GST and ITCs are calculated, reported, and paid or refunded on a regular periodic basis. The report<strong>in</strong>g period ofa registrant may be monthly, quarterly or annually, depend<strong>in</strong>g upon the registrant's revenues and whether theregistrant elects to report on a more frequent basis than is otherwise required.OTHER COMMODITY TAXESBus<strong>in</strong>esses <strong>in</strong>volved <strong>in</strong> br<strong>in</strong>g<strong>in</strong>g goods <strong>in</strong>to Canada, or manufactur<strong>in</strong>g and sell<strong>in</strong>g goods <strong>in</strong> Canada, may also beaffected, either directly or <strong>in</strong>directly, by certa<strong>in</strong> other taxes and duties imposed <strong>in</strong> Canada. Most productsimported <strong>in</strong>to Canada are subject to two types of commodity taxes <strong>in</strong> addition to the GST, namely customsduties and prov<strong>in</strong>cial sales tax. Products such as alcohol and tobacco are subject to additional excise duties.PROVINCIAL SALES TAXEvery prov<strong>in</strong>ce, except Alberta, imposes some form of sales tax. In New Brunswick, Nova Scotia andNewfoundland, harmonized sales tax (“HST”) is charged at a s<strong>in</strong>gle rate of 13% <strong>in</strong>stead of GST and prov<strong>in</strong>cialsales tax. HST is levied under the ETA and follows the GST rules described above. Québec levies its own versionof the GST, which is described below. Ontario, Manitoba, Saskatchewan and British Columbia currently imposevary<strong>in</strong>g forms of a retail sales tax (commonly referred to as prov<strong>in</strong>cial sales tax or "PST"). Ontario and BritishColumbia are set to harmonize their sales tax system with that of the GST, effective July 1, 2010. The comb<strong>in</strong>edrate of tax will rema<strong>in</strong> at 13% for Ontario and 12% for British Columbia, and the tax will be levied under the ETAas HST. A vendor <strong>in</strong> the <strong>bus<strong>in</strong>ess</strong> of sell<strong>in</strong>g taxable goods or provid<strong>in</strong>g taxable services <strong>in</strong> any one or more ofthese prov<strong>in</strong>ces is generally required to obta<strong>in</strong> a vendor's permit from each relevant prov<strong>in</strong>cial government andto collect and remit PST on taxable sales with<strong>in</strong> that prov<strong>in</strong>ce.Québec has a goods and services tax system which closely parallels the concepts and provisions of the GST(<strong>in</strong>clud<strong>in</strong>g the requirement to register and collect tax). Québec Sales Tax ("QST") applies at the rate of 7.5% tothe price of goods and services <strong>in</strong>clusive of GST, mak<strong>in</strong>g the effective rate 7.875% for a comb<strong>in</strong>ed rate with GSTof 12.875%. The Québec tax authority is responsible for the collection and adm<strong>in</strong>istration of both GST and QST<strong>in</strong> Québec.QST will <strong>in</strong>crease to 8.5% on January 1, 2011, for a comb<strong>in</strong>ed rate of 13.925%, and to 9.5% on January 1, 2012,for a total comb<strong>in</strong>ed rate with GST of 14.975%.OTHER TAXES - PROPERTY TAXES AND FEESLAND TRANSFER TAXESMany prov<strong>in</strong>ces impose tax on the transfer of real property (<strong>in</strong>clud<strong>in</strong>g with respect to certa<strong>in</strong> leasehold<strong>in</strong>terests). Ontario transferees of real property are generally liable for land transfer tax at a rate of 1.5% of theconsideration paid. Québec also levies a land transfer tax at similar rates. Certa<strong>in</strong> deferrals and exemptionsmay be available <strong>in</strong> respect of land transfer tax, particularly <strong>in</strong> the context of qualify<strong>in</strong>g <strong>in</strong>ter-corporate transfersamongst affiliated corporations. Certa<strong>in</strong> transfers of real property may also be subject to GST (and QST or HSTdepend<strong>in</strong>g on the relevant prov<strong>in</strong>cial jurisdiction).The City of Montréal levies land transfer take at slightly higher rates than the rest of Québec.The City of Toronto also imposes tax on the transfer of real property located <strong>in</strong> Toronto at a rate of up to 1.5%,which is <strong>in</strong> addition to the Ontario land transfer tax described above.MUNICIPAL PROPERTY TAXESReal property owners may also be subject to municipal property taxes and levies, generally based upon theassessed value of the property. The tax rates vary from one jurisdiction to another.Tax Considerations 91

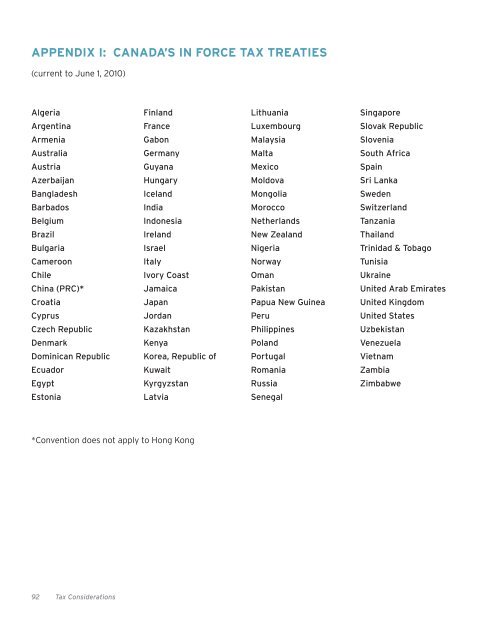

APPENDIX I: CANADA’S IN FORCE TAX TREATIES(current to June 1, 2010)AlgeriaArgent<strong>in</strong>aArmeniaAustraliaAustriaAzerbaijanBangladeshBarbadosBelgiumBrazilBulgariaCameroonChileCh<strong>in</strong>a (PRC)*CroatiaCyprusCzech RepublicDenmarkDom<strong>in</strong>ican RepublicEcuadorEgyptEstoniaF<strong>in</strong>landFranceGabonGermanyGuyanaHungaryIcelandIndiaIndonesiaIrelandIsraelItalyIvory CoastJamaicaJapanJordanKazakhstanKenyaKorea, Republic ofKuwaitKyrgyzstanLatviaLithuaniaLuxembourgMalaysiaMaltaMexicoMoldovaMongoliaMoroccoNetherlandsNew ZealandNigeriaNorwayOmanPakistanPapua New Gu<strong>in</strong>eaPeruPhilipp<strong>in</strong>esPolandPortugalRomaniaRussiaSenegalS<strong>in</strong>gaporeSlovak RepublicSloveniaSouth AfricaSpa<strong>in</strong>Sri LankaSwedenSwitzerlandTanzaniaThailandTr<strong>in</strong>idad & TobagoTunisiaUkra<strong>in</strong>eUnited Arab EmiratesUnited K<strong>in</strong>gdomUnited StatesUzbekistanVenezuelaVietnamZambiaZimbabwe*Convention does not apply to Hong Kong92 Tax Considerations

- Page 1 and 2:

DOING BUSINESSIN CANADAYOUR COMPLET

- Page 3 and 4:

ONTENTSTABLE OF CONTENTSINTRODUCTIO

- Page 5 and 6:

IntroductionPOLITICAL AND CONSTITUT

- Page 7 and 8:

5RealEstateIndustrial and Intellect

- Page 9 and 10:

accordance with directions from the

- Page 11 and 12:

TITLE INSURANCE, TITLE OPINIONS AND

- Page 13 and 14:

11EnvironmentalLawIndustrial and In

- Page 15 and 16:

commercial activities, or carrying

- Page 17 and 18:

The federal government currently re

- Page 19 and 20:

17Types ofBusiness OrganizationIndu

- Page 21 and 22:

provincial law cannot do so as of r

- Page 23 and 24:

partnership, limited partners’ li

- Page 25 and 26:

parties. In Québec, joint venturer

- Page 27 and 28:

25Financing aBusiness OperationIndu

- Page 29 and 30:

The Civil Code of Québec provides

- Page 31 and 32:

29CorporateGovernanceIndustrial and

- Page 33 and 34:

Instrument 58-101. The practices re

- Page 35 and 36:

33CompetitionLawIndustrial and Inte

- Page 37 and 38:

BID-RIGGINGBid rigging is any agree

- Page 39 and 40: anticompetitive agreements among co

- Page 41 and 42: 39ForeignInvestmentIndustrial and I

- Page 43 and 44: apply for Canadian citizenship. (Pe

- Page 45 and 46: (D)GENERAL REVIEW THRESHOLDSThe fol

- Page 47 and 48: there be an "acquisition of control

- Page 49 and 50: Industrial and Intellectual Propert

- Page 51 and 52: to perform or cause them to be perf

- Page 53 and 54: Registration grants an exclusive ri

- Page 55 and 56: PIPEDA applies in all provinces of

- Page 57 and 58: Employment LawCanadian employment l

- Page 59 and 60: displacement, laying-off, suspensio

- Page 61 and 62: easonable cause to believe that the

- Page 63 and 64: 63Retirement Plans, EmployeeBenefit

- Page 65 and 66: • funding;• eligibility;• pen

- Page 67 and 68: 67Temporary Entry andPermanent Resi

- Page 69 and 70: INTERNATIONAL AGREEMENTSIn recent y

- Page 71 and 72: immigrant in another class, he or s

- Page 73 and 74: 73Bankruptcy andInsolvency Proceedi

- Page 75 and 76: BANKRUPTCYBankruptcy results in the

- Page 77 and 78: INTERNATIONAL BANKRUPTCYASSETS LOCA

- Page 79 and 80: Tax ConsiderationsThis chapter prov

- Page 81 and 82: TAX REPORTINGAnnual Tax ReturnsCana

- Page 83 and 84: Québec has legislation that limits

- Page 85 and 86: Amendments, SIFTs and their unithol

- Page 87 and 88: Conversely, where a Canadian reside

- Page 89: A person, whether resident in Canad

- Page 93: TORONTODAVIES WARD PHILLIPS & VINEB