Interim Report - TEEB

Interim Report - TEEB

Interim Report - TEEB

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

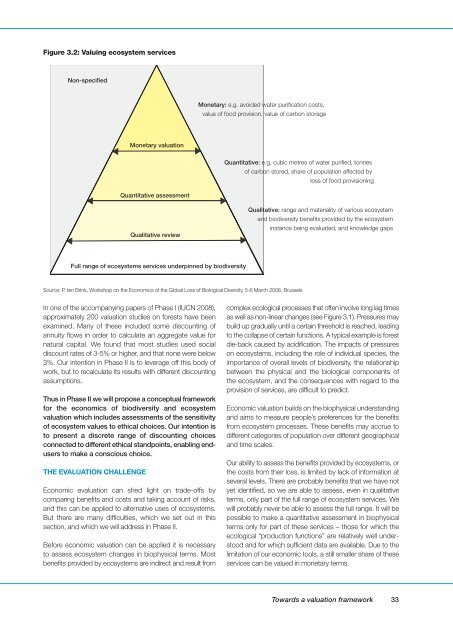

Figure 3.2: Valuing ecosystem services<br />

Non-specified<br />

Monetary: e.g. avoided water purification costs,<br />

value of food provision, value of carbon storage<br />

Monetary valuation<br />

Quantitative: e.g. cubic metres of water purified, tonnes<br />

of carbon stored, share of population affected by<br />

loss of food provisioning<br />

Quantitative assessment<br />

Qualitative review<br />

Qualitative: range and materiality of various ecosystem<br />

and biodiversity benefits provided by the ecosystem<br />

instance being evaluated, and knowledge gaps<br />

Full range of ecosystems services underpinned by biodiversity<br />

Source: P. ten Brink, Workshop on the Economics of the Global Loss of Biological Diversity, 5-6 March 2008, Brussels<br />

In one of the accompanying papers of Phase I (IUCN 2008),<br />

approximately 200 valuation studies on forests have been<br />

examined. Many of these included some discounting of<br />

annuity flows in order to calculate an aggregate value for<br />

natural capital. We found that most studies used social<br />

discount rates of 3-5% or higher, and that none were below<br />

3%. Our intention in Phase II is to leverage off this body of<br />

work, but to recalculate its results with different discounting<br />

assumptions.<br />

Thus in Phase II we will propose a conceptual framework<br />

for the economics of biodiversity and ecosystem<br />

valuation which includes assessments of the sensitivity<br />

of ecosystem values to ethical choices. Our intention is<br />

to present a discrete range of discounting choices<br />

connected to different ethical standpoints, enabling endusers<br />

to make a conscious choice.<br />

THE EVALUATION CHALLENGE<br />

Economic evaluation can shed light on trade-offs by<br />

comparing benefits and costs and taking account of risks,<br />

and this can be applied to alternative uses of ecosystems.<br />

But there are many difficulties, which we set out in this<br />

section, and which we will address in Phase II.<br />

Before economic valuation can be applied it is necessary<br />

to assess ecosystem changes in biophysical terms. Most<br />

benefits provided by ecosystems are indirect and result from<br />

complex ecological processes that often involve long lag times<br />

as well as non-linear changes (see Figure 3.1). Pressures may<br />

build up gradually until a certain threshold is reached, leading<br />

to the collapse of certain functions. A typical example is forest<br />

die-back caused by acidification. The impacts of pressures<br />

on ecosystems, including the role of individual species, the<br />

importance of overall levels of biodiversity, the relationship<br />

between the physical and the biological components of<br />

the ecosystem, and the consequences with regard to the<br />

provision of services, are difficult to predict.<br />

Economic valuation builds on the biophysical understanding<br />

and aims to measure people’s preferences for the benefits<br />

from ecosystem processes. These benefits may accrue to<br />

different categories of population over different geographical<br />

and time scales.<br />

Our ability to assess the benefits provided by ecosystems, or<br />

the costs from their loss, is limited by lack of information at<br />

several levels. There are probably benefits that we have not<br />

yet identified, so we are able to assess, even in qualitative<br />

terms, only part of the full range of ecosystem services. We<br />

will probably never be able to assess the full range. It will be<br />

possible to make a quantitative assessment in biophysical<br />

terms only for part of these services – those for which the<br />

ecological “production functions” are relatively well understood<br />

and for which sufficient data are available. Due to the<br />

limitation of our economic tools, a still smaller share of these<br />

services can be valued in monetary terms.<br />

Towards a valuation framework<br />

33