Managing Risks of Supply-Chain Disruptions: Dual ... - CiteSeerX

Managing Risks of Supply-Chain Disruptions: Dual ... - CiteSeerX

Managing Risks of Supply-Chain Disruptions: Dual ... - CiteSeerX

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

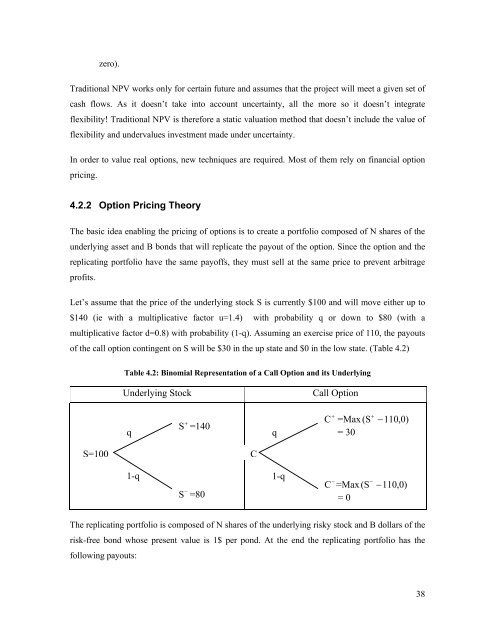

zero).Traditional NPV works only for certain future and assumes that the project will meet a given set <strong>of</strong>cash flows. As it doesn’t take into account uncertainty, all the more so it doesn’t integrateflexibility! Traditional NPV is therefore a static valuation method that doesn’t include the value <strong>of</strong>flexibility and undervalues investment made under uncertainty.In order to value real options, new techniques are required. Most <strong>of</strong> them rely on financial optionpricing.4.2.2 Option Pricing TheoryThe basic idea enabling the pricing <strong>of</strong> options is to create a portfolio composed <strong>of</strong> N shares <strong>of</strong> theunderlying asset and B bonds that will replicate the payout <strong>of</strong> the option. Since the option and thereplicating portfolio have the same pay<strong>of</strong>fs, they must sell at the same price to prevent arbitragepr<strong>of</strong>its.Let’s assume that the price <strong>of</strong> the underlying stock S is currently $100 and will move either up to$140 (ie with a multiplicative factor u=1.4) with probability q or down to $80 (with amultiplicative factor d=0.8) with probability (1-q). Assuming an exercise price <strong>of</strong> 110, the payouts<strong>of</strong> the call option contingent on S will be $30 in the up state and $0 in the low state. (Table 4.2)Table 4.2: Binomial Representation <strong>of</strong> a Call Option and its UnderlyingUnderlying StockCall Optionq+S =140q+C =Max (S + −110,0)= 30S=100C1-q−S =801-q−C =Max (S − −110,0)= 0The replicating portfolio is composed <strong>of</strong> N shares <strong>of</strong> the underlying risky stock and B dollars <strong>of</strong> therisk-free bond whose present value is 1$ per pond. At the end the replicating portfolio has thefollowing payouts:38