Fresh Point Magazine - B2B24 - Il Sole 24 Ore

Fresh Point Magazine - B2B24 - Il Sole 24 Ore

Fresh Point Magazine - B2B24 - Il Sole 24 Ore

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

The big southern-hemisphere producers are Chile and<br />

the RSA, followed by Argentina, Peru, India and Namibia.<br />

Import and export in EU countries<br />

Overall EU imports exceed 1.5 million tons a year and,<br />

although a slight dip in trade volumes occurred in<br />

2009 and 2010 owing to a slide in demand and a rise<br />

in average list price, the overall trend keeps rising.<br />

While most of the table grape for EU consumers – about<br />

a million tons – is produced by Italy, Spain and Greece,<br />

imports also account for a considerable amount, registering<br />

over the last few years more than 600 thousand<br />

tons for a bill of more than a €1 billion (fig. 3).<br />

The EU’s leading table-grape exporters are the<br />

Netherlands and Germany, countries that are reexporters<br />

but not actual producers. For example,<br />

Holland re-exports during winter and spring because<br />

it imports from non-European producers.<br />

Intra-EU trade occurs mostly from July to December<br />

whereas the supply from October to June is imported<br />

from the usual southern-hemisphere producers.<br />

EU imports start in October from Brazil and extend<br />

through June from the RSA, Argentina, Chile and<br />

India, with the RSA and Chile combining to account<br />

for nearly 60% of the import volumes (fig. 4).<br />

EU imports from non-Union producers grew at an<br />

average 2.9% from 2005 to 2010. The suppliers<br />

è il principale produttore europeo di uve da tavola con<br />

circa 2 milioni di tonnellate. Tra i grandi produttori dell’emisfero<br />

australe spiccano invece Cile e Sudafrica,<br />

seguiti da Argentina, Perù, India e Namibia.<br />

Import ed export nei Paesi Ue<br />

Le importazioni dei Paesi Ue superano gli 1,5 milioni di<br />

tonnellate. Negli ultimi dieci anni sono cresciute a un<br />

ritmo molto sostenuto anche se, nel 2009 e nel 2010, è<br />

stata registrata una lieve riduzione dei volumi, determinata<br />

dalla contrazione dell’offerta e dall’aumento dei<br />

listini medi del prodotto importato.<br />

La maggior parte di uva da tavola – circa un milione di tonnellate<br />

- viene dai produttori comunitari (Italia, Spagna e<br />

Grecia), ma anche le importazioni dai Paesi terzi sono rilevanti,<br />

e negli ultimi anni hanno superato le 600mila tonnellate,<br />

con una spesa di oltre 1.000 milioni di euro (fig. 3).<br />

Tra i principali esportatori europei figurano anche Paesi<br />

Bassi e Germania che non sono produttori di uve da<br />

tavola, ma che riesportano una quota significativa delle<br />

uve importate. In particolare, le esportazioni dei Paesi<br />

Bassi riguardano le uve di origine extraeuropea e quindi<br />

sono concentrate nei mesi invernali e primaverili.<br />

Gli scambi intracomunitari avvengono soprattutto tra luglio<br />

e dicembre quando è disponibile la produzione del nostro<br />

emisfero, mentre da ottobre a giugno le importazioni sono<br />

garantite dai diversi produttori dell’emisfero australe.<br />

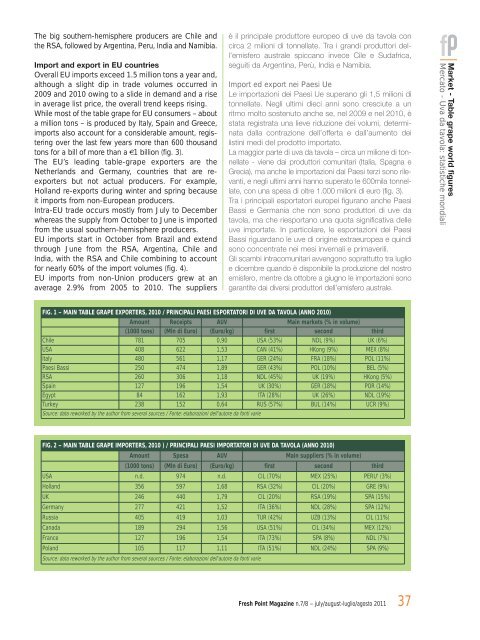

FIG. 1 – MAIN TABLE GRAPE EXPORTERS, 2010 / PRINCIPALI PAESI ESPORTATORI DI UVE DA TAVOLA (ANNO 2010)<br />

Amount Receipts AUV Main markets (% in volume)<br />

(1000 tons) (Mln di Euro) (Euro/kg) first second third<br />

Chile 781 705 0,90 USA (53%) NDL (9%) UK (6%)<br />

USA 408 622 1,53 CAN (41%) HKong (9%) MEX (8%)<br />

Italy 480 561 1,17 GER (<strong>24</strong>%) FRA (18%) POL (11%)<br />

Paesi Bassi 250 474 1,89 GER (43%) POL (10%) BEL (5%)<br />

RSA 260 306 1,18 NDL (45%) UK (19%) HKong (5%)<br />

Spain 127 196 1,54 UK (30%) GER (18%) POR (14%)<br />

Egypt 84 162 1,93 ITA (28%) UK (26%) NDL (19%)<br />

Turkey 238 152 0,64 RUS (57%) BUL (14%) UCR (9%)<br />

Source: data reworked by the author from several sources / Fonte: elaborazioni dell’autore da fonti varie<br />

FIG. 2 – MAIN TABLE GRAPE IMPORTERS, 2010 ) / PRINCIPALI PAESI IMPORTATORI DI UVE DA TAVOLA (ANNO 2010)<br />

Amount Spesa AUV Main suppliers (% in volume)<br />

(1000 tons) (Mln di Euro) (Euro/kg) first second third<br />

USA n.d. 974 n.d. CIL (70%) MEX (25%) PERU' (3%)<br />

Holland 356 597 1,68 RSA (32%) CIL (20%) GRE (9%)<br />

UK <strong>24</strong>6 440 1,79 CIL (20%) RSA (19%) SPA (15%)<br />

Germany 277 421 1,52 ITA (36%) NDL (28%) SPA (12%)<br />

Russia 405 419 1,03 TUR (42%) UZB (13%) CIL (11%)<br />

Canada 189 294 1,56 USA (51%) CIL (34%) MEX (12%)<br />

France 127 196 1,54 ITA (73%) SPA (8%) NDL (7%)<br />

Poland 105 117 1,11 ITA (51%) NDL (<strong>24</strong>%) SPA (9%)<br />

Source: data reworked by the author from several sources / Fonte: elaborazioni dell’autore da fonti varie<br />

<strong>Fresh</strong> <strong>Point</strong> <strong>Magazine</strong> n.7/8 – july/august-luglio/agosto 2011<br />

37<br />

Market - Table grape world figures<br />

Mercato - Uva da tavola: statistiche mondiali