Emerging Trends in Real Estate® Europe 2006 - Urban Land Institute

Emerging Trends in Real Estate® Europe 2006 - Urban Land Institute

Emerging Trends in Real Estate® Europe 2006 - Urban Land Institute

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

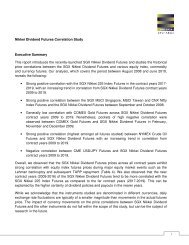

Exhibit 2-3<br />

Change <strong>in</strong> Availability of Equity Capital<br />

for <strong>Real</strong> Estate by Source Location<br />

Middle East<br />

United States<br />

United K<strong>in</strong>gdom<br />

Asia<br />

Spa<strong>in</strong><br />

Other <strong>Europe</strong>an<br />

Countries<br />

France<br />

Australia<br />

Germany<br />

Netherlands<br />

Italy<br />

■ <strong>2006</strong> ■ 2005<br />

6.60<br />

6.56<br />

6.53<br />

6.46<br />

6.47<br />

6.68<br />

6.47<br />

6.2<br />

6.4<br />

6.65<br />

6.25<br />

6.07<br />

6.1<br />

6.18<br />

6.07<br />

6.08<br />

6.02<br />

5.56<br />

5.96<br />

5.96<br />

5.81<br />

5.83<br />

0.0<br />

1<br />

4.5<br />

5<br />

9.0<br />

9<br />

Very Large Same Very Large<br />

Decl<strong>in</strong>e Increase<br />

Source: <strong>Emerg<strong>in</strong>g</strong> <strong>Trends</strong> <strong>in</strong> <strong>Real</strong> Estate <strong>Europe</strong> <strong>2006</strong> survey.<br />

public confidence <strong>in</strong> the sector. Changes are also be<strong>in</strong>g proposed<br />

by the fund management <strong>in</strong>dustry body, the BVI, <strong>in</strong><br />

hopes this will stem the outflows that are threaten<strong>in</strong>g to spiral<br />

out of control. The outlook is so uncerta<strong>in</strong> at the time of<br />

writ<strong>in</strong>g that no one knows whether this will be a short-lived<br />

scare or the onset of a contagion that will force many more<br />

funds to freeze.<br />

Massive redemptions from those funds with significant exposure<br />

to the German real estate market started <strong>in</strong> December 2003<br />

and escalated well <strong>in</strong>to 2005. However, dur<strong>in</strong>g the course of last<br />

year it appeared that the funds had restored public confidence<br />

sufficiently to conta<strong>in</strong> the worst of the damage. Parent <strong>in</strong>stitutions<br />

of troubled funds had been purchas<strong>in</strong>g fund units and<br />

buy<strong>in</strong>g assets from the fund portfolios at book value <strong>in</strong> order to<br />

reliquefy their offspr<strong>in</strong>g. Like the participants <strong>in</strong> the best-known<br />

example of game theory, “the prisoners’ dilemma,” these parent<br />

firms realised that if they all supported their funds until the<br />

German market picked up, they could potentially f<strong>in</strong>d an<br />

orderly way out of difficulty. Then, one parent bank broke<br />

ranks and refused to support their fund—<strong>in</strong>deed, they took<br />

the unprecedented step of freez<strong>in</strong>g it—and the fragile, hardwon<br />

confidence of the public was sent <strong>in</strong>to a tailsp<strong>in</strong>. A<br />

month later, two more funds were frozen. The problems that<br />

underlie the mass redemptions from the latter were corporate<br />

governance– rather than performance-related. Nevertheless,<br />

there is an escalat<strong>in</strong>g feel<strong>in</strong>g of panic seiz<strong>in</strong>g the entire openended<br />

fund market.<br />

German assets dom<strong>in</strong>ate the portfolios of the largest and<br />

oldest open-ended funds. These “historic big battleships from<br />

the 1960s” own some “old and not very structurally sound<br />

stuff” as well as the impressive new assets that take pride of<br />

place <strong>in</strong> their annual reports. Their allocations are heavily<br />

weighted towards offices, and book values are well <strong>in</strong> excess<br />

of market values <strong>in</strong> some cases. This is partly because of the<br />

characteristics of the officially mandated method for valu<strong>in</strong>g<br />

fund assets (described <strong>in</strong> our 2005 edition of <strong>Emerg<strong>in</strong>g</strong> <strong>Trends</strong>)<br />

but also partially due to the ill-judged use of that valuation<br />

methodology. The book values rely on assumptions about<br />

future rents and occupancy, and the optimistic estimates for<br />

these factors used by some funds’ valuers have led to systematic<br />

overvaluation of German offices for the past several years.<br />

“The problem is epidemic. You can’t take a few assets out of a<br />

fund and solve it.”<br />

The difference between market and book valuations of<br />

German office assets <strong>in</strong> some open-ended funds is purported<br />

to range between 10 and 30 percent. The bank that first<br />

decided to freeze its fund did so <strong>in</strong> front of a revaluation that<br />

could take up to one-sixth off of its total value, accord<strong>in</strong>g to<br />

news reports. And the current reductions may not be the end<br />

of the story. A lot of older secondary office space is overrented<br />

and now be<strong>in</strong>g abandoned <strong>in</strong> favour of new prime<br />

office space at cheaper rents with long rent-free periods.<br />

“Who is go<strong>in</strong>g to lease this tired old space <strong>in</strong> a stagnant economy<br />

with a shr<strong>in</strong>k<strong>in</strong>g workforce?” “A lot of the secondary<br />

office will never be relet.”<br />

Revelations about the valuation of fund assets are dest<strong>in</strong>ed<br />

to change the way they are overseen and possibly the frequency<br />

with which they are done. It is also likely to lead to<br />

more external regulation of the open-ended fund <strong>in</strong>dustry.<br />

However, some are question<strong>in</strong>g whether the <strong>in</strong>dustry has a<br />

future, particularly if a successful G-REIT structure is <strong>in</strong>troduced.<br />

“Open-ended funds are flawed <strong>in</strong> their present form.<br />

It’s illogical to have a liquid fund based on illiquid assets.”<br />

“The REIT is a far more jo<strong>in</strong>ed-up f<strong>in</strong>ancial concept and it<br />

will replace open-ended funds.” Some open-ended fund managers<br />

are already plann<strong>in</strong>g to float G-REITs when they are<br />

<strong>Emerg<strong>in</strong>g</strong> <strong>Trends</strong> <strong>in</strong> <strong>Real</strong> Estate ® <strong>Europe</strong> <strong>2006</strong> 17