- Page 2 and 3:

Nota del Autor: Por axioma (ex ante

- Page 4 and 5:

ÍNDICE SINTÉTICO Introducción 7

- Page 6 and 7:

Síntesis, ampliación y comparaci

- Page 8 and 9:

con otras existentes para ver si la

- Page 10 and 11:

capitalismo, logrando una especie d

- Page 12 and 13:

Capítulo I CONCEPTOS PREVIOS “El

- Page 14 and 15:

indeterminismo; en el primer caso s

- Page 16 and 17:

• Elemento implica: que es indivi

- Page 18 and 19:

como conjunto en cuanto se asocia p

- Page 20 and 21:

La síntesis sería ésta: el tiemp

- Page 22 and 23:

Capítulo II CAUSALIDAD ECONÓMICA

- Page 24 and 25:

de hacerlo, y como toda necesidad,

- Page 26 and 27:

Capítulo III AGENTE ECONÓMICO Dej

- Page 28 and 29:

Esta incorporación del agente econ

- Page 30 and 31:

vez en las que aportan capital y/o

- Page 32 and 33:

económico en particular, a la exis

- Page 34 and 35:

c) Bien económico prestado: es el

- Page 36 and 37:

Existen otras clasificaciones de lo

- Page 38 and 39:

expresado queda clara la siguiente

- Page 40 and 41:

S = C + I (= Pr) Pero lo que no pue

- Page 42 and 43:

demandan los bienes económicos en

- Page 44 and 45:

Aquí se destaca con claridad que e

- Page 46 and 47:

La epistemología ya concluyó sobr

- Page 48 and 49:

Capítulo V INTERCAMBIO INTERTEMPOR

- Page 50 and 51:

El tiempo económico es un bien eco

- Page 52 and 53:

En esta sencilla tabla he destacado

- Page 54 and 55:

CAPÍTULO VI INTERCAMBIO INTERPERSO

- Page 56 and 57:

Se deriva entonces que la forma de

- Page 58 and 59:

A la luz de las conclusiones de est

- Page 60 and 61:

En los siguientes capítulos, refer

- Page 62 and 63:

El incumplimiento es aplicable a lo

- Page 64 and 65:

3) Los precios, en tanto informaci

- Page 66 and 67:

la misma cantidad de ese bien entre

- Page 68 and 69:

CALIDAD Y CANTIDAD EN ECONOMÍA En

- Page 70 and 71:

3) Vendibilidad, es decir, de rápi

- Page 72 and 73:

permita ejercer la función de medi

- Page 74 and 75:

El origen de los extravíos de la t

- Page 76 and 77:

esa liquidez que ahora dispone tien

- Page 78 and 79:

humana de liquidez, el ser humano h

- Page 80 and 81:

Es importante destacar porqué es f

- Page 82 and 83:

esto es de fácil respuesta, en vir

- Page 84 and 85:

múdase el poder adquisitivo del di

- Page 86 and 87:

económico futuro. Y en virtud de q

- Page 88 and 89:

Aquí es donde se convalida el erro

- Page 90 and 91:

Como hemos tenido oportunidad de ve

- Page 92 and 93:

Una vez entendido que el dinero no

- Page 94 and 95:

preocupar también por evitar los d

- Page 96 and 97:

cantidades de los bienes económico

- Page 98 and 99:

Menger se introduce en verdaderos p

- Page 100 and 101:

a que el oro era el principal mater

- Page 102 and 103:

se presentará cuando se cambie por

- Page 104 and 105:

Seguidamente, Mises destaca que exi

- Page 106 and 107:

Precios reales (relativos) y moneta

- Page 108 and 109:

“La solución del problema teóri

- Page 110 and 111:

opuesta la de tratar la neutralidad

- Page 112 and 113:

Acerca de las disputas teóricas re

- Page 114 and 115:

entre el contado y el crédito es e

- Page 116 and 117:

duda alguna a la luz de mi teoría.

- Page 118 and 119:

crediticias se caracteriza por el h

- Page 120 and 121:

identificación precisa de las part

- Page 122 and 123:

CI - Crédito circulatorio o bancar

- Page 124 and 125:

pregunta, ya que los “papeles”

- Page 126 and 127:

manipular la cantidad y/o calidad d

- Page 128 and 129:

extinguida la existencia del crédi

- Page 130 and 131:

CAPÍTULO IX EL CRÉDITO Y LA LIQUI

- Page 132 and 133:

crédito. En el uso del crédito co

- Page 134 and 135:

8) Valor y precio del crédito que

- Page 136 and 137:

En síntesis, la desconfianza es la

- Page 138 and 139: LA PELIGROSA CADENA CREDITICIA (CON

- Page 140 and 141: Por otro lado, hemos concluido que

- Page 142 and 143: Tercera parte CORROBORACIÓN DE LA

- Page 144 and 145: (materialización flexible) y concl

- Page 146 and 147: 1) Utilizaré la partida doble cont

- Page 148 and 149: Fecha: xx/xx/xx Cuenta o rubro Unid

- Page 150 and 151: Fecha: 00/00/01 Estado patrimonial

- Page 152 and 153: Evidentemente, el activo de los est

- Page 154 and 155: económicos; y precisamente la cont

- Page 156 and 157: Fecha: 02/01/01 Intercambio “fís

- Page 158 and 159: Ahora procedo a obtener el estado c

- Page 160 and 161: Fecha: 02/01/01 Estado patrimonial

- Page 162 and 163: Movimientos que se eliminan para el

- Page 164 and 165: CAPÍTULO XII CRÉDITO En este cap

- Page 166 and 167: Fecha: 04/01/01 Estado patrimonial

- Page 168 and 169: Fecha: 05/01/01 Intercambio empresa

- Page 170 and 171: Ahora procedo a obtener el estado c

- Page 172 and 173: a) Los precios surgen del intercamb

- Page 174 and 175: Fecha: 06/10/01 Estado consolidado

- Page 176 and 177: Bien económico PMa: Al observar la

- Page 178 and 179: Espero se advierta la enorme import

- Page 180 and 181: cargo dicha autoridad de las deudas

- Page 182 and 183: No hubo movimiento de unidades fís

- Page 184 and 185: Fecha: 10/01/01 Intercambio en la e

- Page 186 and 187: Fecha: 10/01/01 Estado final de la

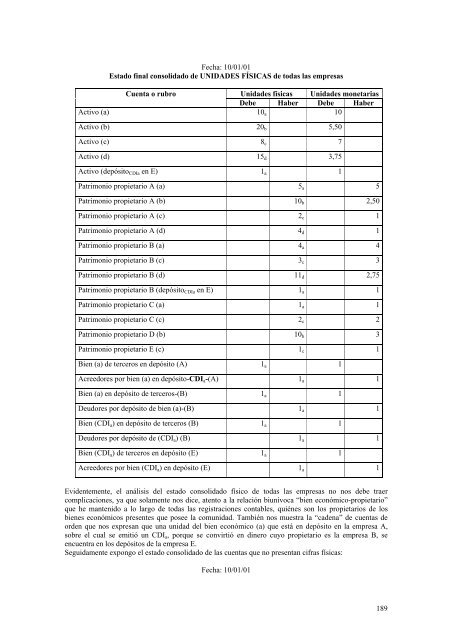

- Page 190 and 191: Estado final consolidado SÓLO UNID

- Page 192 and 193: Fecha: 10/01/01 Estado final consol

- Page 194 and 195: Fecha: 10/01/01 Estado a compensar

- Page 196 and 197: • Tanto el dinero como el crédit

- Page 198 and 199: Cuarta parte Síntesis, ampliación

- Page 200 and 201: flechas que indican al tiempo como

- Page 202 and 203: CONTADO “bienes económicos prese

- Page 204 and 205: Riqueza del Agente económico X Al

- Page 206 and 207: Derivaciones de la ecuación de riq

- Page 208 and 209: Oferta económica A la luz del razo

- Page 210 and 211: Precio interpersonal: “precio que

- Page 212 and 213: es algo atinente a todos los interc

- Page 214 and 215: El rompecabezas que subyace detrás

- Page 216 and 217: materializa el tiempo económico, e

- Page 218 and 219: CAPÍTULO XV TEORÍA CUANTITATIVA C

- Page 220 and 221: “El enfoque de Fisher de la econo

- Page 222 and 223: introduce en el motivo precaución

- Page 224 and 225: compra´ (Ya sabemos lo que opino s

- Page 226 and 227: efiera a las variaciones de interé

- Page 228 and 229: se deriva cómo variarán los stock

- Page 230 and 231: estudio de los stocks, tema de las

- Page 232 and 233: “necesidad-bien económico” y l

- Page 234 and 235: directamente en este proceso (caben

- Page 236 and 237: concibiendo algo así como “carac

- Page 238 and 239:

el concepto de equilibrio, sino que

- Page 240 and 241:

“3- En tercer lugar, tenemos que

- Page 242 and 243:

desempleo. Expresarse en contrario

- Page 244 and 245:

propiedad de las tierras y que en n

- Page 246 and 247:

incluyendo en la ecuación del “d

- Page 248 and 249:

incluye mi ecuación de riqueza tot

- Page 250 and 251:

la ordenada (propiedad); en otras p

- Page 252 and 253:

Comentario de Laidler (p. 19 -fig.

- Page 254 and 255:

En forma sencilla puedo decir que c

- Page 256 and 257:

Tasa de interés r 2 r 1 0 Nivel de

- Page 258 and 259:

como “variable de holgura” para

- Page 260 and 261:

elación positiva entre la variaci

- Page 262 and 263:

CAPÍTULO XVII HAYEK Así como le d

- Page 264 and 265:

En el punto I del referido trabajo

- Page 266 and 267:

forma de dinero (distintos tipos de

- Page 268 and 269:

confusión el hecho de que no está

- Page 270 and 271:

PÚBLICO? [...] debo ahora examinar

- Page 272 and 273:

variables económicas para su vigen

- Page 274 and 275:

dinero virtual, confunden el dinero

- Page 276 and 277:

aspectos teóricos que subyacen en

- Page 278 and 279:

que es dinero y lo que es crédito,

- Page 280 and 281:

precio del dinero en el de los dem

- Page 282 and 283:

Con un buen esquema histórico de l

- Page 284 and 285:

Quinta parte Solución a las CRISIS

- Page 286 and 287:

que pertenece, de lo contrario nadi

- Page 288 and 289:

Las teorías no han llegado a una e

- Page 290 and 291:

Capítulo XIX TRATAMIENTO DE LAS CR

- Page 292 and 293:

Con ánimo de sugerir soluciones gl

- Page 294 and 295:

Es de fundamental importancia no in

- Page 296 and 297:

1) Induce a que los individuos que

- Page 298 and 299:

Apéndice LAS INSTITUCIONES ECONÓM

- Page 300 and 301:

evitar las crisis surgidas de siste

- Page 302 and 303:

CONCEPTOS NUEVOS GLOSARIO DE CONCEP

- Page 304 and 305:

Materialización del tiempo económ

- Page 306 and 307:

“Vetusta riqueza” o “vetusta

- Page 308 and 309:

Introducción al Conocimiento Cient

- Page 310 and 311:

DERNBURG, Thomas F. y MCDOUGALL, Du

- Page 312 and 313:

MARX, Carlos, El Capital: Crítica

- Page 314 and 315:

ZALDUENDO, Eduardo A., Breve Histor

- Page 316 and 317:

i) Otras clasificaciones 35 Cómo s

- Page 318 and 319:

Capítulo IX El crédito y la liqui

- Page 320 and 321:

Teoría de Hayek 262 Trueque y dine

- Page 322:

322