Strategic Review of the EDUCO Program - EQUIP123.net

Strategic Review of the EDUCO Program - EQUIP123.net

Strategic Review of the EDUCO Program - EQUIP123.net

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

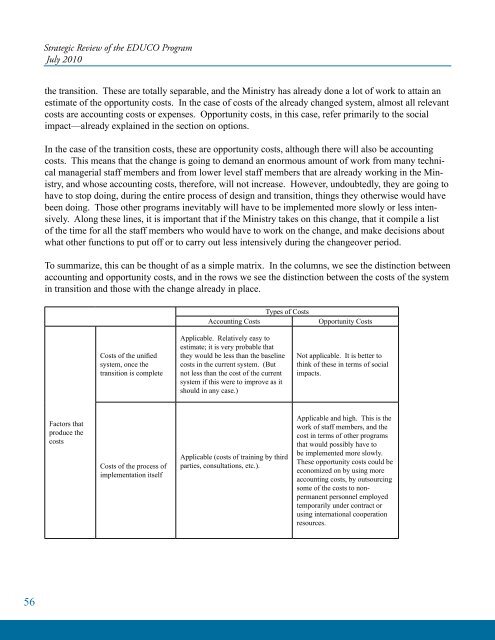

<strong>Strategic</strong> <strong>Review</strong> <strong>of</strong> <strong>the</strong> <strong>EDUCO</strong> <strong>Program</strong>July 2010<strong>the</strong> transition. These are totally separable, and <strong>the</strong> Ministry has already done a lot <strong>of</strong> work to attain anestimate <strong>of</strong> <strong>the</strong> opportunity costs. In <strong>the</strong> case <strong>of</strong> costs <strong>of</strong> <strong>the</strong> already changed system, almost all relevantcosts are accounting costs or expenses. Opportunity costs, in this case, refer primarily to <strong>the</strong> socialimpact—already explained in <strong>the</strong> section on options.In <strong>the</strong> case <strong>of</strong> <strong>the</strong> transition costs, <strong>the</strong>se are opportunity costs, although <strong>the</strong>re will also be accountingcosts. This means that <strong>the</strong> change is going to demand an enormous amount <strong>of</strong> work from many technicalmanagerial staff members and from lower level staff members that are already working in <strong>the</strong> Ministry,and whose accounting costs, <strong>the</strong>refore, will not increase. However, undoubtedly, <strong>the</strong>y are going tohave to stop doing, during <strong>the</strong> entire process <strong>of</strong> design and transition, things <strong>the</strong>y o<strong>the</strong>rwise would havebeen doing. Those o<strong>the</strong>r programs inevitably will have to be implemented more slowly or less intensively.Along <strong>the</strong>se lines, it is important that if <strong>the</strong> Ministry takes on this change, that it compile a list<strong>of</strong> <strong>the</strong> time for all <strong>the</strong> staff members who would have to work on <strong>the</strong> change, and make decisions aboutwhat o<strong>the</strong>r functions to put <strong>of</strong>f or to carry out less intensively during <strong>the</strong> changeover period.To summarize, this can be thought <strong>of</strong> as a simple matrix. In <strong>the</strong> columns, we see <strong>the</strong> distinction betweenaccounting and opportunity costs, and in <strong>the</strong> rows we see <strong>the</strong> distinction between <strong>the</strong> costs <strong>of</strong> <strong>the</strong> systemin transition and those with <strong>the</strong> change already in place.Accounting CostsTypes <strong>of</strong> CostsOpportunity CostsCosts <strong>of</strong> <strong>the</strong> unifiedsystem, once <strong>the</strong>transition is completeApplicable. Relatively easy toestimate; it is very probable that<strong>the</strong>y would be less than <strong>the</strong> baselinecosts in <strong>the</strong> current system. (Butnot less than <strong>the</strong> cost <strong>of</strong> <strong>the</strong> currentsystem if this were to improve as itshould in any case.)Not applicable. It is better tothink <strong>of</strong> <strong>the</strong>se in terms <strong>of</strong> socialimpacts.Factors thatproduce <strong>the</strong>costsCosts <strong>of</strong> <strong>the</strong> process <strong>of</strong>implementation itselfApplicable (costs <strong>of</strong> training by thirdparties, consultations, etc.).Applicable and high. This is <strong>the</strong>work <strong>of</strong> staff members, and <strong>the</strong>cost in terms <strong>of</strong> o<strong>the</strong>r programsthat would possibly have tobe implemented more slowly.These opportunity costs could beeconomized on by using moreaccounting costs, by outsourcingsome <strong>of</strong> <strong>the</strong> costs to nonpermanentpersonnel employedtemporarily under contract orusing international cooperationresources.56