Option-Implied Currency Risk Premia - Princeton University

Option-Implied Currency Risk Premia - Princeton University

Option-Implied Currency Risk Premia - Princeton University

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

exposure. Since the empirical factor replicating portfolios were constructed to be dollar-neutral the value of this<br />

risk premium component is zero at all points in time. We find that: (a) the model-implied risk premium for the<br />

conditional and unconditional portfolios is statistically indistinguishable; and, (b) the empirical portfolios realized<br />

historical mean returns, which were indistinguishable from the corresponding model-implied premia. The<br />

first result indicates that, although we find evidence of time-variation with the global factor loadings (Table I), it<br />

is insufficiently correlated with the variation in the global price of risk to drive a meaningful wedge between the<br />

risk premia on the conditional and unconditional factor portfolios. We discuss the impact of time-varying global<br />

factor loadings on risk premia in more detail in Section 4. The second result indicates that foreign exchange spot<br />

and option markets consistently price currency risks, and suggests that estimates of currency risk premia based on<br />

historical returns are not significantly upward biased due to peso problems, as argued by Burnside, et al. (2011).<br />

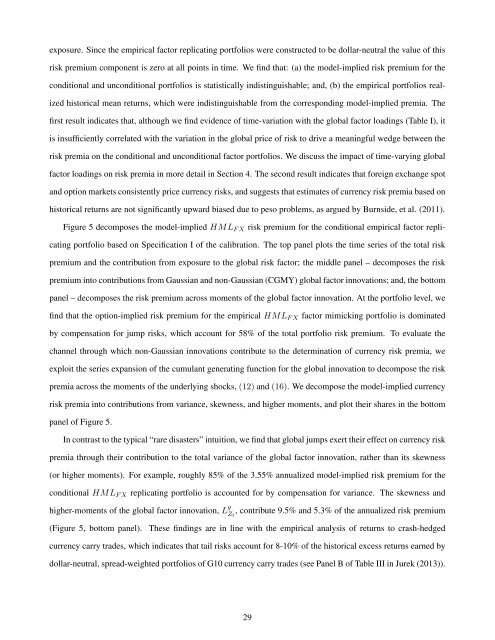

Figure 5 decomposes the model-implied HML F X risk premium for the conditional empirical factor replicating<br />

portfolio based on Specification I of the calibration. The top panel plots the time series of the total risk<br />

premium and the contribution from exposure to the global risk factor; the middle panel – decomposes the risk<br />

premium into contributions from Gaussian and non-Gaussian (CGMY) global factor innovations; and, the bottom<br />

panel – decomposes the risk premium across moments of the global factor innovation. At the portfolio level, we<br />

find that the option-implied risk premium for the empirical HML F X factor mimicking portfolio is dominated<br />

by compensation for jump risks, which account for 58% of the total portfolio risk premium. To evaluate the<br />

channel through which non-Gaussian innovations contribute to the determination of currency risk premia, we<br />

exploit the series expansion of the cumulant generating function for the global innovation to decompose the risk<br />

premia across the moments of the underlying shocks, (12) and (16). We decompose the model-implied currency<br />

risk premia into contributions from variance, skewness, and higher moments, and plot their shares in the bottom<br />

panel of Figure 5.<br />

In contrast to the typical “rare disasters” intuition, we find that global jumps exert their effect on currency risk<br />

premia through their contribution to the total variance of the global factor innovation, rather than its skewness<br />

(or higher moments). For example, roughly 85% of the 3.55% annualized model-implied risk premium for the<br />

conditional HML F X replicating portfolio is accounted for by compensation for variance. The skewness and<br />

higher-moments of the global factor innovation, L g Z t<br />

, contribute 9.5% and 5.3% of the annualized risk premium<br />

(Figure 5, bottom panel).<br />

These findings are in line with the empirical analysis of returns to crash-hedged<br />

currency carry trades, which indicates that tail risks account for 8-10% of the historical excess returns earned by<br />

dollar-neutral, spread-weighted portfolios of G10 currency carry trades (see Panel B of Table III in Jurek (2013)).<br />

29