The economic effects of EU-reforms in corporate income tax systems

The economic effects of EU-reforms in corporate income tax systems

The economic effects of EU-reforms in corporate income tax systems

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

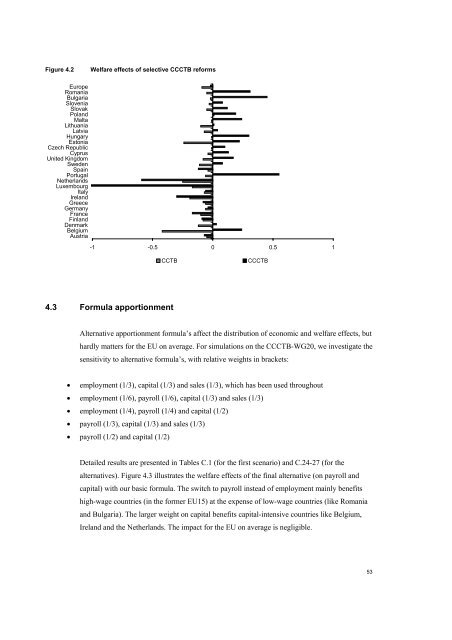

Figure 4.2<br />

Welfare <strong>effects</strong> <strong>of</strong> selective CCCTB <strong>reforms</strong><br />

Europe<br />

Romania<br />

Bulgaria<br />

Slovenia<br />

Slovak<br />

Poland<br />

Malta<br />

Lithuania<br />

Latvia<br />

Hungary<br />

Estonia<br />

Czech Republic<br />

Cyprus<br />

United K<strong>in</strong>gdom<br />

Sweden<br />

Spa<strong>in</strong><br />

Portugal<br />

Netherlands<br />

Luxembourg<br />

Italy<br />

Ireland<br />

Greece<br />

Germany<br />

France<br />

F<strong>in</strong>land<br />

Denmark<br />

Belgium<br />

Austria<br />

-1 -0.5 0 0.5 1<br />

CCTB<br />

CCCTB<br />

4.3 Formula apportionment<br />

Alternative apportionment formula’s affect the distribution <strong>of</strong> <strong>economic</strong> and welfare <strong>effects</strong>, but<br />

hardly matters for the <strong>EU</strong> on average. For simulations on the CCCTB-WG20, we <strong>in</strong>vestigate the<br />

sensitivity to alternative formula’s, with relative weights <strong>in</strong> brackets:<br />

• employment (1/3), capital (1/3) and sales (1/3), which has been used throughout<br />

• employment (1/6), payroll (1/6), capital (1/3) and sales (1/3)<br />

• employment (1/4), payroll (1/4) and capital (1/2)<br />

• payroll (1/3), capital (1/3) and sales (1/3)<br />

• payroll (1/2) and capital (1/2)<br />

Detailed results are presented <strong>in</strong> Tables C.1 (for the first scenario) and C.24-27 (for the<br />

alternatives). Figure 4.3 illustrates the welfare <strong>effects</strong> <strong>of</strong> the f<strong>in</strong>al alternative (on payroll and<br />

capital) with our basic formula. <strong>The</strong> switch to payroll <strong>in</strong>stead <strong>of</strong> employment ma<strong>in</strong>ly benefits<br />

high-wage countries (<strong>in</strong> the former <strong>EU</strong>15) at the expense <strong>of</strong> low-wage countries (like Romania<br />

and Bulgaria). <strong>The</strong> larger weight on capital benefits capital-<strong>in</strong>tensive countries like Belgium,<br />

Ireland and the Netherlands. <strong>The</strong> impact for the <strong>EU</strong> on average is negligible.<br />

53