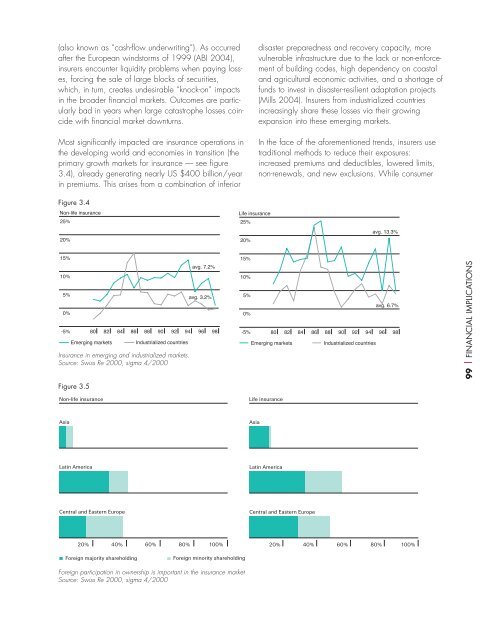

(also known as “cash-flow underwriting”). As occurredafter the European windstorms of 1999 (ABI 2004),insurers encounter liquidity problems when paying losses,forcing the sale of large blocks of securities,which, in turn, creates undesirable “knock-on” impactsin the broader financial markets. Outcomes are particularlybad in years when large catastrophe losses coincidewith financial market downturns.Most significantly impacted are insurance operations inthe developing world <strong>and</strong> economies in transition (theprimary growth markets for insurance — see figure3.4), already generating nearly US $400 billion/yearin premiums. This arises from a combination of inferiordisaster preparedness <strong>and</strong> recovery capacity, morevulnerable infrastructure due to the lack or non-enforcementof building codes, high dependency on coastal<strong>and</strong> agricultural <strong>economic</strong> activities, <strong>and</strong> a shortage offunds to invest in disaster-resilient adaptation projects(Mills 2004). Insurers from industrialized countriesincreasingly share these losses via their growingexpansion into these emerging markets.In the face of the aforementioned trends, insurers usetraditional methods to reduce their exposures:increased premiums <strong>and</strong> deductibles, lowered limits,non-renewals, <strong>and</strong> new exclusions. While consumerFigure 3.4Non-life insurance25%Life insurance25%avg. 13.3%20%20%15%10%5%0%-5%8082Emerging markets84Industrialized countriesInsurance in emerging <strong>and</strong> industrialized markets.Source: Swiss Re 2000, sigma 4/20008688909294avg. 7.2%avg. 3.2%969815%10%5%0%-5% 80 82Emerging markets8486avg. 6.7%88 90 92 94 96 98Industrialized countries99 | FINANCIAL IMPLICATIONSFigure 3.5Non-life insuranceLife insuranceAsiaAsiaLatin AmericaLatin AmericaCentral <strong>and</strong> Eastern EuropeCentral <strong>and</strong> Eastern Europe20% 40% 60% 80% 100%20% 40% 60% 80% 100%Foreign majority shareholdingForeign minority shareholdingForeign participation in ownership is important in the insurance marketSource: Swiss Re 2000, sigma 4/2000

100 | FINANCIAL IMPLICATIONSdem<strong>and</strong> for insurance increases at first, it evolves intoreduced willingness to pay <strong>and</strong> some shift from the useof insurance to alternatives such as weather derivatives.As warned by the US Government AccountabilityOffice (GAO 2005), private insurers encounterincreasing difficulty in h<strong>and</strong>ling extreme weatherevents. As commercial insurability declines, dem<strong>and</strong>semerge to exp<strong>and</strong> existing government-provided insurancefor flood <strong>and</strong> crop loss, <strong>and</strong> to assume new risks(for example, for wildfires <strong>and</strong> windstorms). Cashstrappedgovernments, however, find that claims interferewith balancing their budgets (Changnon 2003)<strong>and</strong>, in turn, limit their coverage, with the result thatmore ultimate losses are shifted back to the individuals<strong>and</strong> businesses impacted by climate <strong>change</strong>.Compounding the problem, international aid for naturaldisasters continues its current decline as a percentageof donor country GDP (Mills 2004).<strong>Climate</strong> <strong>change</strong> accelerates several forms of unrelatedadverse structural <strong>change</strong> already underway in theinsurance industry. 6 This manifests as a rise in competitionamong insurers, significant consolidation due tothe reduced viability of small firms, increased riskexposure via globalization <strong>and</strong> a growing proportionof competing self-insurance <strong>and</strong> alternative risk transfermechanisms.CCF-II: SURPRISE IMPACTSA shift from gradual to non-linear impacts of climate<strong>change</strong> serves to intensify the adverse effects of CCF-I.Disruptions are greater <strong>and</strong> the <strong>economic</strong> cost of naturalcatastrophes rises at an increasing rate, with elevatedstress on insurers <strong>and</strong> reinsurers. This scenario isalso fundamentally different for insurers insofar asCCF-I entails relatively predictable <strong>change</strong>s that can(to a degree) be adjusted to, whereas CCF-II involvesa substantial increase in impacts <strong>and</strong> uncertainty, significantchallenges to the actuarial processes thatunderpin the insurance business.Life <strong>and</strong> <strong>health</strong> impacts are particularly amplified incomparison to the outcomes in CCF-I. Extreme heatcatastrophes become more common. Events on a parwith that seen in Europe in the summer of 2003 cometo the US with the result that offensive air masses ofunprecedented length range from almost 200% to over400% above average. Intensities also exceed thehottest summers over the past 60 years by a significantmargin. All-time records for maximum <strong>and</strong> high minimumtemperature are broken in large numbers of cities,with corresponding death rates five times that previouslyseen in typical summers. Aside from mortalities, hospitalizationstax hospital resources in emergencyroom(s) already hit hard by constrained budgets.Also due, in part, to temperature increases, the currenttrend towards increasingly damaging wildfires continues.Both a cause <strong>and</strong> impact of climate <strong>change</strong>,more fires set intentionally to clear forests <strong>and</strong> creategrazing l<strong>and</strong> in the developing world grow out of control(due to climate-<strong>change</strong> droughts <strong>and</strong> high winds).Such associated events caused an estimated US $9.3billion in <strong>economic</strong> damages in 1997 (CNN 2005).Another bad year in 2005 forced the closures ofKuala Lumpur’s largest harbor <strong>and</strong> most other businesses<strong>and</strong> manufacturing plants, as well as disruption totourism. A continuation of the trend results in a combinationof insured losses, with causes ranging from anupturn in respiratory disease to widespread businessinterruptions. Included in the impacts are well-insuredoffshore industries, based in industrialized countries.The combination of more aeroallergens, rising temperatures,greater humidity, more wildfire smoke, <strong>and</strong>more dust <strong>and</strong> particulates considerably exacerbatesupper respiratory disease (rhinitis, conjunctivitis, sinusitis),lower respiratory disease <strong>and</strong> cardiovasculardisease. Cases of asthma increase sharply. A 30%increase in cases would occur, raising the total toabout 400 million new cases per year by 2025.The baseline cost was US $13 billion/year in the USalone as of the mid-1990s (half of which are direct<strong>health</strong> care costs). If a 30% increase took place in theUS, the incremental cost of US $4 billion/year wouldbe on a par with that of a very large hurricane eachyear.With a continued rise in atmospheric CO2 concentrations<strong>and</strong> early arrival of spring, a significant jump inwinter <strong>and</strong> summer warming (for example, from acceleratedrelease of methane), is accompanied by a stepwiseadvance in the hydrological cycle, <strong>and</strong> ensuinggrowth of weeds, pollen <strong>and</strong> molds. Additionally, dust6Even in wealthy nations, governments are increasingly seeking to limit their financial exposures to natural disasters. As a case in point, therisk of residential flooding in the US is deemed largely uninsurable, which has given rise to a National Flood Insurance Program (NFIP), withmore than 4.2 million policies in force, representing nearly US $560 billion in coverage. The NFIP pays no more than US $250,000 perloss per household <strong>and</strong> US $500,000 for small businesses.

- Page 1 and 2:

Climate Change FuturesHealth, Ecolo

- Page 4 and 5:

Table of ContentsIntroductionPart I

- Page 6 and 7:

EXECUTIVE SUMMARYClimate is the con

- Page 8 and 9:

the past decade, an increasing prop

- Page 10 and 11:

THE CASE STUDIES IN BRIEFInfectious

- Page 12 and 13:

THE INSURER’S OVERVIEW:A UNIQUE P

- Page 14:

Regulators and governments can empl

- Page 17 and 18:

THE PROBLEM:CLIMATE IS CHANGING, FA

- Page 19 and 20:

Figure 1.3 GreenlandEXTREMESOne of

- Page 21 and 22:

20 | THE CLIMATE CONTEXT TODAYWholl

- Page 23 and 24:

Figure 1.5 Global Weather-Related L

- Page 25 and 26:

Climate signals in rising costs fro

- Page 27 and 28:

CLIMATE CHANGE CANOCCUR ABRUPTLYPer

- Page 29 and 30:

28 | THE CLIMATE CONTEXT TODAYCCF-I

- Page 31 and 32:

communities, salinizing ground wate

- Page 33 and 34:

Health is the final common pathway

- Page 35 and 36:

34 | INFECTIOUS AND RESPIRATORY DIS

- Page 37 and 38:

Figure 2.4 Malaria and Floods in Mo

- Page 39 and 40:

Figure 2.61920-1980CASE STUDIES38 |

- Page 41 and 42:

A MALARIA SUCCESSThe New York Times

- Page 43 and 44:

A new flavivirus, Usutu, akin to WN

- Page 45 and 46:

44 | INFECTIOUS AND RESPIRATORY DIS

- Page 47 and 48:

One analysis (Vanderhoof and Vander

- Page 49 and 50: BIODIVERSITYBUFFERS AGAINSTTHE SPRE

- Page 51 and 52: Figure 2.15 RagweedMOLDSLong-term f

- Page 53 and 54: ASTHMA COSTSTODAYexamples, the Afri

- Page 55 and 56: Stott et al. (2004) calculate that

- Page 57 and 58: In the summer of 2005, northern Spa

- Page 59 and 60: a better understanding of subpopula

- Page 61 and 62: 60 | EXTREME WEATHER EVENTSFLOODSFO

- Page 63 and 64: MOSQUITO- AND SOIL-BORNE DISEASESEC

- Page 65 and 66: Table 2.2 Direct and Indirect Healt

- Page 67 and 68: HEALTH AND ECOLOGICALIMPLICATIONSOu

- Page 69 and 70: 68 | NATURAL AND MANAGED SYSTEMSCAS

- Page 71 and 72: Figure 2.27 Soybean Sudden Death Sy

- Page 73 and 74: 72 | NATURAL AND MANAGED SYSTEMSCAS

- Page 75 and 76: 74 | NATURAL AND MANAGED SYSTEMSCAS

- Page 77 and 78: 76 | NATURAL AND MANAGED SYSTEMSCAS

- Page 79 and 80: 78 | NATURAL AND MANAGED SYSTEMSTHE

- Page 81 and 82: HARMFUL ALGALBLOOMSFigure 2.32 Red

- Page 83 and 84: 82 | NATURAL AND MANAGED SYSTEMSCAS

- Page 85 and 86: CASE STUDIES 84 | NATURAL AND MANAG

- Page 87 and 88: CASE STUDIES 86 | NATURAL AND MANAG

- Page 89 and 90: CASE STUDIES 88 | NATURAL AND MANAG

- Page 91 and 92: CASE STUDIES 90 | NATURAL AND MANAG

- Page 93 and 94: “Climate change is one of the wor

- Page 95 and 96: 94 | FINANCIAL IMPLICATIONS• Incr

- Page 97 and 98: Extreme weather events are a partic

- Page 99: 98 | FINANCIAL IMPLICATIONSTable 3.

- Page 103 and 104: 102 | FINANCIAL IMPLICATIONSClimate

- Page 105 and 106: These include:Solar Photovoltaic Pa

- Page 107 and 108: • Social and economic factors in

- Page 109 and 110: Finally, new technologies need to b

- Page 111 and 112: 110 | FINANCIAL IMPLICATIONSBRETTON

- Page 113: 112 | APPENDICESAppendix A. Summary

- Page 116 and 117: Table B.1 Summer Percentage Frequen

- Page 118 and 119: Climate sensitivity for small-scale

- Page 120 and 121: diffuse and do not manifest in sing

- Page 122 and 123: APPENDIX D.LIST OF PARTICIPANTS ATT

- Page 124: Carmenza RobledoGruppe OekologieEMP

- Page 127 and 128: 126 | BIBLIOGRAPHYBibliographyAAAAI

- Page 129 and 130: 128 | BIBLIOGRAPHYChordas, L. Epide

- Page 131 and 132: Ford, S.E. & Tripp, M.R. Diseases a

- Page 133 and 134: 132 | BIBLIOGRAPHYKalkstein, L. S.,

- Page 135 and 136: 134 | BIBLIOGRAPHYMills, E. The ins

- Page 137 and 138: 136 | BIBLIOGRAPHYRose, J. B., Epst

- Page 139 and 140: 138 | BIBLIOGRAPHYVandyk, J. K., Ba

- Page 142: Infectious and Respiratory Diseases