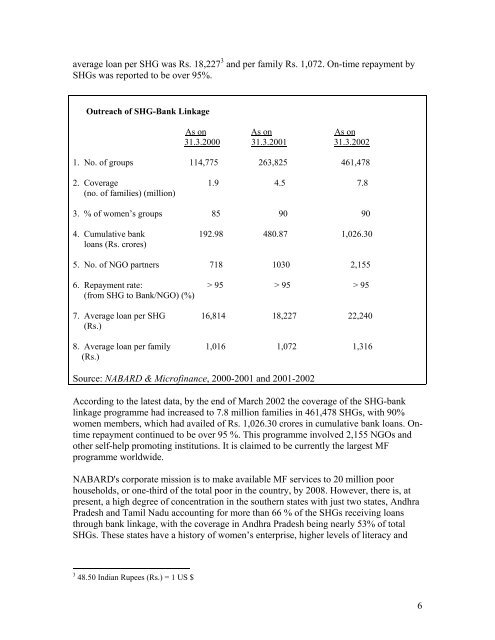

average loan per SHG w<strong>as</strong> Rs. 18,227 3 and per family Rs. 1,072. On-time repayment bySHGs w<strong>as</strong> reported to be over 95%.Outreach of SHG-Bank L<strong>in</strong>kageAs on As on As on31.3.2000 31.3.2001 31.3.20021. No. of groups 114,775 263,825 461,4782. Coverage 1.9 4.5 7.8(no. of families) (million)3. % of women’s groups 85 90 904. Cumulative bank 192.98 480.87 1,026.30loans (Rs. crores)5. No. of NGO partners 718 1030 2,1556. Repayment rate: > 95 > 95 > 95(from SHG to Bank/NGO) (%)7. Average loan per SHG 16,814 18,227 22,240(Rs.)8. Average loan per family 1,016 1,072 1,316(Rs.)Source: NABARD & Microf<strong>in</strong>ance, 2000-2001 and 2001-2002Accord<strong>in</strong>g to the latest data, by the end of March 2002 the coverage of the SHG-bankl<strong>in</strong>kage programme had <strong>in</strong>cre<strong>as</strong>ed to 7.8 million families <strong>in</strong> 461,478 SHGs, with 90%women members, which had availed of Rs. 1,026.30 crores <strong>in</strong> cumulative bank loans. Ontimerepayment cont<strong>in</strong>ued to be over 95 %. This programme <strong>in</strong>volved 2,155 NGOs andother self-<strong>help</strong> promot<strong>in</strong>g <strong>in</strong>stitutions. It is claimed to be currently the largest MFprogramme worldwide.NABARD's corporate mission is to make available MF services to 20 million poorhouseholds, or one-third of the total poor <strong>in</strong> the country, by 2008. However, there is, atpresent, a high degree of concentration <strong>in</strong> the southern states with just two states, AndhraPradesh and Tamil Nadu account<strong>in</strong>g for more than 66 % of the SHGs receiv<strong>in</strong>g loansthrough bank l<strong>in</strong>kage, with the coverage <strong>in</strong> Andhra Pradesh be<strong>in</strong>g nearly 53% of totalSHGs. These states have a history of women’s enterprise, higher levels of literacy and3 48.50 <strong>India</strong>n Rupees (Rs.) = 1 US $6

strong cooperative <strong>in</strong>stitutions. SHG-bank l<strong>in</strong>kage h<strong>as</strong> not <strong>as</strong> yet made an impact <strong>in</strong> thepoverty belt of the northern, central and e<strong>as</strong>tern regions.The outreach of SHG-bank l<strong>in</strong>kage may seem to be impressive, but <strong>in</strong> the context of themagnitude of poverty <strong>in</strong> <strong>India</strong> and the flow of funds for poverty alleviation it represents avery small <strong>in</strong>tervention. An estimated 60 million <strong>India</strong>n rural households may be cl<strong>as</strong>sified<strong>as</strong> poor. It is well known that only about one-third of SHG members are able to accessloans <strong>in</strong> the <strong>in</strong>itial years. Thus of the 4.5 million families covered by March 2001 andeligible for bank loans, only about 1.5 million would have received loans of an average ofRs. 3,000 each. The benefit of bank f<strong>in</strong>ance is thus realised by a much smaller number offamilies. Other members, however, may benefit through sav<strong>in</strong>gs and petty loans from theSHGs’ <strong>in</strong>ternal fund.Rs. 53,504 crores w<strong>as</strong> expected to be disbursed for agriculture and allied activities by thebank<strong>in</strong>g system dur<strong>in</strong>g 2000-2001 4 . Dur<strong>in</strong>g the same period, disbursements under bankl<strong>in</strong>kage were Rs.250.62 crores or less than half of one per cent of this figure. Similarly,disbursements of bank loans under the poverty-focused self-employment programme,Swarna Jayanti Swarozgar Yojana (SGSY) 5 , meant for families below the poverty l<strong>in</strong>e,were Rs. 642.34 crores or more than two and a half times the advances under SHG-bankl<strong>in</strong>kage. Thus while the SHG programme h<strong>as</strong> made notable progress <strong>in</strong> provid<strong>in</strong>g loans tolargely poor families, it h<strong>as</strong> not significantly <strong>in</strong>cre<strong>as</strong>ed the credit flow to rural are<strong>as</strong>.2.3 Institutions Fund<strong>in</strong>g and Promot<strong>in</strong>g SHGs2.3.1 MF WholesalersThere are half-a-dozen apex <strong>in</strong>stitutions provid<strong>in</strong>g funds and capacity-build<strong>in</strong>g supportfor MF through various MFIs. Under various schemes they provide bulk loans to retailNGO-MFIs and other emerg<strong>in</strong>g forms of microf<strong>in</strong>ance <strong>in</strong>stitutions (MFIs) such <strong>as</strong>f<strong>in</strong>ancial cooperatives, mutually aided cooperative thrift societies (MACTS), andfederations of SHGs. Detailed particulars of their loan schemes and terms are given <strong>in</strong>Appendix 3. A similar approach to NABARD’s bank l<strong>in</strong>kage, us<strong>in</strong>g NGOs/MFIs <strong>as</strong><strong>in</strong>termediaries (model III <strong>in</strong> section 2.2.1 above) h<strong>as</strong> also been adopted by other bulklend<strong>in</strong>g <strong>in</strong>stitutions such <strong>as</strong> the Small Industries Bank of <strong>India</strong> (SIDBI), R<strong>as</strong>htriya MahilaKosh (RMK), Hous<strong>in</strong>g and F<strong>in</strong>ance Development Corporation (HDFC), Hous<strong>in</strong>g andUrban Development Corporation (HUDCO), R<strong>as</strong>htriya Grameen Vik<strong>as</strong> Nidhi (RGVN)and Friends of Women’s World Bank<strong>in</strong>g (FWWB).NABARD: Apart from giv<strong>in</strong>g the lead <strong>in</strong> pilot<strong>in</strong>g the SHG-bank l<strong>in</strong>kage and the ref<strong>in</strong>anceof loans by banks to SHGs, NABARD is engaged <strong>in</strong> fulfill<strong>in</strong>g a variety of promotion andsupport functions <strong>as</strong> the apex bank for agriculture and rural development. These <strong>in</strong>clude:• develop<strong>in</strong>g a conducive policy framework4 These data and those below are from NABARD Annual Report 2000-2001.5 This, <strong>in</strong> turn, is currently be<strong>in</strong>g implemented on a smaller scale than its predecessor, the IRD programme,which closed <strong>in</strong> 1999 and under which annual bank loans were <strong>in</strong> excess of Rs. 1,500 crores.7

- Page 4 and 5: List of AcronymsAIAMEDAIMSAPMASASAA

- Page 6 and 7: EXECUTIVE SUMMARY1. Introduction1.1

- Page 8 and 9: self-management by members and scal

- Page 10 and 11: 6.4 On the other hand field reports

- Page 12 and 13: sustainable self-help groups. An in

- Page 14 and 15: 2. DEVELOPMENT OF SELF-HELP GROUPS

- Page 18 and 19: • training and sensitising bank o

- Page 20 and 21: organizational structure and the na

- Page 22 and 23: Table 2.1 (contd.)S.No.ParticularsN

- Page 24 and 25: the SHG from banks starts from pari

- Page 26 and 27: • In either situation SHGs can co

- Page 28 and 29: 3.2.3 SHG Federations Linked to MF

- Page 32 and 33: 3.4 ConclusionThis section served t

- Page 34 and 35: MYRADA,Karnatakaa.o.OUTREACH,Karnat

- Page 36 and 37: Name ofNGO/StateDHANFoundation,Tami

- Page 38 and 39: However, for a comparative analysis

- Page 40 and 41: linkages with credit and savings 34

- Page 42 and 43: out of 5,153 SHGs covered under the

- Page 44 and 45: eceived revolving fund grants, cost

- Page 46 and 47: the high level of educated unemploy

- Page 48 and 49: CARE-CASHE Project(A.P.)(implemente

- Page 50 and 51: Holy CrossSocial ServiceCentre(HCSS

- Page 52 and 53: Agency/Programme5. Rashtriya Mahila

- Page 54 and 55: microfinance intermediary 41 . Unde

- Page 56 and 57: On the other hand, there is evidenc

- Page 58 and 59: infrastructural and other constrain

- Page 60 and 61: would not be possible while working

- Page 62 and 63: through the SHG as a basis to sourc

- Page 64 and 65: the programme is particularly probl

- Page 66 and 67:

It is possible to query the methodo

- Page 68 and 69:

world. Other partners from India ar

- Page 70 and 71:

RECOMMENDATIONSIt is not clear what

- Page 72 and 73:

REFERENCESAIAMED (2000), Good Pract

- Page 75:

Mahajan, Vijay and G. Nagasri (1999

- Page 79 and 80:

Appendix 2: Types of SHGsTypes of S

- Page 81 and 82:

Appendix 3 (contd.)OrganisationSIDB

- Page 83 and 84:

4. Trade based Group model: The est

- Page 85 and 86:

Appendix 5S.No.1. JOTHI 92,077.00

- Page 87:

Appendix 6: Stages of Evolution of