proratable indirect materials and indirect labor, including production-related depreciation and pension<br />

expenses but excluding any general administrative and selling expenses. In conformity with IAS 37, expenses are<br />

not provided for.<br />

– Assets and liabilities from any future income tax relief or burden (deferred taxes) are recognized according to the<br />

liability method, based on the future tax load. Deferred taxes also include assets created by the offset of tax loss<br />

carryovers against anticipated future profits, however, always provided that their realization is reasonably certain.<br />

– Moreover, the Sundry line mainly mirrors the effects of IAS rules for the accounting treatment of development costs.<br />

(3) Group of consolidated companies Besides Kolbenschmidt Pierburg <strong>AG</strong>,<br />

the consolidated accounts include all<br />

German and foreign subsidiaries in<br />

which Kolbenschmidt Pierburg <strong>AG</strong><br />

holds the majority of voting rights<br />

(whether directly or indirectly). Principally,<br />

companies are initially consolidated<br />

or deconsolidated when control<br />

is transferred. Associated affiliates<br />

and joint ventures are stated at equity.<br />

The additions to investees stated at<br />

equity involve the following:<br />

12-31-2000 Additions Disposals 12-31-<strong>2001</strong><br />

Fully consolidated companies 47 -- (4) 43<br />

thereof German 20 -- (1) 19<br />

thereof foreign 27 -- (3) 24<br />

Investees stated at equity 1 2 -- 3<br />

thereof German -- 1 -- 1<br />

thereof foreign 1 1 -- 2<br />

The disposals from the consolidation<br />

group concern, apart from Pierburg<br />

Instruments GmbH, the following<br />

companies:<br />

– With effect as of December 31,<br />

<strong>2001</strong>/January 1, 2002, the share<br />

capital of Pierburg Instruments<br />

GmbH was raised to admit a new<br />

majority shareholder, thus reducing<br />

the Kolbenschmidt Pierburg Group’s<br />

equity interest in Pierburg Instruments<br />

GmbH to a mere 49 percent.<br />

As of December 31, <strong>2001</strong>, this company<br />

is carried at equity. While<br />

Pierburg Instruments GmbH had<br />

– As and when the controlling<br />

majority was transferred as of<br />

December 31, <strong>2001</strong>, the shares in<br />

Pierburg Instruments Inc. were<br />

sold at a price of €6.0 million.<br />

been fully consolidated in fiscal<br />

2000, this company has been<br />

carried at equity as from fiscal <strong>2001</strong>.<br />

– The other addition to investees<br />

carried at equity refers to Kolbenschmidt<br />

Pierburg Shanghai Nonferrous<br />

Components Co. Ltd., a<br />

joint venture formed in China with<br />

effect as of April 1, <strong>2001</strong>. The share<br />

of €11.5 million was paid up cash.<br />

– Moreover, the shares in Vehicle<br />

Spares Ltd. were sold and transferred<br />

at a price of £1 with economic<br />

effect as of January 1, <strong>2001</strong>.<br />

– In the year under review,<br />

SEM Bailly Compte S.A.S. was<br />

merged into Pierburg S.à.r.l.<br />

77

![PDF [1.0 MB] - KSPG AG](https://img.yumpu.com/5513074/1/171x260/pdf-10-mb-kspg-ag.jpg?quality=85)