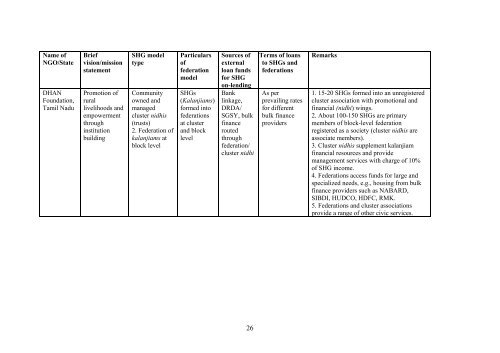

Name ofNGO/StateDHANFoundation,Tamil NaduBriefvision/missionstatementPromotion ofrurallivelihoods andempowermentthrough<strong>in</strong>stitutionbuild<strong>in</strong>gSHG modeltypeCommunityowned andmanagedcluster nidhis(trusts)2. Federation ofkalanjiams atblock levelParticularsoffederationmodelSHGs(Kalanjiams)formed <strong>in</strong>tofederationsat clusterand blocklevelSources ofexternalloan fundsfor SHGon-lend<strong>in</strong>gBankl<strong>in</strong>kage,DRDA/SGSY, bulkf<strong>in</strong>anceroutedthroughfederation/cluster nidhiTerms of loansto SHGs andfederationsAs perprevail<strong>in</strong>g ratesfor differentbulk f<strong>in</strong>anceprovidersRemarks1. 15-20 SHGs formed <strong>in</strong>to an unregisteredcluster <strong>as</strong>sociation with promotional andf<strong>in</strong>ancial (nidhi) w<strong>in</strong>gs.2. About 100-150 SHGs are primarymembers of block-level federationregistered <strong>as</strong> a society (cluster nidhis are<strong>as</strong>sociate members).3. Cluster nidhis supplement kalanjiamf<strong>in</strong>ancial resources and providemanagement services with charge of 10%of SHG <strong>in</strong>come.4. Federations access funds for large andspecialized needs, e.g., hous<strong>in</strong>g from bulkf<strong>in</strong>ance providers such <strong>as</strong> NABARD,SIBDI, HUDCO, HDFC, RMK.5. Federations and cluster <strong>as</strong>sociationsprovide a range of other civic services.26

4. COSTS OF SHG PROMOTIONThe cost of promotion of SHGs h<strong>as</strong> become a live issue for discussion <strong>in</strong> development circles<strong>in</strong> <strong>India</strong>. Rough estimates of promotion cost per SHG for different projects, NGOs and banksengaged <strong>in</strong> SHG promotion varies considerably 31 . The wide range of such estimates is notunsurpris<strong>in</strong>g. First, there rema<strong>in</strong>s a lack of uniformity about what costs to <strong>in</strong>clude, how stafftime is imputed for development workers partially engaged <strong>in</strong> SHG promotion along withother functions, and whether and how overhead costs are allocated. Second, the period ofsupport and the nature and purpose of SHGs promoted is also varied. Some SHGs are broughttogether <strong>in</strong> federations, which requires <strong>in</strong> turn the build<strong>in</strong>g of further capacity and <strong>in</strong>curr<strong>in</strong>gof costs <strong>in</strong> respect of these <strong>in</strong>stitutions. Third, distance and time taken to reach <strong>in</strong>teriorvillages and to motivate communities byp<strong>as</strong>sed by development is greater than forma<strong>in</strong>stream villages. F<strong>in</strong>ally, the prices of <strong>in</strong>puts differ across the country such that the sameset of physical <strong>in</strong>puts may cost more <strong>in</strong> some regions than <strong>in</strong> others. The cost of SHGpromotion is a particular concern of the donor community that is keen to ensure theproductive and effective use of grants provided for this purpose.As part of this study data h<strong>as</strong> been obta<strong>in</strong>ed from 10 NGOs/projects on costs of SHGpromotion through <strong>in</strong>terviews and written communications. This consisted of estimatesvary<strong>in</strong>g from rough calculations to more detailed item-wise estimates prepared <strong>in</strong> model formor worked out on the b<strong>as</strong>is of historical cost of the projects. These are discussed <strong>in</strong> section4.4. However, before attempt<strong>in</strong>g an analysis of data obta<strong>in</strong>ed from lead<strong>in</strong>g NGO promoters ofSHGs towards benchmark<strong>in</strong>g of promotion costs, it would be <strong>in</strong>structive to exam<strong>in</strong>e theconcept of cost-effectiveness, or efficiency, of SHG promotion.4.1 Concepts of Cost EfficiencyIn any development project activities are undertaken with a view to generate a level ofbenefits <strong>in</strong> excess of the costs of the project. Neo-cl<strong>as</strong>sical decision rules can be employed forchoos<strong>in</strong>g between alternative <strong>in</strong>vestments us<strong>in</strong>g techniques b<strong>as</strong>ed upon marg<strong>in</strong>al analysis.These <strong>in</strong>volve discount<strong>in</strong>g future costs and benefits accru<strong>in</strong>g to project participants to arriveat the net present worth of a project. In projects expected to yield tangible outputs, like an<strong>in</strong>cre<strong>as</strong>e <strong>in</strong> agricultural production, the quantification of benefits is relatively e<strong>as</strong>y. However,where <strong>in</strong>tangible outputs result, e.g., <strong>in</strong> education and health projects, the method used is to“determ<strong>in</strong>e on a present worth b<strong>as</strong>is the le<strong>as</strong>t cost comb<strong>in</strong>ation of tangible costs that willrealise the same <strong>in</strong>tangible benefit.” (Gitt<strong>in</strong>ger, 1984). This is known <strong>as</strong> le<strong>as</strong>t-cost analysis orcost effectiveness analysis.We can view SHG formation <strong>as</strong> an “<strong>in</strong>termediate project output” with<strong>in</strong> a larger developmentproject or service delivery programme. Cost-effectiveness analysis can also be applied topromotion of a unit SHG to make a selection from different approaches represent<strong>in</strong>g differenttechnologies of promotion. Us<strong>in</strong>g the constant effects method, a comparison of thediscounted present worth of costs <strong>in</strong>curred over the years <strong>in</strong> develop<strong>in</strong>g an SHG underdifferent models can <strong>help</strong> determ<strong>in</strong>e the le<strong>as</strong>t-cost or efficient technology 32 .31 Harper (2002) reports a range of between about Rs. 1,350 and Rs. 16,000 for the cost of <strong>in</strong>itially develop<strong>in</strong>gand <strong>as</strong>sess<strong>in</strong>g an SHG.32 This does not, however, constitute a me<strong>as</strong>ure of effectiveness, or impact, of a project s<strong>in</strong>ce the analysis isdone without reference to the participants or users of the project.27

- Page 4 and 5: List of AcronymsAIAMEDAIMSAPMASASAA

- Page 6 and 7: EXECUTIVE SUMMARY1. Introduction1.1

- Page 8 and 9: self-management by members and scal

- Page 10 and 11: 6.4 On the other hand field reports

- Page 12 and 13: sustainable self-help groups. An in

- Page 14 and 15: 2. DEVELOPMENT OF SELF-HELP GROUPS

- Page 16 and 17: average loan per SHG was Rs. 18,227

- Page 18 and 19: • training and sensitising bank o

- Page 20 and 21: organizational structure and the na

- Page 22 and 23: Table 2.1 (contd.)S.No.ParticularsN

- Page 24 and 25: the SHG from banks starts from pari

- Page 26 and 27: • In either situation SHGs can co

- Page 28 and 29: 3.2.3 SHG Federations Linked to MF

- Page 32 and 33: 3.4 ConclusionThis section served t

- Page 34 and 35: MYRADA,Karnatakaa.o.OUTREACH,Karnat

- Page 38 and 39: However, for a comparative analysis

- Page 40 and 41: linkages with credit and savings 34

- Page 42 and 43: out of 5,153 SHGs covered under the

- Page 44 and 45: eceived revolving fund grants, cost

- Page 46 and 47: the high level of educated unemploy

- Page 48 and 49: CARE-CASHE Project(A.P.)(implemente

- Page 50 and 51: Holy CrossSocial ServiceCentre(HCSS

- Page 52 and 53: Agency/Programme5. Rashtriya Mahila

- Page 54 and 55: microfinance intermediary 41 . Unde

- Page 56 and 57: On the other hand, there is evidenc

- Page 58 and 59: infrastructural and other constrain

- Page 60 and 61: would not be possible while working

- Page 62 and 63: through the SHG as a basis to sourc

- Page 64 and 65: the programme is particularly probl

- Page 66 and 67: It is possible to query the methodo

- Page 68 and 69: world. Other partners from India ar

- Page 70 and 71: RECOMMENDATIONSIt is not clear what

- Page 72 and 73: REFERENCESAIAMED (2000), Good Pract

- Page 75: Mahajan, Vijay and G. Nagasri (1999

- Page 79 and 80: Appendix 2: Types of SHGsTypes of S

- Page 81 and 82: Appendix 3 (contd.)OrganisationSIDB

- Page 83 and 84: 4. Trade based Group model: The est

- Page 85 and 86: Appendix 5S.No.1. JOTHI 92,077.00

- Page 87:

Appendix 6: Stages of Evolution of