Securitization Glossary - Securitization.Net

Securitization Glossary - Securitization.Net

Securitization Glossary - Securitization.Net

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Nomura Fixed Income Research<br />

commercial mortgage loans, examples of call protection include<br />

lockouts (temporary prohibitions against prepayment),<br />

defeasance (requirement to purchase securities that create an<br />

identical cash flow), prepayment fees (calculated as a<br />

predetermined percentage of outstanding balance), and yield<br />

maintenance penalties. In subprime residential mortgage loans,<br />

prepayment penalties are a form of call protection.<br />

callable bond – a bond redeemable (prepayable), in whole or in<br />

part, by its issuer before its final maturity date. MBS are a<br />

special form of callable bonds because the borrowers on the<br />

individual underlying mortgage loans can prepay their loans. A<br />

mortgage loan borrower is long an option that allows him to<br />

prepay his loan. An investor who owns an MBS backed by the<br />

loan has a short position in the option.<br />

charge-off – to recognize a loss on a receivable. The charge-off<br />

rate on a pool of receivables (e.g., credit card receivables) is the<br />

annual rate at which losses are realized, expressed as a<br />

percentage of the balance of the pool.<br />

clean-up call – the right of a servicer to redeem an ABS or MBS<br />

after the balance of the underlying asset pool has declined<br />

below a predetermined level (e.g., 10% of its original amount). A<br />

clean-up call permits a servicer to terminate its administrative<br />

obligations (such as processing monthly remittances to<br />

investors and sending out monthly reports) when the related<br />

servicing fee has been reduced to a level that might not fully<br />

cover the cost of administering the transaction.<br />

collateral – (1) assets serving as security for a loan; (2) assets<br />

subject to a lien, charge or encumbrance; (3) assets backing or<br />

underlying a securitization. In the case of a loan secured by<br />

collateral, if the borrower fails to make required payments, the<br />

lender has the right to seize and sell the collateral to recover the<br />

defaulted amount.<br />

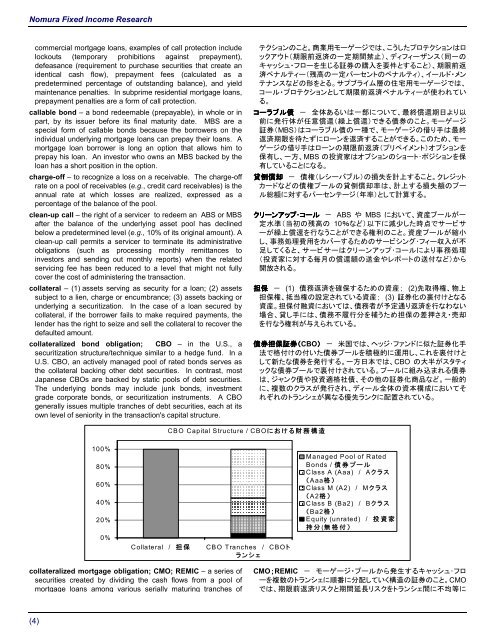

collateralized bond obligation; CBO – in the U.S., a<br />

securitization structure/technique similar to a hedge fund. In a<br />

U.S. CBO, an actively managed pool of rated bonds serves as<br />

the collateral backing other debt securities. In contrast, most<br />

Japanese CBOs are backed by static pools of debt securities.<br />

The underlying bonds may include junk bonds, investment<br />

grade corporate bonds, or securitization instruments. A CBO<br />

generally issues multiple tranches of debt securities, each at its<br />

own level of seniority in the transaction's capital structure.<br />

テクションのこと。 商 業 用 モーゲージでは、こうしたプロテクションはロ<br />

ックアウト( 期 限 前 返 済 の 一 定 期 間 禁 止 )、ディフィーザンス( 同 一 の<br />

キャッシュ・フローを 生 じる 証 券 の 購 入 を 要 件 とすること)、 期 限 前 返<br />

済 ペナルティー( 残 高 の 一 定 パーセントのペナルティ)、イールド・メン<br />

テナンスなどの 形 をとる。サプブライム 層 の 住 宅 用 モーゲージでは、<br />

コール・プロテクションとして 期 限 前 返 済 ペナルティーが 使 われてい<br />

る。<br />

コーラブル 債 - 全 体 あるいは 一 部 について、 最 終 償 還 期 日 より 以<br />

前 に 発 行 体 が 任 意 償 還 ( 繰 上 償 還 )できる 債 券 のこと。モーゲージ<br />

証 券 (MBS)はコーラブル 債 の 一 種 で、モーゲージの 借 り 手 は 最 終<br />

返 済 期 限 を 待 たずにローンを 返 済 することができる。このため、モー<br />

ゲージの 借 り 手 はローンの 期 限 前 返 済 (プリペイメント)オプションを<br />

保 有 し、 一 方 、MBS の 投 資 家 はオプションのショート・ポジションを 保<br />

有 していることになる。<br />

貸 倒 償 却 - 債 権 (レシーバブル)の 損 失 を 計 上 すること。クレジット<br />

カードなどの 債 権 プールの 貸 倒 償 却 率 は、 計 上 する 損 失 額 のプー<br />

ル 総 額 に 対 するパーセンテージ( 年 率 )として 計 算 する。<br />

クリーンアップ・コール - ABS や MBS において、 資 産 プールが 一<br />

定 水 準 ( 当 初 の 残 高 の 10%など) 以 下 に 減 少 した 時 点 でサービサ<br />

ーが 繰 上 償 還 を 行 なうことができる 権 利 のこと。 資 産 プールが 縮 小<br />

し、 事 務 処 理 費 用 をカバーするためのサービシング・フィー 収 入 が 不<br />

足 してくると、サービサーはクリーンアップ・コールにより 事 務 処 理<br />

( 投 資 家 に 対 する 毎 月 の 償 還 額 の 送 金 やレポートの 送 付 など)から<br />

開 放 される。<br />

担 保 - (1) 債 務 返 済 を 確 保 するための 資 産 ; (2) 先 取 得 権 、 物 上<br />

担 保 権 、 抵 当 権 の 設 定 されている 資 産 ; (3) 証 券 化 の 裏 付 けとなる<br />

資 産 。 担 保 付 融 資 においては、 債 務 者 が 予 定 通 り 返 済 を 行 なわない<br />

場 合 、 貸 し 手 には、 債 務 不 履 行 分 を 補 うため 担 保 の 差 押 さえ・ 売 却<br />

を 行 なう 権 利 が 与 えられている。<br />

債 券 担 保 証 券 (CBO) ( - 米 国 では、ヘッジ・ファンドに 似 た 証 券 化 手<br />

法 で 格 付 けの 付 いた 債 券 プールを 積 極 的 に 運 用 し、これを 裏 付 けと<br />

して 新 たな 債 券 を 発 行 する。 一 方 日 本 では、CBO の 大 半 がスタティ<br />

ックな 債 券 プールで 裏 付 けされている。プールに 組 み 込 まれる 債 券<br />

は、ジャンク 債 や 投 資 適 格 社 債 、その 他 の 証 券 化 商 品 など。 一 般 的<br />

に、 複 数 のクラスが 発 行 され、ディール 全 体 の 資 本 構 成 においてそ<br />

れぞれのトランシェが 異 なる 優 先 ランクに 配 置 されている。<br />

CBO Capital Structure / CBOにおける 財 務 構 造<br />

100%<br />

80%<br />

60%<br />

40%<br />

20%<br />

0%<br />

Collateral / 担 保<br />

CBO Tranches / CBOト<br />

ランシェ<br />

Managed Pool of Rated<br />

Bonds / 債 券 プール<br />

Class A (Aaa) / A クラス<br />

(Aaa 格 )<br />

Class M (A2) / M クラス<br />

(A2 格 )<br />

Class B (Ba2) / B クラス<br />

(Ba2 格 )<br />

Equity (unrated) / 投 資 家<br />

持 分 ( 無 格 付 )<br />

collateralized mortgage obligation; CMO; REMIC – a series of<br />

securities created by dividing the cash flows from a pool of<br />

mortgage loans among various serially maturing tranches of<br />

CMO;REMIC - モーゲージ・プールから 発 生 するキャッシュ・フロ<br />

ーを 複 数 のトランシェに 順 番 に 分 配 していく 構 造 の 証 券 のこと。CMO<br />

では、 期 限 前 返 済 リスクと 期 間 延 長 リスクをトランシェ 間 に 不 均 等 に<br />

(4)