- Page 2 and 3:

This page intentionally left blank.

- Page 4 and 5:

CopyrightDrake Software User’s Ma

- Page 6 and 7:

Table of ContentsDrake Software Use

- Page 8 and 9:

Table of ContentsDrake Software Use

- Page 10 and 11:

What’s New in Drake for 2008Drake

- Page 12 and 13:

What’s New in Drake for 2008Drake

- Page 14 and 15:

Contacting Drake SupportDrake Softw

- Page 16 and 17:

InstallationDrake Software User’s

- Page 18 and 19:

Running Drake on a NetworkDrake Sof

- Page 20 and 21:

Running Drake on a NetworkDrake Sof

- Page 22 and 23:

Software SetupDrake Software User

- Page 24 and 25:

Software SetupDrake Software User

- Page 26 and 27:

Software SetupDrake Software User

- Page 28 and 29:

Software SetupDrake Software User

- Page 30 and 31:

Software SetupDrake Software User

- Page 32 and 33:

Software SetupDrake Software User

- Page 34 and 35:

Software SetupDrake Software User

- Page 36 and 37:

Software SetupDrake Software User

- Page 38 and 39:

Software SetupDrake Software User

- Page 40 and 41:

Software SetupDrake Software User

- Page 42 and 43:

Software SetupDrake Software User

- Page 44 and 45:

Software SetupDrake Software User

- Page 46 and 47:

Software SetupDrake Software User

- Page 48 and 49:

Software SetupDrake Software User

- Page 50 and 51:

Software SetupDrake Software User

- Page 52 and 53:

Software SetupDrake Software User

- Page 54 and 55:

Making Changes on the FlyDrake Soft

- Page 56 and 57:

Making Changes on the FlyDrake Soft

- Page 58 and 59:

Making Changes on the FlyDrake Soft

- Page 60 and 61:

Making Changes on the FlyDrake Soft

- Page 62 and 63:

Logging In and OutDrake Software Us

- Page 64 and 65:

Creating and Opening ReturnsDrake S

- Page 66 and 67:

Data EntryDrake Software User’s M

- Page 68 and 69:

Data EntryDrake Software User’s M

- Page 70 and 71:

Data EntryDrake Software User’s M

- Page 72 and 73:

Data EntryDrake Software User’s M

- Page 74 and 75:

About State ReturnsDrake Software U

- Page 76 and 77:

Prior-Year UpdatesDrake Software Us

- Page 78 and 79:

Prior-Year UpdatesDrake Software Us

- Page 80 and 81:

Organizers and ProformasDrake Softw

- Page 82 and 83:

SchedulerDrake Software User’s Ma

- Page 84 and 85:

SchedulerDrake Software User’s Ma

- Page 86 and 87:

SchedulerDrake Software User’s Ma

- Page 88 and 89:

SchedulerDrake Software User’s Ma

- Page 90 and 91:

E-filing PreparationDrake Software

- Page 92 and 93:

Taxpayer DemographicsDrake Software

- Page 94 and 95:

ExemptionsDrake Software User’s M

- Page 96 and 97:

Personal Service Income (W-2, 1099-

- Page 98 and 99:

Passive and Investment Income (1099

- Page 100 and 101:

Passive and Investment Income (1099

- Page 102 and 103:

Self-Employment Income (Schedule C)

- Page 104 and 105:

Sales of AssetsDrake Software User

- Page 106 and 107:

Sales of AssetsDrake Software User

- Page 108 and 109:

Sales of AssetsDrake Software User

- Page 110 and 111:

Retirement Income (1099-R, etc.)Dra

- Page 112 and 113:

Supplemental IncomeDrake Software U

- Page 114 and 115:

Farm IncomeDrake Software User’s

- Page 116 and 117:

Social Security and Railroad Benefi

- Page 118 and 119:

Educator ExpensesDrake Software Use

- Page 120 and 121:

Self-Employment AdjustmentsDrake So

- Page 122 and 123:

PenaltiesDrake Software User’s Ma

- Page 124 and 125:

Domestic Production Activities Dedu

- Page 126 and 127:

Alternative Minimum TaxDrake Softwa

- Page 128 and 129:

Elderly/Disabled CreditDrake Softwa

- Page 130 and 131:

Retirement Savings Contributions Cr

- Page 132 and 133:

Household Employment TaxesDrake Sof

- Page 134 and 135:

Estimated TaxesDrake Software User

- Page 136 and 137:

Estimated TaxesDrake Software User

- Page 138 and 139:

Earned Income Credit (EIC)Drake Sof

- Page 140 and 141:

Additional Child Tax Credit and Com

- Page 142 and 143:

Recovery Rebate CreditDrake Softwar

- Page 144 and 145:

Electronic Funds Withdrawal (Direct

- Page 146 and 147:

Third Party DesigneeDrake Software

- Page 148 and 149:

DepreciationDrake Software User’s

- Page 150 and 151:

DepreciationDrake Software User’s

- Page 152 and 153:

DepreciationDrake Software User’s

- Page 154 and 155:

Auto ExpensesDrake Software User’

- Page 156 and 157:

Auto ExpensesDrake Software User’

- Page 158 and 159:

Office in HomeDrake Software User

- Page 160 and 161:

Net Operating LossesDrake Software

- Page 162 and 163:

Special ReturnsDrake Software User

- Page 164 and 165:

Requests, Claims, and Other FormsDr

- Page 166 and 167:

Requests, Claims, and Other FormsDr

- Page 168 and 169:

Special Features in Data EntryDrake

- Page 170 and 171:

Special Features in Data EntryDrake

- Page 172 and 173:

Special Features in Data EntryDrake

- Page 174 and 175:

Calculation ResultsDrake Software U

- Page 176 and 177:

Viewing and Printing a ReturnDrake

- Page 178 and 179:

Viewing and Printing a ReturnDrake

- Page 180 and 181:

Viewing and Printing a ReturnDrake

- Page 182 and 183:

Setting Up View/Print OptionsDrake

- Page 184 and 185:

Archive ManagerDrake Software User

- Page 186 and 187:

Archive ManagerDrake Software User

- Page 188 and 189:

Preparing to E-FileDrake Software U

- Page 190 and 191:

E-filing a ReturnDrake Software Use

- Page 192 and 193:

E-filing a ReturnDrake Software Use

- Page 194 and 195:

E-filing a ReturnDrake Software Use

- Page 196 and 197:

EF Override Options in Data EntryDr

- Page 198 and 199:

EF Override Options in Data EntryDr

- Page 200 and 201:

EF DatabaseDrake Software User’s

- Page 202 and 203:

Online EF DatabaseDrake Software Us

- Page 204 and 205:

Online EF DatabaseDrake Software Us

- Page 206 and 207:

Online EF DatabaseDrake Software Us

- Page 208 and 209:

About State FilingDrake Software Us

- Page 210 and 211:

About Bank ProductsDrake Software U

- Page 212 and 213:

About Bank ProductsDrake Software U

- Page 214 and 215:

About Bank ProductsDrake Software U

- Page 216 and 217:

Preparing to Offer Bank ProductsDra

- Page 218 and 219:

Bank Product TransmissionDrake Soft

- Page 220 and 221:

Processing the Loan CheckDrake Soft

- Page 222 and 223:

Troubleshooting Check PrintingDrake

- Page 224 and 225:

Cancellations, Tracking, & Post-Sea

- Page 226 and 227:

About Client StatusesDrake Software

- Page 228 and 229:

Customizing the DisplayDrake Softwa

- Page 230 and 231:

CSM ReportsDrake Software User’s

- Page 232 and 233:

Admin-only FeaturesDrake Software U

- Page 234 and 235:

Online SupportDrake Software User

- Page 236 and 237:

Online SupportDrake Software User

- Page 238 and 239:

Online SupportDrake Software User

- Page 240 and 241:

Online SupportDrake Software User

- Page 242 and 243:

Software SupportDrake Software User

- Page 244 and 245:

Interactive SupportDrake Software U

- Page 246 and 247:

Interactive SupportDrake Software U

- Page 248 and 249:

Interactive SupportDrake Software U

- Page 250 and 251:

Fax Cover Letter for SupportDrake S

- Page 252 and 253:

Install UpdatesDrake Software User

- Page 254 and 255:

Download FontsDrake Software User

- Page 256 and 257:

File MaintenanceDrake Software User

- Page 258 and 259:

File MaintenanceDrake Software User

- Page 260 and 261:

File MaintenanceDrake Software User

- Page 262 and 263:

File MaintenanceDrake Software User

- Page 264 and 265:

File MaintenanceDrake Software User

- Page 266 and 267: LettersDrake Software User’s Manu

- Page 268 and 269: AmortizationDrake Software User’s

- Page 270 and 271: Install State ProgramsDrake Softwar

- Page 272 and 273: Quick EstimatorDrake Software User

- Page 274 and 275: Report ManagerDrake Software User

- Page 276 and 277: Setting Up a ReportDrake Software U

- Page 278 and 279: Setting Up a ReportDrake Software U

- Page 280 and 281: Filter ManagerDrake Software User

- Page 282 and 283: Filter ManagerDrake Software User

- Page 284 and 285: Report ViewerDrake Software User’

- Page 286 and 287: Fixed Asset ManagerDrake Software U

- Page 288 and 289: Hash TotalsDrake Software User’s

- Page 290 and 291: Document ManagerDrake Software User

- Page 292 and 293: Document ManagerDrake Software User

- Page 294 and 295: Document ManagerDrake Software User

- Page 296 and 297: Document ManagerDrake Software User

- Page 298 and 299: Document ManagerDrake Software User

- Page 300 and 301: Tax PlannerDrake Software User’s

- Page 302 and 303: Tax PlannerDrake Software User’s

- Page 304 and 305: Tax PlannerDrake Software User’s

- Page 306 and 307: Client Write-UpDrake Software User

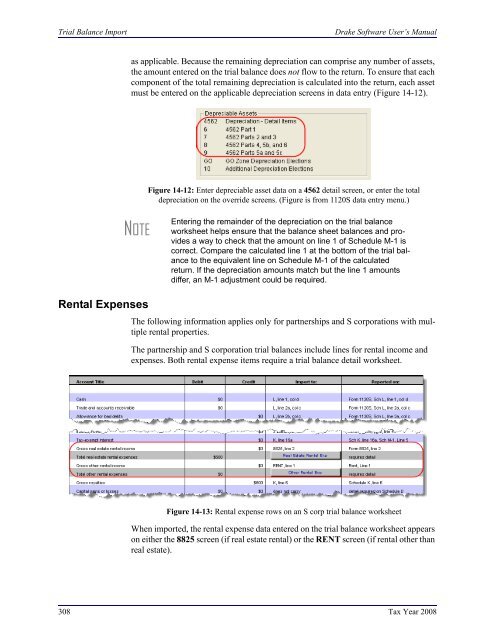

- Page 308 and 309: Trial Balance ImportDrake Software

- Page 310 and 311: Trial Balance ImportDrake Software

- Page 312 and 313: Trial Balance ImportDrake Software

- Page 314 and 315: Trial Balance ImportDrake Software

- Page 318 and 319: Binary AttachmentsDrake Software Us

- Page 320 and 321: Binary AttachmentsDrake Software Us

- Page 322 and 323: Appendix A: Preseason ChecklistDrak

- Page 324 and 325: Appendix A: Preseason ChecklistDrak

- Page 326 and 327: PROCESS: E-FILING FEDERAL RETURNSCo

- Page 328 and 329: Appendix C: KeywordsDrake Software

- Page 330 and 331: Appendix C: KeywordsDrake Software

- Page 332 and 333: Appendix C: KeywordsDrake Software

- Page 334 and 335: Appendix D: Acronyms & Abbreviation

- Page 336 and 337: Appendix D: Acronyms & Abbreviation

- Page 338 and 339: Appendix E: State E-filing Mandates

- Page 340 and 341: Appendix E: State E-filing Mandates

- Page 342 and 343: Appendix E: State E-filing Mandates

- Page 344 and 345: Prepare to use TrialBalance ImportC

- Page 346 and 347: Index2008 Drake Softwarebank name d

- Page 348 and 349: Index2008 Drake Softwarechanging 18

- Page 350 and 351: Index2008 Drake Softwareestimating

- Page 352 and 353: Index2008 Drake SoftwareForm 8867 (

- Page 354 and 355: Index2008 Drake Softwareand moving

- Page 356 and 357: Index2008 Drake SoftwareReal-Time L

- Page 358 and 359: Index2008 Drake SoftwareSSN, see So