atw 2017-12

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

<strong>atw</strong> Vol. 62 (<strong>2017</strong>) | Issue <strong>12</strong> ı December<br />

May <strong>2017</strong><br />

• Uranium: 19.25–22.75<br />

• Conversion: 5.00–5.50<br />

• Separative work: 42.00–45.00<br />

June <strong>2017</strong><br />

• Uranium: 19.25–20.50<br />

• Conversion: 5.55–5.50<br />

• Separative work: 42.00–43.00<br />

July <strong>2017</strong><br />

• Uranium: 19.75–20.50<br />

• Conversion: 4.75–5.25<br />

• Separative work: 42.00–43.00<br />

August <strong>2017</strong><br />

• Uranium: 19.50–21.00<br />

• Conversion: 4.75–5.25<br />

• Separative work: 41.00–43.00<br />

September <strong>2017</strong><br />

• Uranium: 19.75–20.75<br />

• Conversion: 4.60–5.10<br />

• Separative work: 40.50–42.00<br />

October <strong>2017</strong><br />

• Uranium: 19.90–20.50<br />

• Conversion: 4.50–5.25<br />

• Separative work: 40.00–43.00<br />

| | Source: Energy Intelligence<br />

www.energyintel.com<br />

Cross-border Price<br />

for Hard Coal<br />

Cross-border price for hard coal in<br />

[€/t TCE] and orders in [t TCE] for<br />

use in power plants (TCE: tonnes of<br />

coal equivalent, German border):<br />

20<strong>12</strong>: 93.02; 27,453,635<br />

2013: 79.<strong>12</strong>, 31,637,166<br />

2014: 72.94, 30,591,663<br />

2015: 67.90; 28,919,230<br />

2016: 67.07; 29,787,178<br />

I. quarter: 56.87; 8,627,347<br />

II. quarter: 56.<strong>12</strong>; 5,970,240<br />

III. quarter: 65.03, 7.257.041<br />

IV. quarter: 88.28; 7,932,550<br />

<strong>2017</strong>:<br />

I. quarter: 95.75; 8,385,071<br />

II. quarter: 86.40; 5,094,233<br />

| | Source: BAFA, some data provisional<br />

www.bafa.de<br />

EEX Trading Results<br />

October <strong>2017</strong><br />

(eex) In October <strong>2017</strong>, the European<br />

Energy Exchange (EEX) achieved a<br />

total volume of 261.3 TWh on its<br />

power derivatives markets (October<br />

2016: 410.1 TWh). The October<br />

volume comprised 141.1 TWh traded<br />

at EEX via Trade Registration with<br />

subsequent clearing. Clearing and<br />

settlement of all exchange transactions<br />

was executed by European<br />

Commodity Clearing (ECC). The shift<br />

in liquidity from the German-Austrian<br />

Phelix Future into the German Phelix<br />

DE future continued to increase<br />

in October. A large share of German<br />

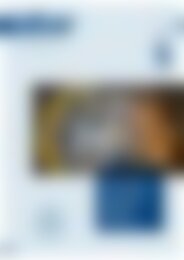

| | Uranium spot market prices from 1980 to <strong>2017</strong> and from 2006 to <strong>2017</strong>. The price range is shown.<br />

In years with U.S. trade restrictions the unrestricted uranium spot market price is shown.<br />

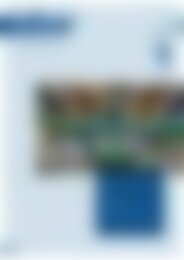

| | Separative work and conversion market price ranges from 2007 to <strong>2017</strong>. The price range is shown.<br />

)1<br />

In December 2009 Energy Intelligence changed the method of calculation for spot market prices. The change results in virtual price leaps.<br />

trading volumes for maturities<br />

beyond 2018 is already traded in<br />

the Phelix DE Futures on a regular<br />

basis. In October, options were<br />

traded on the basis of the new<br />

Phelix-DE Future for the first time.<br />

The Settlement Price for base<br />

load contract (Phelix Futures) with<br />

delivery in 2018 amounted to<br />

36.71 €/MWh. The Settlement Price<br />

for peak load contract (Phelix Futures)<br />

with delivery in 2018 amounted to<br />

45.17 €/MWh.<br />

On the EEX Market for emission<br />

allowances, 142.3 million tonnes of<br />

CO 2 (October 2016: 80.5 million<br />

tonnes of CO 2 ) were traded in October.<br />

The total volume increased to 77%.<br />

Primary market auctions contributed<br />

84.1 million tonnes of CO 2 to the<br />

total volume. At 55.7 million tonnes<br />

of CO 2 volumes on the derivatives<br />

market more than doubled compared<br />

to October 2016 (19.4 million tonnes<br />

of CO 2 ).<br />

The E-Carbix amounted to<br />

7.25 €/EUA, the EUA price with<br />

delivery in December <strong>2017</strong> amounted<br />

to 6.88/7.80 €/ EUA (min./max.).<br />

| | www.eex.com<br />

MWV Crude Oil/Product Prices<br />

September <strong>2017</strong><br />

(mwv) According to information and<br />

calculations by the Association of the<br />

German Petroleum Industry MWV e.V.<br />

in September <strong>2017</strong> the prices for super<br />

fuel, fuel oil and heating oil noted<br />

again slightly higher compared with<br />

the previous month August <strong>2017</strong>. The<br />

average gas station prices for Euro<br />

super consisted of 137.<strong>12</strong> €Cent<br />

( August <strong>2017</strong>: 134.01 €Cent, approx.<br />

+2.32 % in brackets: each information<br />

for pre vious month or rather previous<br />

month comparison), for diesel fuel of<br />

114.36 €Cent (1<strong>12</strong>.40; +1.74 %) and<br />

for heating oil (HEL) of 55.84 €Cent<br />

(53.24, +4.88 %).<br />

The tax share for super with a<br />

consumer price of 137.<strong>12</strong> €Cent<br />

(134.01 €Cent) consisted of<br />

65.45 €Cent (47.73 %, 65.45 €Cent)<br />

for the current constant mineral oil<br />

tax share and 21.89 €Cent (current<br />

rate: 19.0 % = const., 21.40 €Cent)<br />

for the value added tax. The product<br />

price (notation Rotterdam) consisted<br />

of 37.79 €Cent (27.56 %, 35.37 €Cent)<br />

and the gross margin consisted of<br />

11.99 €Cent (8.74 %; 11.79 €Cent).<br />

Thus the overall tax share for super<br />

results of 66.73 % (67.84 %).<br />

Worldwide crude oil prices<br />

(monthly average price OPEC/Brent/<br />

WTI, Source: U.S. EIA) were approx.<br />

+6.68 % (+5.<strong>12</strong> %) higher in<br />

September compared to August <strong>2017</strong>.<br />

The market showed a stable<br />

development with higher prices; each<br />

in US-$/bbl: OPEC basket: 53.44<br />

(49.60); UK-Brent: 56.15 (51.70);<br />

West Texas Inter mediate (WTI):<br />

49.82 (49.82).<br />

| | www.mwv.de<br />

769<br />

NEWS<br />

News