Securitization Glossary - Securitization.Net

Securitization Glossary - Securitization.Net

Securitization Glossary - Securitization.Net

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Nomura Fixed Income Research<br />

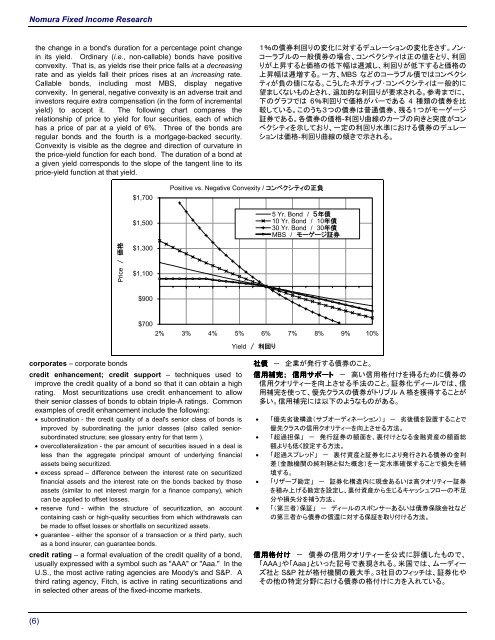

the change in a bond's duration for a percentage point change<br />

in its yield. Ordinary (i.e., non-callable) bonds have positive<br />

convexity. That is, as yields rise their price falls at a decreasing<br />

rate and as yields fall their prices rises at an increasing rate.<br />

Callable bonds, including most MBS, display negative<br />

convexity. In general, negative convexity is an adverse trait and<br />

investors require extra compensation (in the form of incremental<br />

yield) to accept it. The following chart compares the<br />

relationship of price to yield for four securities, each of which<br />

has a price of par at a yield of 6%. Three of the bonds are<br />

regular bonds and the fourth is a mortgage-backed security.<br />

Convexity is visible as the degree and direction of curvature in<br />

the price-yield function for each bond. The duration of a bond at<br />

a given yield corresponds to the slope of the tangent line to its<br />

price-yield function at that yield.<br />

1%の 債 券 利 回 りの 変 化 に 対 するデュレーションの 変 化 をさす。ノン・<br />

コーラブルの 一 般 債 券 の 場 合 、コンベクシティは 正 の 値 をとり、 利 回<br />

りが 上 昇 すると 価 格 の 低 下 幅 は 逓 減 し、 利 回 りが 低 下 すると 価 格 の<br />

上 昇 幅 は 逓 増 する。 一 方 、MBS などのコーラブル 債 ではコンベクシ<br />

ティが 負 の 値 になる。こうしたネガティブ・コンベクシティは 一 般 的 に<br />

望 ましくないものとされ、 追 加 的 な 利 回 りが 要 求 される。 参 考 までに、<br />

下 のグラフでは 6% 利 回 りで 価 格 がパーである 4 種 類 の 債 券 を 比<br />

較 している。このうち3つの 債 券 は 普 通 債 券 、 残 る1つがモーゲージ<br />

証 券 である。 各 債 券 の 価 格 - 利 回 り 曲 線 のカーブの 向 きと 突 度 がコン<br />

ベクシティを 示 しており、 一 定 の 利 回 り 水 準 における 債 券 のデュレー<br />

ションは 価 格 - 利 回 り 曲 線 の 傾 きで 示 される。<br />

$1,700<br />

$1,500<br />

Positive vs. Negative Convexity / コンベクシティの 正 負<br />

5 Yr. Bond / 5 年 債<br />

10 Yr. Bond / 10 年 債<br />

30 Yr. Bond / 30 年 債<br />

MBS / モーゲージ 証 券<br />

Price / 価 格<br />

$1,300<br />

$1,100<br />

$900<br />

$700<br />

2% 3% 4% 5% 6% 7% 8% 9% 10%<br />

Yield / 利 回 り<br />

corporates – corporate bonds<br />

credit enhancement; credit support – techniques used to<br />

improve the credit quality of a bond so that it can obtain a high<br />

rating. Most securitizations use credit enhancement to allow<br />

their senior classes of bonds to obtain triple-A ratings. Common<br />

examples of credit enhancement include the following:<br />

• subordination - the credit quality of a deal's senior class of bonds is<br />

improved by subordinating the junior classes (also called seniorsubordinated<br />

structure; see glossary entry for that term ).<br />

• overcollateralization - the par amount of securities issued in a deal is<br />

less than the aggregate principal amount of underlying financial<br />

assets being securitized.<br />

• excess spread – difference between the interest rate on securitized<br />

financial assets and the interest rate on the bonds backed by those<br />

assets (similar to net interest margin for a finance company), which<br />

can be applied to offset losses.<br />

• reserve fund - within the structure of securitization, an account<br />

containing cash or high-quality securities from which withdrawals can<br />

be made to offset losses or shortfalls on securitized assets.<br />

• guarantee - either the sponsor of a transaction or a third party, such<br />

as a bond insurer, can guarantee bonds.<br />

credit rating – a formal evaluation of the credit quality of a bond,<br />

usually expressed with a symbol such as "AAA" or "Aaa." In the<br />

U.S., the most active rating agencies are Moody's and S&P. A<br />

third rating agency, Fitch, is active in rating securitizations and<br />

in selected other areas of the fixed-income markets.<br />

社 債 - 企 業 が 発 行 する 債 券 のこと。<br />

信 用 補 完 ; 信 用 サポート - 高 い 信 用 格 付 けを 得 るために 債 券 の<br />

信 用 クオリティーを 向 上 させる 手 法 のこと。 証 券 化 ディールでは、 信<br />

用 補 完 を 使 って、 優 先 クラスの 債 券 がトリプル A 格 を 獲 得 することが<br />

多 い。 信 用 補 完 には 以 下 のようなものがある。<br />

• 「 優 先 劣 後 構 造 (サブオーディネーション)」 - 劣 後 債 を 設 置 することで<br />

優 先 クラスの 信 用 クオリティーを 向 上 させる 方 法 。<br />

• 「 超 過 担 保 」 - 発 行 証 券 の 額 面 を、 裏 付 けとなる 金 融 資 産 の 額 面 総<br />

額 よりも 低 く 設 定 する 方 法 。<br />

• 「 超 過 スプレッド」 - 裏 付 資 産 と 証 券 化 により 発 行 される 債 券 の 金 利<br />

差 ( 金 融 機 関 の 純 利 鞘 と 似 た 概 念 )を 一 定 水 準 確 保 することで 損 失 を 補<br />

填 する。<br />

• 「リザーブ 勘 定 」 - 証 券 化 構 造 内 に 現 金 あるいは 高 クオリティー 証 券<br />

を 積 み 上 げる 勘 定 を 設 定 し、 裏 付 資 産 から 生 じるキャッシュフローの 不 足<br />

分 や 損 失 分 を 補 う 方 法 。<br />

• 「( 第 三 者 ) 保 証 」 - ディールのスポンサーあるいは 債 券 保 険 会 社 など<br />

の 第 三 者 から 債 券 の 償 還 に 対 する 保 証 を 取 り 付 ける 方 法 。<br />

信 用 格 付 け - 債 券 の 信 用 クオリティーを 公 式 に 評 価 したもので、<br />

「AAA」や「Aaa」といった 記 号 で 表 現 される。 米 国 では、ムーディー<br />

ズ 社 と S&P 社 が 格 付 機 関 の 最 大 手 。3 社 目 のフィッチは、 証 券 化 や<br />

その 他 の 特 定 分 野 における 債 券 の 格 付 けに 力 を 入 れている。<br />

(6)