You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

EXECUTIVE SUITE<br />

UPCOMING EVENTS<br />

CinemaCon <strong>2014</strong> Mar. 24–27<br />

National Assoc. of Broadcasters<br />

(NAB) Conf. & Exhibition<br />

Apr. 5–10<br />

NATO of Pennsylvania Apr. 23<br />

NATO of CA/NV Southern<br />

California Film <strong>Pro</strong>duct Seminar<br />

Apr. 24<br />

North Central States NATO <strong>2014</strong> Apr. 29–30<br />

NATO of CA/NV Northern<br />

California Film <strong>Pro</strong>duct Seminar<br />

TONE <strong>2014</strong> Future of Cinema<br />

Conference<br />

Mid-Atlantic NATO “Cinema Show<br />

& Tell”<br />

Apr. 29<br />

May 7<br />

May 13–14<br />

ShowCanada <strong>2014</strong> June 3–5<br />

Cine Europe <strong>2014</strong> June 16–29<br />

NAC Convention & Trade Show<br />

<strong>2014</strong><br />

July 15–18<br />

ShowSouth <strong>2014</strong> Aug. 19–20<br />

Geneva Convention <strong>2014</strong> Sept. 9–11<br />

CineShow <strong>2014</strong> Sept. 16–17<br />

Kino Expo International<br />

Convention & Trade Show <strong>2014</strong><br />

NATO General Membershp and<br />

Board of Directors Meeting<br />

Sept. 22–26<br />

Sept. 30–Oct. 1<br />

Rocky Mountain NATO <strong>2014</strong> Oct. 7–9<br />

Australian International Movie<br />

Convention <strong>2014</strong><br />

Oct. 12–16<br />

ShowARama Oct. 14–16<br />

ShowEast <strong>2014</strong> Oct. 27–30<br />

CineAsia <strong>2014</strong> Dec. 9–11<br />

population. Americans go to the movies a little more than four times<br />

a year at a relatively (by global standards) high ticket price. The U.S.<br />

market is strong but mature. The European market is also relatively<br />

mature, though people there go to the movies about twice a year on<br />

average. Meanwhile, box office is exploding in places like China, India,<br />

Russia, and Brazil. Chinese box office grew 400 percent in five years and<br />

will likely outpace the United States by 2020. Simply put, the emerging<br />

markets have become the growth engine to replace declining DVD sales.<br />

What does the growth of the international market mean for the<br />

quantity and diversity of movies distributed by the majors in the United<br />

States? I have shown how the numbers have declined. Ms. Obst’s book<br />

describes the resulting death of genres, including many (but not all) comedies;<br />

sports movies; small dramas generally, and particularly those that<br />

explore national history; political pieces; period pieces; romances; movies<br />

with minimal pre-awareness; mixed genres; westerns; and more.<br />

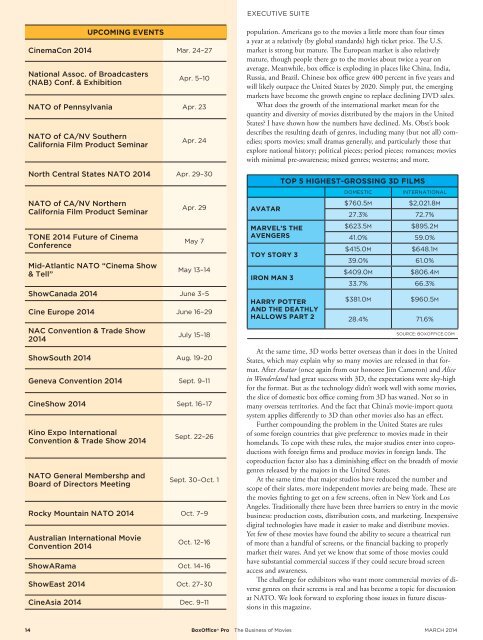

AVATAR<br />

MARVEL’S THE<br />

AVENGERS<br />

TOY STORY 3<br />

IRON MAN 3<br />

TOP 5 HIGHEST-GROSSING 3D FILMS<br />

HARRY POTTER<br />

AND THE DEATHLY<br />

HALLOWS PART 2<br />

DOMESTIC<br />

INTERNATIONAL<br />

$760.5m<br />

$2,021.8m<br />

27.3% 72.7%<br />

$623.5m<br />

$895.2m<br />

41.0% 59.0%<br />

$415.0m<br />

$648.1m<br />

39.0% 61.0%<br />

$409.0m<br />

$806.4m<br />

33.7% 66.3%<br />

$381.0m<br />

$960.5m<br />

28.4% 71.6%<br />

SOURCE: BOXOFFICE.COM<br />

At the same time, 3D works better overseas than it does in the United<br />

States, which may explain why so many movies are released in that format.<br />

After Avatar (once again from our honoree Jim Cameron) and Alice<br />

in Wonderland had great success with 3D, the expectations were sky-high<br />

for the format. But as the technology didn’t work well with some movies,<br />

the slice of domestic box office coming from 3D has waned. Not so in<br />

many overseas territories. And the fact that China’s movie-import quota<br />

system applies differently to 3D than other movies also has an effect.<br />

Further compounding the problem in the United States are rules<br />

of some foreign countries that give preference to movies made in their<br />

homelands. To cope with these rules, the major studios enter into coproductions<br />

with foreign firms and produce movies in foreign lands. The<br />

coproduction factor also has a diminishing effect on the breadth of movie<br />

genres released by the majors in the United States.<br />

At the same time that major studios have reduced the number and<br />

scope of their slates, more independent movies are being made. These are<br />

the movies fighting to get on a few screens, often in New York and Los<br />

Angeles. Traditionally there have been three barriers to entry in the movie<br />

business: production costs, distribution costs, and marketing. Inexpensive<br />

digital technologies have made it easier to make and distribute movies.<br />

Yet few of these movies have found the ability to secure a theatrical run<br />

of more than a handful of screens, or the financial backing to properly<br />

market their wares. And yet we know that some of those movies could<br />

have substantial commercial success if they could secure broad screen<br />

access and awareness.<br />

The challenge for exhibitors who want more commercial movies of diverse<br />

genres on their screens is real and has become a topic for discussion<br />

at NATO. We look forward to exploring those issues in future discussions<br />

in this magazine.<br />

14 BoxOffice ® <strong>Pro</strong> The Business of Movies MARCH <strong>2014</strong>