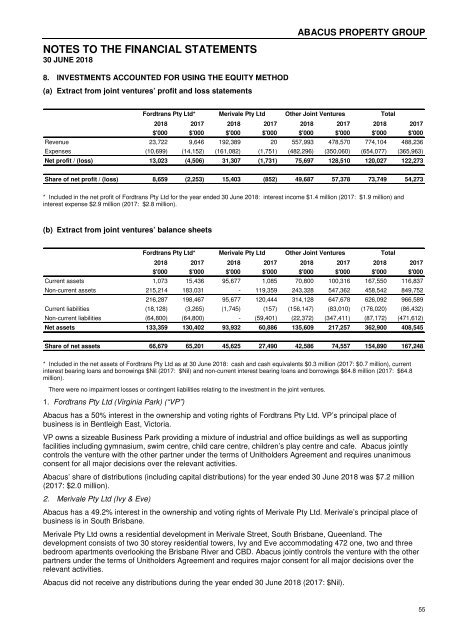

Abacus Property Group – Annual Financial Report 2018

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

ABACUS PROPERTY GROUP<br />

NOTES TO THE FINANCIAL STATEMENTS<br />

30 JUNE <strong>2018</strong><br />

4. INCOME TAX (continued)<br />

(c) Recognised deferred tax assets and liabilities<br />

<strong>2018</strong> 2017<br />

$'000<br />

$'000<br />

Deferred income tax relates to the following:<br />

Deferred tax liabilities<br />

Revaluation of investment properties at fair value 10,675 8,540<br />

Capital allowances 1,976 1,080<br />

Other 2,209 4,948<br />

Gross deferred income tax liabilities 14,860 14,568<br />

Set off against deferred tax assets (2,642) (4,210)<br />

Net deferred income tax liabilities 12,218 10,358<br />

Deferred tax assets<br />

Revaluation of investments and financial instruments at fair value 6,024 6,451<br />

Provisions - other 1,500 1,500<br />

Provisions - employee entitlements 2,272 2,929<br />

Derecognition of deferred tax asset (losses - AHF) (607) (600)<br />

Losses available for offset against future taxable income 655 682<br />

Other 1,034 202<br />

Gross deferred income tax assets 10,878 11,164<br />

Set off of deferred tax liabilities (2,642) (4,210)<br />

Net deferred income tax assets 8,236 6,954<br />

Tax consolidation<br />

AGHL and its 100% owned Australian resident subsidiaries, ASOL and its 100% owned Australian resident<br />

subsidiaries and AHL and its 100% owned Australian resident subsidiaries have formed separate tax<br />

consolidated groups. AGHL, ASOL and AHL are the head entity of their respective tax consolidated groups. The<br />

head entity and the controlled entities in the tax consolidated group continue to account for their own current and<br />

deferred tax amounts. These amounts are measured in a manner that is consistent with the broad principles in<br />

AASB 112 Income Taxes. The nature of the tax funding agreements are discussed further below.<br />

Nature of the tax funding agreement<br />

Members of the respective tax consolidated groups have entered into tax funding agreements. The tax funding<br />

agreements require payments to/from the head entity to be recognised via an inter-entity receivable (payable)<br />

which is at call. To the extent that there is a difference between the amount allocated under the tax funding<br />

agreement and the allocation under UIG 1052, the head entity accounts for these as equity transactions.<br />

The amounts receivable or payable under the tax funding agreements are due upon receipt of the funding advice<br />

from the head entity, which is issued as soon as practicable after the end of each financial year. The head entity<br />

may also require payment of interim funding amounts to assist with its obligations to pay tax instalments.<br />

50