Abacus Property Group – Annual Financial Report 2018

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

ABACUS PROPERTY GROUP<br />

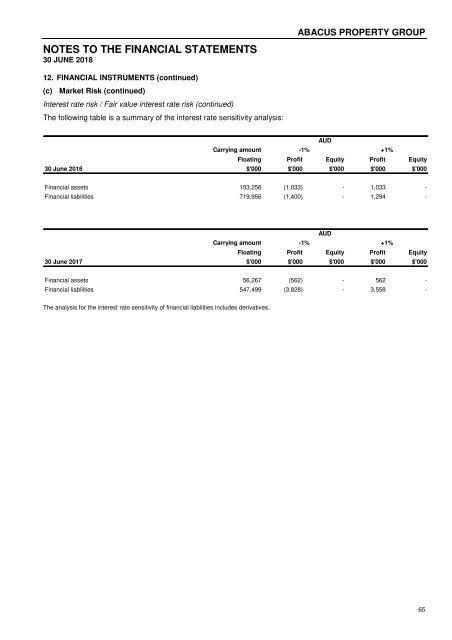

NOTES TO THE FINANCIAL STATEMENTS<br />

30 JUNE <strong>2018</strong><br />

12. FINANCIAL INSTRUMENTS<br />

<strong>Financial</strong> Risk Management<br />

The risks arising from the use of the <strong>Group</strong>’s financial instruments are credit risk, liquidity risk and market risk<br />

(interest rate risk, price risk and foreign currency risk).<br />

The <strong>Group</strong>’s financial risk management focuses on mitigating the unpredictability of the financial markets and its<br />

impact on the financial performance of the <strong>Group</strong>. The Board reviews and agrees policies for managing each of<br />

these risks, which are summarised below.<br />

Primary responsibility for identification and control of financial risks rests with the Treasury Management<br />

Committee under the authority of the Board. The Board reviews and agrees policies for managing each of the<br />

risks identified below, including the setting of limits for trading in derivatives, hedging cover of interest rate risks<br />

and cash flow forecast projections.<br />

The main purpose of the financial instruments used by the <strong>Group</strong> is to raise finance for the <strong>Group</strong>’s operations.<br />

The <strong>Group</strong> has various other financial assets and liabilities such as trade receivables and trade payables, which<br />

arise directly from its operations. The <strong>Group</strong> also enters into derivative transactions principally interest rate<br />

derivatives. The purpose is to manage the interest rate exposure arising from the <strong>Group</strong>’s operations and its<br />

sources of finance.<br />

Details of the significant accounting policies and methods adopted, including the criteria for recognition, the basis<br />

of measurement and the basis on which income and expenses are recognised, in respect of each class of<br />

financial asset, financial liability and equity instruments are disclosed in the section about this report and Note 22<br />

to the financial statements.<br />

(a) Credit risk<br />

Credit risk is the risk of financial loss to the <strong>Group</strong> if a customer or counterparty to a financial instrument fails to<br />

meet its contractual obligations, and arises principally from the <strong>Group</strong>’s receivables from customers, investment in<br />

securities and options, secured property loans and interest bearing loans and derivatives with banks.<br />

The <strong>Group</strong> manages its exposure to risk by:<br />

- derivative counterparties and cash transactions are limited to high credit quality financial institutions;<br />

- policy which limits the amount of credit exposure to any one financial institution;<br />

- providing loans as an investment into joint ventures, associates, related parties and third parties where it is<br />

satisfied with the underlying property exposure within that entity;<br />

- regularly monitoring loans and receivables balances on an ongoing basis;<br />

- regularly monitoring the performance of its associates, joint ventures, related parties and third parties on an<br />

ongoing basis; and<br />

- obtaining collateral as security (where required or appropriate).<br />

The <strong>Group</strong>’s credit risk is predominately driven by its <strong>Property</strong> Developments business which provides loans to<br />

third parties, those using the funds for property development and / or investment. The <strong>Group</strong> mitigates the<br />

exposure to this risk by evaluation of the application before acceptance. The analysis will specifically focus on:<br />

- the Loan Valuation Ratio (LVR) at drawdown;<br />

- mortgage ranking;<br />

- background of the developer (borrower) including previous developments;<br />

- background of the owner (borrower) including previous investment track record;<br />

- that the terms and conditions of higher ranking mortgages are acceptable to the <strong>Group</strong>;<br />

- appropriate property insurances are in place with a copy provided to the <strong>Group</strong>; and<br />

- market analysis of the completed development being used to service drawdown.<br />

The <strong>Group</strong> also mitigates this risk by ensuring adequate security is obtained and timely monitoring of the financial<br />

instrument to identify any potential adverse changes in the credit quality.<br />

60