RiskMetrics⢠âTechnical Document

RiskMetrics⢠âTechnical Document

RiskMetrics⢠âTechnical Document

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

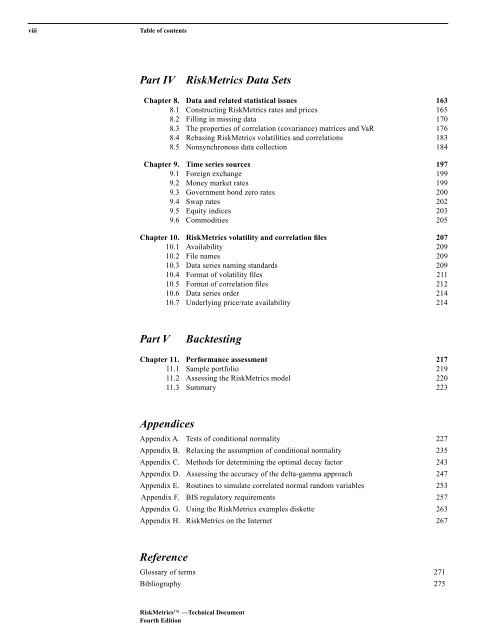

viii<br />

Table of contents<br />

Part IV RiskMetrics Data Sets<br />

Chapter 8. Data and related statistical issues 163<br />

8.1 Constructing RiskMetrics rates and prices 165<br />

8.2 Filling in missing data 170<br />

8.3 The properties of correlation (covariance) matrices and VaR 176<br />

8.4 Rebasing RiskMetrics volatilities and correlations 183<br />

8.5 Nonsynchronous data collection 184<br />

Chapter 9. Time series sources 197<br />

9.1 Foreign exchange 199<br />

9.2 Money market rates 199<br />

9.3 Government bond zero rates 200<br />

9.4 Swap rates 202<br />

9.5 Equity indices 203<br />

9.6 Commodities 205<br />

Chapter 10. RiskMetrics volatility and correlation files 207<br />

10.1 Availability 209<br />

10.2 File names 209<br />

10.3 Data series naming standards 209<br />

10.4 Format of volatility files 211<br />

10.5 Format of correlation files 212<br />

10.6 Data series order 214<br />

10.7 Underlying price/rate availability 214<br />

Part V<br />

Backtesting<br />

Chapter 11. Performance assessment 217<br />

11.1 Sample portfolio 219<br />

11.2 Assessing the RiskMetrics model 220<br />

11.3 Summary 223<br />

Appendices<br />

Appendix A. Tests of conditional normality 227<br />

Appendix B. Relaxing the assumption of conditional normality 235<br />

Appendix C. Methods for determining the optimal decay factor 243<br />

Appendix D. Assessing the accuracy of the delta-gamma approach 247<br />

Appendix E. Routines to simulate correlated normal random variables 253<br />

Appendix F. BIS regulatory requirements 257<br />

Appendix G. Using the RiskMetrics examples diskette 263<br />

Appendix H. RiskMetrics on the Internet 267<br />

Reference<br />

Glossary of terms 271<br />

Bibliography 275<br />

RiskMetrics —Technical <strong>Document</strong><br />

Fourth Edition