Formats

Formats

Formats

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

4.13 Accounting Procedure<br />

1) The accounts are prepared on cash basis i.e. a transaction is only<br />

recorded when cash is received or paid.<br />

2) Period of accounts is a financial year as a period of 12 months from<br />

1 st April to 31st March ending of next year.<br />

3) Daily transactions shall be recorded in Cash Book.<br />

– The receipts are recorded on receipts side and payments on<br />

payments side.<br />

– Every day the cash book shall be closed and Closing Balance<br />

worked out would then form the Opening Balance for next day.<br />

– Classification / head of account for each transaction shall be<br />

clearly mentioned.<br />

4) Every day the details of transactions as recorded in the cash book.<br />

– Transferred to Register of Receipts if the transaction is receipts<br />

– Transferred to Register of Payments if it is payment.<br />

Daily transactions recorded will be transferred automatically either<br />

to register of receipts or to register of payments.<br />

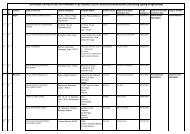

5) At the end of the month total of receipt and payment up to object<br />

head should be shifted to monthly receipts and payment register.<br />

(Format – I)<br />

6) The monthly figure added to month’s progressive total and figures<br />

upto end of the current months can be worked out in the consolidated<br />

abstract register in (Format – II).<br />

7) Bank Reconciliation:<br />

– At the end of the month the bank and treasury reconciliation<br />

should be completed.<br />

– Differences between cash book, bank and treasury balances are<br />

to be rectified.<br />

– Corrections should be made then & there in the Register of<br />

Receipts and Register of Payments.<br />

- 15 -

![lldisha Secretariat. Sachihalaya Marg. Bhubaneswar-75l |]|]l ...](https://img.yumpu.com/19939453/1/184x260/lldisha-secretariat-sachihalaya-marg-bhubaneswar-75l-l-.jpg?quality=85)