in the 21st Century

hTOE305aYVW

hTOE305aYVW

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

Formal F<strong>in</strong>ancial Inclusion <strong>in</strong> Kenya: Understand<strong>in</strong>g <strong>the</strong> Demand-Side Constra<strong>in</strong>ts 123<br />

variables, a 1% <strong>in</strong>crease <strong>in</strong> <strong>in</strong>come results <strong>in</strong> an 8.5% <strong>in</strong>crease <strong>in</strong> <strong>the</strong> likelihood<br />

of a person be<strong>in</strong>g banked. This result is slightly higher than <strong>the</strong> f<strong>in</strong>d<strong>in</strong>g of Beck<br />

(2011) us<strong>in</strong>g <strong>the</strong> 2009 F<strong>in</strong>Access data, where a 1% <strong>in</strong>crease <strong>in</strong> expenditure<br />

led to a 7% <strong>in</strong>crease <strong>in</strong> <strong>the</strong> likelihood of a person be<strong>in</strong>g banked. 13 This result<br />

is <strong>in</strong> l<strong>in</strong>e with what our conceptual framework would suggest. From a policy<br />

perspective, this tells us that this <strong>in</strong>crease <strong>in</strong> <strong>in</strong>come is chang<strong>in</strong>g <strong>the</strong> demand<br />

of those <strong>in</strong>voluntary excluded and <strong>in</strong>creas<strong>in</strong>g <strong>the</strong>ir access to formal bank<br />

products. Aga<strong>in</strong>, however, it is important to remember that chang<strong>in</strong>g <strong>the</strong> value<br />

proposition of bank products for different <strong>in</strong>come groups is also critical to <strong>the</strong><br />

uptake of <strong>the</strong>se products. Focus<strong>in</strong>g solely on <strong>in</strong>come without tailor<strong>in</strong>g <strong>the</strong>se<br />

bank products to better fit <strong>the</strong> needs of lower <strong>in</strong>come <strong>in</strong>dividuals misses an<br />

important opportunity to <strong>in</strong>crease access.<br />

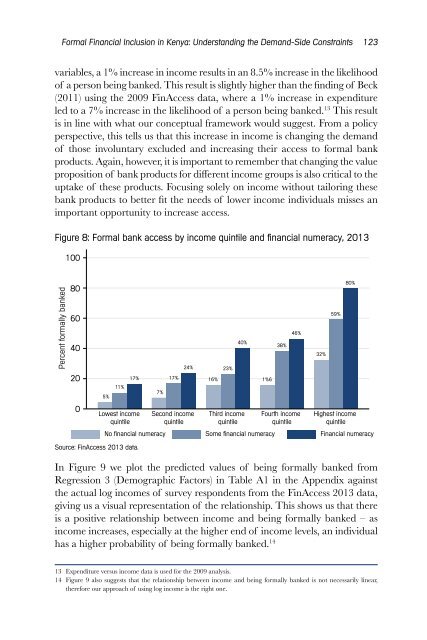

Figure 8: Formal bank access by <strong>in</strong>come qu<strong>in</strong>tile and f<strong>in</strong>ancial numeracy, 2013<br />

100<br />

Percent formally banked<br />

80<br />

60<br />

40<br />

20<br />

0<br />

5%<br />

11%<br />

17%<br />

Lowest <strong>in</strong>come<br />

qu<strong>in</strong>tile<br />

Source: F<strong>in</strong>Access 2013 data.<br />

7%<br />

17%<br />

24%<br />

Second <strong>in</strong>come<br />

qu<strong>in</strong>tile<br />

16%<br />

23%<br />

40%<br />

Third <strong>in</strong>come<br />

qu<strong>in</strong>tile<br />

1%6<br />

38%<br />

46%<br />

Fourth <strong>in</strong>come<br />

qu<strong>in</strong>tile<br />

32%<br />

59%<br />

80%<br />

Highest <strong>in</strong>come<br />

qu<strong>in</strong>tile<br />

No f<strong>in</strong>ancial numeracy Some f<strong>in</strong>ancial numeracy F<strong>in</strong>ancial numeracy<br />

In Figure 9 we plot <strong>the</strong> predicted values of be<strong>in</strong>g formally banked from<br />

Regression 3 (Demographic Factors) <strong>in</strong> Table A1 <strong>in</strong> <strong>the</strong> Appendix aga<strong>in</strong>st<br />

<strong>the</strong> actual log <strong>in</strong>comes of survey respondents from <strong>the</strong> F<strong>in</strong>Access 2013 data,<br />

giv<strong>in</strong>g us a visual representation of <strong>the</strong> relationship. This shows us that <strong>the</strong>re<br />

is a positive relationship between <strong>in</strong>come and be<strong>in</strong>g formally banked – as<br />

<strong>in</strong>come <strong>in</strong>creases, especially at <strong>the</strong> higher end of <strong>in</strong>come levels, an <strong>in</strong>dividual<br />

has a higher probability of be<strong>in</strong>g formally banked. 14<br />

13 Expenditure versus <strong>in</strong>come data is used for <strong>the</strong> 2009 analysis.<br />

14 Figure 9 also suggests that <strong>the</strong> relationship between <strong>in</strong>come and be<strong>in</strong>g formally banked is not necessarily l<strong>in</strong>ear,<br />

<strong>the</strong>refore our approach of us<strong>in</strong>g log <strong>in</strong>come is <strong>the</strong> right one.