The Future of Online Grocery Shopping in the United ... - Kantar Retail

The Future of Online Grocery Shopping in the United ... - Kantar Retail

The Future of Online Grocery Shopping in the United ... - Kantar Retail

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

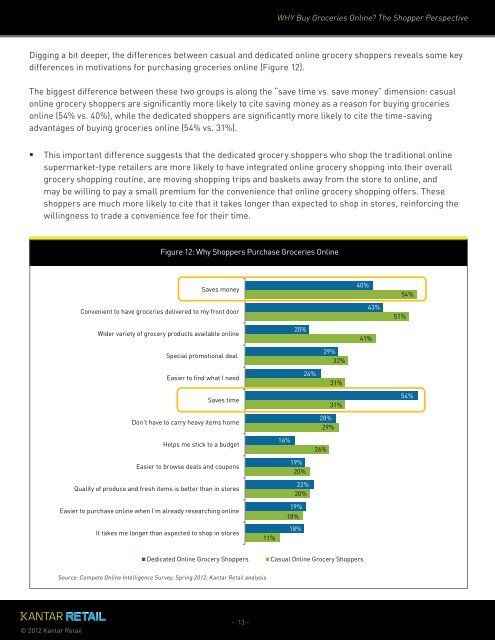

Digg<strong>in</strong>g a bit deeper, <strong>the</strong> differences between casual and dedicated onl<strong>in</strong>e grocery shoppers reveals some key<br />

differences <strong>in</strong> motivations for purchas<strong>in</strong>g groceries onl<strong>in</strong>e (Figure 12).<br />

<strong>The</strong> biggest difference between <strong>the</strong>se two groups is along <strong>the</strong> “save time vs. save money” dimension: casual<br />

onl<strong>in</strong>e grocery shoppers are significantly more likely to cite sav<strong>in</strong>g money as a reason for buy<strong>in</strong>g groceries<br />

onl<strong>in</strong>e (54% vs. 40%), while <strong>the</strong> dedicated shoppers are significantly more likely to cite <strong>the</strong> time-sav<strong>in</strong>g<br />

advantages <strong>of</strong> buy<strong>in</strong>g groceries onl<strong>in</strong>e (54% vs. 31%).<br />

This important difference suggests that <strong>the</strong> dedicated grocery shoppers who shop <strong>the</strong> traditional onl<strong>in</strong>e<br />

supermarket-type retailers are more likely to have <strong>in</strong>tegrated onl<strong>in</strong>e grocery shopp<strong>in</strong>g <strong>in</strong>to <strong>the</strong>ir overall<br />

grocery shopp<strong>in</strong>g rout<strong>in</strong>e, are mov<strong>in</strong>g shopp<strong>in</strong>g trips and baskets away from <strong>the</strong> store to onl<strong>in</strong>e, and<br />

may be will<strong>in</strong>g to pay a small premium for <strong>the</strong> convenience that onl<strong>in</strong>e grocery shopp<strong>in</strong>g <strong>of</strong>fers. <strong>The</strong>se<br />

shoppers are much more likely to cite that it takes longer than expected to shop <strong>in</strong> stores, re<strong>in</strong>forc<strong>in</strong>g <strong>the</strong><br />

will<strong>in</strong>gness to trade a convenience fee for <strong>the</strong>ir time.<br />

© 2012 <strong>Kantar</strong> <strong>Retail</strong><br />

Figure 12: Why Shoppers Purchase Groceries <strong>Onl<strong>in</strong>e</strong><br />

Saves money<br />

Convenient to have groceries delivered to my front door<br />

Wider variety <strong>of</strong> grocery products available onl<strong>in</strong>e<br />

Special promotional deal<br />

Easier to f<strong>in</strong>d what I need<br />

Saves time<br />

Don’t have to carry heavy items home<br />

Helps me stick to a budget<br />

Easier to browse deals and coupons<br />

Quality <strong>of</strong> produce and fresh items is better than <strong>in</strong> stores<br />

Easier to purchase onl<strong>in</strong>e when I’m already research<strong>in</strong>g onl<strong>in</strong>e<br />

It takes me longer than expected to shop <strong>in</strong> stores<br />

Source: Compete <strong>Onl<strong>in</strong>e</strong> Intelligence Survey, Spr<strong>in</strong>g 2012; <strong>Kantar</strong> <strong>Retail</strong> analysis<br />

- 13 -<br />

11%<br />

WHY Buy Groceries <strong>Onl<strong>in</strong>e</strong>? <strong>The</strong> Shopper Perspective<br />

16%<br />

20%<br />

19%<br />

20%<br />

22%<br />

20%<br />

19%<br />

18%<br />

18%<br />

24%<br />

28%<br />

29%<br />

26%<br />

29%<br />

32%<br />

31%<br />

31%<br />

Dedicated <strong>Onl<strong>in</strong>e</strong> <strong>Grocery</strong> Shoppers Casual <strong>Onl<strong>in</strong>e</strong> <strong>Grocery</strong> Shoppers<br />

40%<br />

41%<br />

43%<br />

51%<br />

54%<br />

54%