Emerging Trends in Real Estate® Europe 2006 - Urban Land Institute

Emerging Trends in Real Estate® Europe 2006 - Urban Land Institute

Emerging Trends in Real Estate® Europe 2006 - Urban Land Institute

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

without be<strong>in</strong>g pan-<strong>Europe</strong>an.”<br />

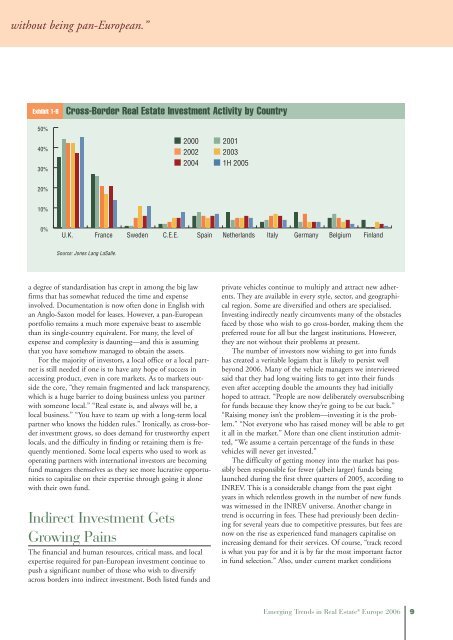

Exhibit 1-8 Cross-Border <strong>Real</strong> Estate Investment Activity by Country<br />

50%<br />

40%<br />

30%<br />

20%<br />

10%<br />

0%<br />

Source: Jones Lang LaSalle.<br />

a degree of standardisation has crept <strong>in</strong> among the big law<br />

firms that has somewhat reduced the time and expense<br />

<strong>in</strong>volved. Documentation is now often done <strong>in</strong> English with<br />

an Anglo-Saxon model for leases. However, a pan-<strong>Europe</strong>an<br />

portfolio rema<strong>in</strong>s a much more expensive beast to assemble<br />

than its s<strong>in</strong>gle-country equivalent. For many, the level of<br />

expense and complexity is daunt<strong>in</strong>g—and this is assum<strong>in</strong>g<br />

that you have somehow managed to obta<strong>in</strong> the assets.<br />

For the majority of <strong>in</strong>vestors, a local office or a local partner<br />

is still needed if one is to have any hope of success <strong>in</strong><br />

access<strong>in</strong>g product, even <strong>in</strong> core markets. As to markets outside<br />

the core, “they rema<strong>in</strong> fragmented and lack transparency,<br />

which is a huge barrier to do<strong>in</strong>g bus<strong>in</strong>ess unless you partner<br />

with someone local.” “<strong>Real</strong> estate is, and always will be, a<br />

local bus<strong>in</strong>ess.” “You have to team up with a long-term local<br />

partner who knows the hidden rules.” Ironically, as cross-border<br />

<strong>in</strong>vestment grows, so does demand for trustworthy expert<br />

locals, and the difficulty <strong>in</strong> f<strong>in</strong>d<strong>in</strong>g or reta<strong>in</strong><strong>in</strong>g them is frequently<br />

mentioned. Some local experts who used to work as<br />

operat<strong>in</strong>g partners with <strong>in</strong>ternational <strong>in</strong>vestors are becom<strong>in</strong>g<br />

fund managers themselves as they see more lucrative opportunities<br />

to capitalise on their expertise through go<strong>in</strong>g it alone<br />

with their own fund.<br />

Indirect Investment Gets<br />

Grow<strong>in</strong>g Pa<strong>in</strong>s<br />

■ 2000 ■ 2001<br />

■ 2002 ■ 2003<br />

■ 2004 ■ 1H 2005<br />

U.K. France Sweden C.E.E. Spa<strong>in</strong> Netherlands Italy Germany Belgium F<strong>in</strong>land<br />

The f<strong>in</strong>ancial and human resources, critical mass, and local<br />

expertise required for pan-<strong>Europe</strong>an <strong>in</strong>vestment cont<strong>in</strong>ue to<br />

push a significant number of those who wish to diversify<br />

across borders <strong>in</strong>to <strong>in</strong>direct <strong>in</strong>vestment. Both listed funds and<br />

private vehicles cont<strong>in</strong>ue to multiply and attract new adherents.<br />

They are available <strong>in</strong> every style, sector, and geographical<br />

region. Some are diversified and others are specialised.<br />

Invest<strong>in</strong>g <strong>in</strong>directly neatly circumvents many of the obstacles<br />

faced by those who wish to go cross-border, mak<strong>in</strong>g them the<br />

preferred route for all but the largest <strong>in</strong>stitutions. However,<br />

they are not without their problems at present.<br />

The number of <strong>in</strong>vestors now wish<strong>in</strong>g to get <strong>in</strong>to funds<br />

has created a veritable logjam that is likely to persist well<br />

beyond <strong>2006</strong>. Many of the vehicle managers we <strong>in</strong>terviewed<br />

said that they had long wait<strong>in</strong>g lists to get <strong>in</strong>to their funds<br />

even after accept<strong>in</strong>g double the amounts they had <strong>in</strong>itially<br />

hoped to attract. “People are now deliberately oversubscrib<strong>in</strong>g<br />

for funds because they know they’re go<strong>in</strong>g to be cut back.”<br />

“Rais<strong>in</strong>g money isn’t the problem—<strong>in</strong>vest<strong>in</strong>g it is the problem.”<br />

“Not everyone who has raised money will be able to get<br />

it all <strong>in</strong> the market.” More than one client <strong>in</strong>stitution admitted,<br />

“We assume a certa<strong>in</strong> percentage of the funds <strong>in</strong> these<br />

vehicles will never get <strong>in</strong>vested.”<br />

The difficulty of gett<strong>in</strong>g money <strong>in</strong>to the market has possibly<br />

been responsible for fewer (albeit larger) funds be<strong>in</strong>g<br />

launched dur<strong>in</strong>g the first three quarters of 2005, accord<strong>in</strong>g to<br />

INREV. This is a considerable change from the past eight<br />

years <strong>in</strong> which relentless growth <strong>in</strong> the number of new funds<br />

was witnessed <strong>in</strong> the INREV universe. Another change <strong>in</strong><br />

trend is occurr<strong>in</strong>g <strong>in</strong> fees. These had previously been decl<strong>in</strong><strong>in</strong>g<br />

for several years due to competitive pressures, but fees are<br />

now on the rise as experienced fund managers capitalise on<br />

<strong>in</strong>creas<strong>in</strong>g demand for their services. Of course, “track record<br />

is what you pay for and it is by far the most important factor<br />

<strong>in</strong> fund selection.” Also, under current market conditions<br />

<strong>Emerg<strong>in</strong>g</strong> <strong>Trends</strong> <strong>in</strong> <strong>Real</strong> Estate ® <strong>Europe</strong> <strong>2006</strong> 9