Creating

Doing Business in 2006 -- Creating Jobs - Caribbean Elections

Doing Business in 2006 -- Creating Jobs - Caribbean Elections

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

GETTING CREDIT 37<br />

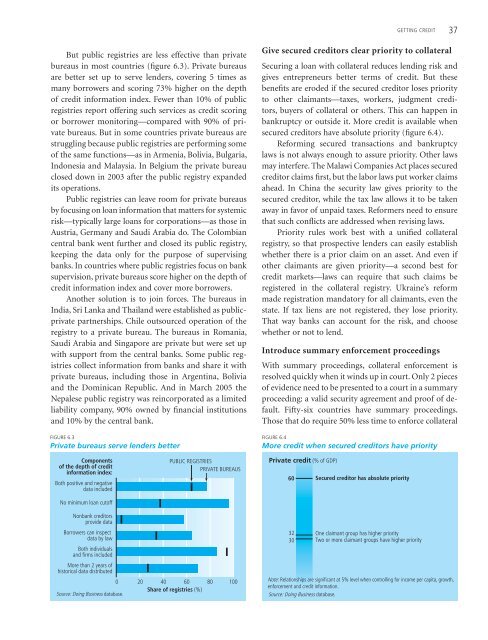

But public registries are less effective than private<br />

bureaus in most countries (figure 6.3). Private bureaus<br />

are better set up to serve lenders, covering 5 times as<br />

many borrowers and scoring 73% higher on the depth<br />

of credit information index. Fewer than 10% of public<br />

registries report offering such services as credit scoring<br />

or borrower monitoring—compared with 90% of private<br />

bureaus. But in some countries private bureaus are<br />

struggling because public registries are performing some<br />

of the same functions—as in Armenia, Bolivia, Bulgaria,<br />

Indonesia and Malaysia. In Belgium the private bureau<br />

closed down in 2003 after the public registry expanded<br />

its operations.<br />

Public registries can leave room for private bureaus<br />

by focusing on loan information that matters for systemic<br />

risk—typically large loans for corporations—as those in<br />

Austria, Germany and Saudi Arabia do. The Colombian<br />

central bank went further and closed its public registry,<br />

keeping the data only for the purpose of supervising<br />

banks. In countries where public registries focus on bank<br />

supervision, private bureaus score higher on the depth of<br />

credit information index and cover more borrowers.<br />

Another solution is to join forces. The bureaus in<br />

India, Sri Lanka and Thailand were established as publicprivate<br />

partnerships. Chile outsourced operation of the<br />

registry to a private bureau. The bureaus in Romania,<br />

Saudi Arabia and Singapore are private but were set up<br />

with support from the central banks. Some public registries<br />

collect information from banks and share it with<br />

private bureaus, including those in Argentina, Bolivia<br />

and the Dominican Republic. And in March 2005 the<br />

Nepalese public registry was reincorporated as a limited<br />

liability company, 90% owned by financial institutions<br />

and 10% by the central bank.<br />

<br />

<br />

Give secured creditors clear priority to collateral<br />

Securing a loan with collateral reduces lending risk and<br />

gives entrepreneurs better terms of credit. But these<br />

benefits are eroded if the secured creditor loses priority<br />

to other claimants—taxes, workers, judgment creditors,<br />

buyers of collateral or others. This can happen in<br />

bankruptcy or outside it. More credit is available when<br />

secured creditors have absolute priority (figure 6.4).<br />

Reforming secured transactions and bankruptcy<br />

laws is not always enough to assure priority. Other laws<br />

may interfere. The Malawi Companies Act places secured<br />

creditor claims first, but the labor laws put worker claims<br />

ahead. In China the security law gives priority to the<br />

secured creditor, while the tax law allows it to be taken<br />

away in favor of unpaid taxes. Reformers need to ensure<br />

that such conflicts are addressed when revising laws.<br />

Priority rules work best with a unified collateral<br />

registry, so that prospective lenders can easily establish<br />

whether there is a prior claim on an asset. And even if<br />

other claimants are given priority—a second best for<br />

credit markets—laws can require that such claims be<br />

registered in the collateral registry. Ukraine’s reform<br />

made registration mandatory for all claimants, even the<br />

state. If tax liens are not registered, they lose priority.<br />

That way banks can account for the risk, and choose<br />

whether or not to lend.<br />

Introduce summary enforcement proceedings<br />

With summary proceedings, collateral enforcement is<br />

resolved quickly when it winds up in court. Only 2 pieces<br />

of evidence need to be presented to a court in a summary<br />

proceeding: a valid security agreement and proof of default.<br />

Fifty-six countries have summary proceedings.<br />

Those that do require 50% less time to enforce collateral