Clusters and competitiveness - PRO INNO Europe

Clusters and competitiveness - PRO INNO Europe

Clusters and competitiveness - PRO INNO Europe

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

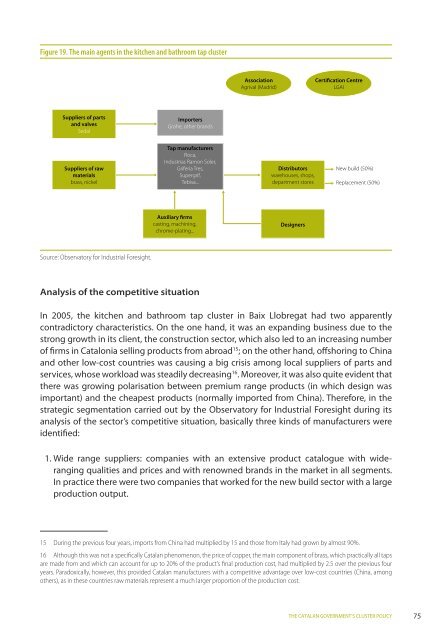

Figure 19. The main agents in the kitchen <strong>and</strong> bathroom tap cluster<br />

Suppliers of parts<br />

<strong>and</strong> valves<br />

Sedal<br />

Suppliers of raw<br />

materials<br />

brass, nickel<br />

Source: Observatory for Industrial Foresight.<br />

Importers<br />

Grohe, other br<strong>and</strong>s<br />

Tap manufacturers<br />

Roca,<br />

Industrias Ramon Soler,<br />

Grifería Tres,<br />

Supergrif,<br />

Tebisa...<br />

Auxiliary firms<br />

casting, machining,<br />

chrome-plating...<br />

Analysis of the competitive situation<br />

Association<br />

Agrival (Madrid)<br />

Distributors<br />

warehouses, shops,<br />

department stores<br />

Designers<br />

Certification Centre<br />

LGAI<br />

New build (50%)<br />

Replacement (50%)<br />

In 2005, the kitchen <strong>and</strong> bathroom tap cluster in Baix Llobregat had two apparently<br />

contradictory characteristics. On the one h<strong>and</strong>, it was an exp<strong>and</strong>ing business due to the<br />

strong growth in its client, the construction sector, which also led to an increasing number<br />

of firms in Catalonia selling products from abroad 15 ; on the other h<strong>and</strong>, offshoring to China<br />

<strong>and</strong> other low-cost countries was causing a big crisis among local suppliers of parts <strong>and</strong><br />

services, whose workload was steadily decreasing 16 . Moreover, it was also quite evident that<br />

there was growing polarisation between premium range products (in which design was<br />

important) <strong>and</strong> the cheapest products (normally imported from China). Therefore, in the<br />

strategic segmentation carried out by the Observatory for Industrial Foresight during its<br />

analysis of the sector’s competitive situation, basically three kinds of manufacturers were<br />

identified:<br />

1. Wide range suppliers: companies with an extensive product catalogue with wideranging<br />

qualities <strong>and</strong> prices <strong>and</strong> with renowned br<strong>and</strong>s in the market in all segments.<br />

In practice there were two companies that worked for the new build sector with a large<br />

production output.<br />

15 During the previous four years, imports from China had multiplied by 15 <strong>and</strong> those from Italy had grown by almost 90%.<br />

16 Although this was not a specifically Catalan phenomenon, the price of copper, the main component of brass, which practically all taps<br />

are made from <strong>and</strong> which can account for up to 20% of the product’s final production cost, had multiplied by 2.5 over the previous four<br />

years. Paradoxically, however, this provided Catalan manufacturers with a competitive advantage over low-cost countries (China, among<br />

others), as in these countries raw materials represent a much larger proportion of the production cost.<br />

THE CATALAN GOVERNMENT’S CLUSTER POLICY<br />

75