Dóra Fazekas Carbon Market Implications for new EU - UniCredit ...

Dóra Fazekas Carbon Market Implications for new EU - UniCredit ...

Dóra Fazekas Carbon Market Implications for new EU - UniCredit ...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

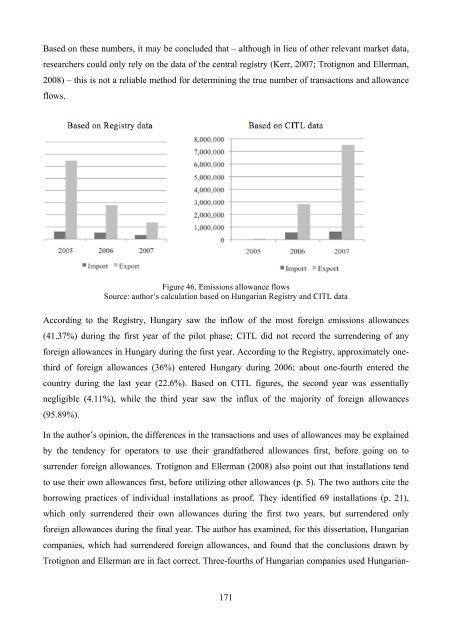

Based on these numbers, it may be concluded that – although in lieu of other relevant market data,<br />

researchers could only rely on the data of the central registry (Kerr, 2007; Trotignon and Ellerman,<br />

2008) – this is not a reliable method <strong>for</strong> determining the true number of transactions and allowance<br />

flows.<br />

Figure 46. Emissions allowance flows<br />

Source: author’s calculation based on Hungarian Registry and CITL data<br />

According to the Registry, Hungary saw the inflow of the most <strong>for</strong>eign emissions allowances<br />

(41.37%) during the first year of the pilot phase; CITL did not record the surrendering of any<br />

<strong>for</strong>eign allowances in Hungary during the first year. According to the Registry, approximately one-<br />

third of <strong>for</strong>eign allowances (36%) entered Hungary during 2006; about one-fourth entered the<br />

country during the last year (22.6%). Based on CITL figures, the second year was essentially<br />

negligible (4.11%), while the third year saw the influx of the majority of <strong>for</strong>eign allowances<br />

(95.89%).<br />

In the author’s opinion, the differences in the transactions and uses of allowances may be explained<br />

by the tendency <strong>for</strong> operators to use their grandfathered allowances first, be<strong>for</strong>e going on to<br />

surrender <strong>for</strong>eign allowances. Trotignon and Ellerman (2008) also point out that installations tend<br />

to use their own allowances first, be<strong>for</strong>e utilizing other allowances (p. 5). The two authors cite the<br />

borrowing practices of individual installations as proof. They identified 69 installations (p. 21),<br />

which only surrendered their own allowances during the first two years, but surrendered only<br />

<strong>for</strong>eign allowances during the final year. The author has examined, <strong>for</strong> this dissertation, Hungarian<br />

companies, which had surrendered <strong>for</strong>eign allowances, and found that the conclusions drawn by<br />

Trotignon and Ellerman are in fact correct. Three-fourths of Hungarian companies used Hungarian-<br />

171