Shefrin - Behavioral & Neoclassical asset pricing theories - 2008

Shefrin - Behavioral & Neoclassical asset pricing theories - 2008

Shefrin - Behavioral & Neoclassical asset pricing theories - 2008

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

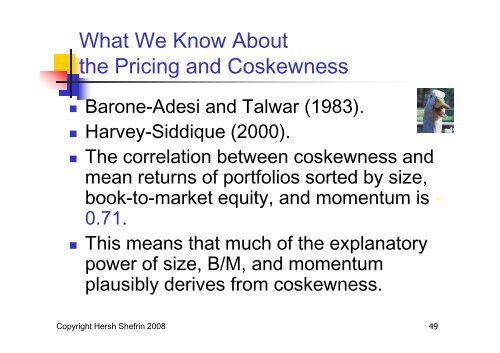

What We Know About<br />

the Pricing and Coskewness<br />

Barone-Adesi and Talwar (1983).<br />

Harvey-Siddique (2000).<br />

The correlation between coskewness and<br />

mean returns of portfolios sorted by size,<br />

book-to-market equity, and momentum is -<br />

0.71.<br />

This means that much of the explanatory<br />

power of size, B/M, and momentum<br />

plausibly derives from coskewness.<br />

Copyright Hersh <strong>Shefrin</strong> <strong>2008</strong><br />

49