SSG No 10 - Shipgaz

SSG No 10 - Shipgaz

SSG No 10 - Shipgaz

- TAGS

- shipgaz

- shipgaz.com

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

MARKET REPORTS<br />

Rates and fixtures week 19<br />

Shortsea dry bulk market report<br />

Baltic. The Baltic market has clearly taken<br />

a breather this week with a significant drop<br />

in activity combined with weaker rates.<br />

Prompt tonnage supply is building up in<br />

the whole region forcing owners to accept<br />

rate cuts in order to cover their promptest<br />

positions. Still owners able to book ahead<br />

are putting bullish numbers on their<br />

indications, but presently it seems unlikely<br />

that the market will manage to remain at<br />

present level as tonnage is getting more<br />

and more visible.<br />

Activity level: Slower<br />

Scandinavia. It has been very difficult to<br />

book ahead also in Scandinavian waters<br />

with more tonnage showing along the<br />

coast of <strong>No</strong>rway and in Kattegat. Rates<br />

have remained mostly unchanged, but spot<br />

orders have attracted much more attention<br />

from owners this week indicating that<br />

they have fewer options to play. Still good<br />

activity in project cargo movements from<br />

Denmark and Poland to <strong>No</strong>rway and the<br />

UK this week, but also small coasters are<br />

beginning to see a dip in demand.<br />

Activity level: Slower<br />

UK/Continent. Activity has also dropped<br />

on the Continent with owners looking<br />

for suitable employment to take them to<br />

Baltic or south to Mediterranean. 2,000 mt<br />

soya meal from ARAG to Latvia is paying<br />

in region of EUR 12–12.50 while 3,000<br />

mt minerals from ARAG to N.Spain were<br />

fixed at EUR 19.50 p/mt. Resent increases<br />

in fuel costs have so far not been compensated<br />

in freight rates, and there is reason to<br />

7,000<br />

6,000<br />

5,000<br />

4,000<br />

3,000<br />

2,000<br />

1,000<br />

20<br />

25.000 shipping<br />

professionals<br />

read this ad<br />

believe that current lack of momentum will<br />

make it difficult to push for rate increases.<br />

Activity level: Slower<br />

Mediterranean. Both western and Eastern<br />

Mediterranean are seeing good activity and<br />

volume flow with rates remaining mostly<br />

unchanged on major trading routes. Wheat<br />

continues to dominate the market in western<br />

regions while minerals seem to be the<br />

main taker for tonnage ex Turkey and Black<br />

Sea. Still no change in activity, but tonnage<br />

availability might build up as ships arrive<br />

from <strong>No</strong>rthern Europe in coming weeks.<br />

Activity level: Active<br />

Fixtures<br />

– 2,500 mt agriprod 60’ <strong>No</strong>rth Sea/WC<br />

Greece fixed EUR 64 p/mt<br />

– 3,000 mt minerals WC Greece/Span Med<br />

fixed USD 35 p/mt<br />

Advertise in Scandinavian Shipping Gazette. www.shipgaz.com<br />

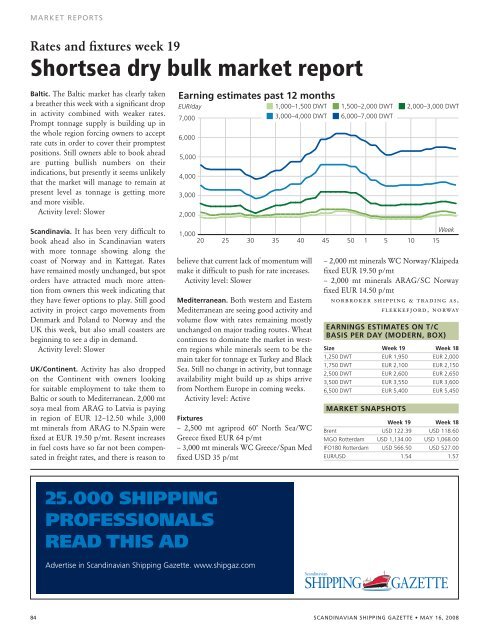

earning estimates past 12 months<br />

EUR/day<br />

■ 1,000–1,500 DWT ■ 1,500–2,000 DWT ■ 2,000–3,000 DWT<br />

■ 3,000–4,000 DWT ■ 6,000–7,000 DWT<br />

25<br />

– 2,000 mt minerals WC <strong>No</strong>rway/Klaipeda<br />

fixed EUR 19.50 p/mt<br />

– 2,000 mt minerals ARAG/SC <strong>No</strong>rway<br />

fixed EUR 14.50 p/mt<br />

norbroker shipping & trading as,<br />

flekkefjord, norway<br />

84 SCANDINAVIAN SHIPPING GAZETTE • MAY 16, 2008<br />

30<br />

35<br />

40<br />

45<br />

50<br />

1<br />

5<br />

<strong>10</strong><br />

15<br />

Week<br />

earningS eStiMateS on t/C<br />

BaSiS per day (Modern, Box)<br />

Size Week 19 Week 18<br />

1,250 DWT EUR 1,950 EUR 2,000<br />

1,750 DWT EUR 2,<strong>10</strong>0 EUR 2,150<br />

2,500 DWT EUR 2,600 EUR 2,650<br />

3,500 DWT EUR 3,550 EUR 3,600<br />

6,500 DWT EUR 5,400 EUR 5,450<br />

MarKet SnapShotS<br />

Week 19 Week 18<br />

Brent USD 122.39 USD 118.60<br />

MGO Rotterdam USD 1,134.00 USD 1,068.00<br />

IFO180 Rotterdam USD 566.50 USD 527.00<br />

EUR/USD 1.54 1.57