The Future of Online Grocery Shopping in the United ... - Kantar Retail

The Future of Online Grocery Shopping in the United ... - Kantar Retail

The Future of Online Grocery Shopping in the United ... - Kantar Retail

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

© 2012 <strong>Kantar</strong> <strong>Retail</strong><br />

WHO Shops <strong>Onl<strong>in</strong>e</strong> for Groceries?<br />

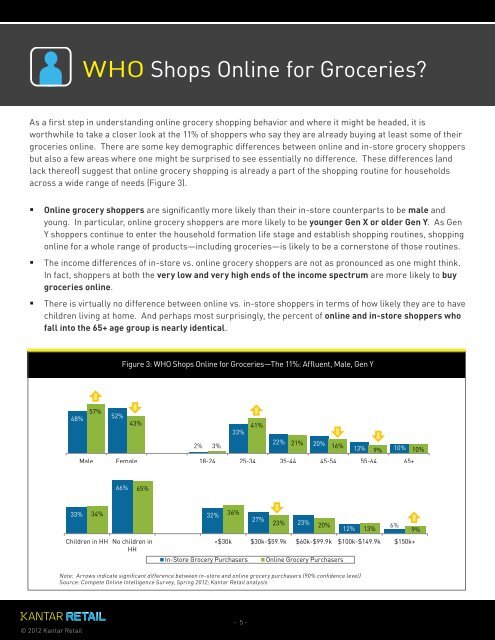

As a first step <strong>in</strong> understand<strong>in</strong>g onl<strong>in</strong>e grocery shopp<strong>in</strong>g behavior and where it might be headed, it is<br />

worthwhile to take a closer look at <strong>the</strong> 11% <strong>of</strong> shoppers who say <strong>the</strong>y are already buy<strong>in</strong>g at least some <strong>of</strong> <strong>the</strong>ir<br />

groceries onl<strong>in</strong>e. <strong>The</strong>re are some key demographic differences between onl<strong>in</strong>e and <strong>in</strong>-store grocery shoppers<br />

but also a few areas where one might be surprised to see essentially no difference. <strong>The</strong>se differences (and<br />

lack <strong>the</strong>re<strong>of</strong>) suggest that onl<strong>in</strong>e grocery shopp<strong>in</strong>g is already a part <strong>of</strong> <strong>the</strong> shopp<strong>in</strong>g rout<strong>in</strong>e for households<br />

across a wide range <strong>of</strong> needs (Figure 3).<br />

<strong>Onl<strong>in</strong>e</strong> grocery shoppers are significantly more likely than <strong>the</strong>ir <strong>in</strong>-store counterparts to be male and<br />

young. In particular, onl<strong>in</strong>e grocery shoppers are more likely to be younger Gen X or older Gen Y. As Gen<br />

Y shoppers cont<strong>in</strong>ue to enter <strong>the</strong> household formation life stage and establish shopp<strong>in</strong>g rout<strong>in</strong>es, shopp<strong>in</strong>g<br />

onl<strong>in</strong>e for a whole range <strong>of</strong> products—<strong>in</strong>clud<strong>in</strong>g groceries—is likely to be a cornerstone <strong>of</strong> those rout<strong>in</strong>es.<br />

<strong>The</strong> <strong>in</strong>come differences <strong>of</strong> <strong>in</strong>-store vs. onl<strong>in</strong>e grocery shoppers are not as pronounced as one might th<strong>in</strong>k.<br />

In fact, shoppers at both <strong>the</strong> very low and very high ends <strong>of</strong> <strong>the</strong> <strong>in</strong>come spectrum are more likely to buy<br />

groceries onl<strong>in</strong>e.<br />

<strong>The</strong>re is virtually no difference between onl<strong>in</strong>e vs. <strong>in</strong>-store shoppers <strong>in</strong> terms <strong>of</strong> how likely <strong>the</strong>y are to have<br />

children liv<strong>in</strong>g at home. And perhaps most surpris<strong>in</strong>gly, <strong>the</strong> percent <strong>of</strong> onl<strong>in</strong>e and <strong>in</strong>-store shoppers who<br />

fall <strong>in</strong>to <strong>the</strong> 65+ age group is nearly identical.<br />

Figure 3: WHO Shops <strong>Onl<strong>in</strong>e</strong> for Groceries—<strong>The</strong> 11%: Affluent, Male, Gen Y<br />

48%<br />

57%<br />

52%<br />

43%<br />

41%<br />

33%<br />

2% 3%<br />

22% 21% 20% 16% 13% 9% 10% 10%<br />

Male Female 18-24 25-34 35-44 45-54 55-64 65+<br />

33%<br />

34%<br />

66%<br />

65%<br />

Children <strong>in</strong> HH No children <strong>in</strong><br />

HH<br />

32%<br />

Note: Arrows <strong>in</strong>dicate significant difference between <strong>in</strong>-store and onl<strong>in</strong>e grocery purchasers (90% confidence level)<br />

Source: Compete <strong>Onl<strong>in</strong>e</strong> Intelligence Survey, Spr<strong>in</strong>g 2012; <strong>Kantar</strong> <strong>Retail</strong> analysis<br />

36%<br />

- 5 -<br />

27%<br />

23% 23% 20%<br />

12%<br />

6%<br />

13% 9%<br />