lezione 8

lezione 8

lezione 8

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

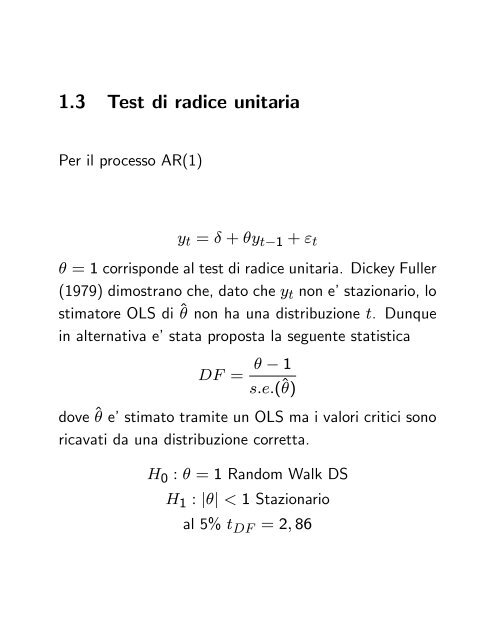

1.3 Test di radice unitaria<br />

Per il processo AR(1)<br />

yt = + yt 1 + "t<br />

= 1 corrisponde al test di radice unitaria. Dickey Fuller<br />

(1979) dimostrano che, dato che yt non e’stazionario, lo<br />

stimatore OLS di ^ non ha una distribuzione t. Dunque<br />

in alternativa e’stata proposta la seguente statistica<br />

DF =<br />

1<br />

s:e:(^)<br />

dove ^ e’stimato tramite un OLS ma i valori critici sono<br />

ricavati da una distribuzione corretta.<br />

H0 : = 1 Random Walk DS<br />

H1 : j j < 1 Stazionario<br />

al 5% t DF = 2; 86

![[ ]](https://img.yumpu.com/14935362/1/184x260/-.jpg?quality=85)