CUSTOMER AGREED REMUNERATION - CRA International

CUSTOMER AGREED REMUNERATION - CRA International

CUSTOMER AGREED REMUNERATION - CRA International

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

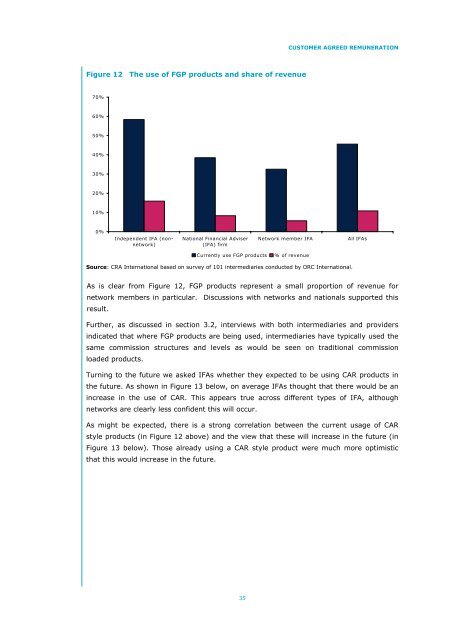

Figure 12 The use of FGP products and share of revenue<br />

70%<br />

60%<br />

50%<br />

40%<br />

30%<br />

20%<br />

10%<br />

0%<br />

Independent IFA (nonnetwork)<br />

National Financial Adviser<br />

(IFA) firm<br />

Currently use FGP products % of revenue<br />

<strong>CUSTOMER</strong> <strong>AGREED</strong> <strong>REMUNERATION</strong><br />

Network member IFA All IFAs<br />

Source: <strong>CRA</strong> <strong>International</strong> based on survey of 101 intermediaries conducted by ORC <strong>International</strong>.<br />

As is clear from Figure 12, FGP products represent a small proportion of revenue for<br />

network members in particular. Discussions with networks and nationals supported this<br />

result.<br />

Further, as discussed in section 3.2, interviews with both intermediaries and providers<br />

indicated that where FGP products are being used, intermediaries have typically used the<br />

same commission structures and levels as would be seen on traditional commission<br />

loaded products.<br />

Turning to the future we asked IFAs whether they expected to be using CAR products in<br />

the future. As shown in Figure 13 below, on average IFAs thought that there would be an<br />

increase in the use of CAR. This appears true across different types of IFA, although<br />

networks are clearly less confident this will occur.<br />

As might be expected, there is a strong correlation between the current usage of CAR<br />

style products (in Figure 12 above) and the view that these will increase in the future (in<br />

Figure 13 below). Those already using a CAR style product were much more optimistic<br />

that this would increase in the future.<br />

35