The Future of Online Grocery Shopping in the United ... - Kantar Retail

The Future of Online Grocery Shopping in the United ... - Kantar Retail

The Future of Online Grocery Shopping in the United ... - Kantar Retail

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

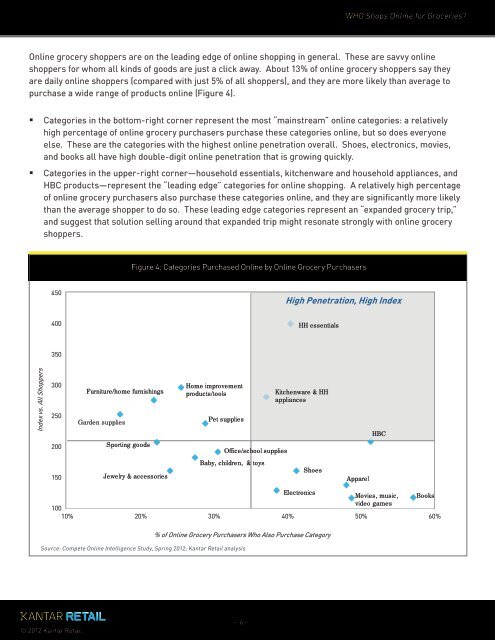

<strong>Onl<strong>in</strong>e</strong> grocery shoppers are on <strong>the</strong> lead<strong>in</strong>g edge <strong>of</strong> onl<strong>in</strong>e shopp<strong>in</strong>g <strong>in</strong> general. <strong>The</strong>se are savvy onl<strong>in</strong>e<br />

shoppers for whom all k<strong>in</strong>ds <strong>of</strong> goods are just a click away. About 13% <strong>of</strong> onl<strong>in</strong>e grocery shoppers say <strong>the</strong>y<br />

are daily onl<strong>in</strong>e shoppers (compared with just 5% <strong>of</strong> all shoppers), and <strong>the</strong>y are more likely than average to<br />

purchase a wide range <strong>of</strong> products onl<strong>in</strong>e (Figure 4).<br />

Index vs. All Shoppers<br />

Categories <strong>in</strong> <strong>the</strong> bottom-right corner represent <strong>the</strong> most “ma<strong>in</strong>stream” onl<strong>in</strong>e categories: a relatively<br />

high percentage <strong>of</strong> onl<strong>in</strong>e grocery purchasers purchase <strong>the</strong>se categories onl<strong>in</strong>e, but so does everyone<br />

else. <strong>The</strong>se are <strong>the</strong> categories with <strong>the</strong> highest onl<strong>in</strong>e penetration overall. Shoes, electronics, movies,<br />

and books all have high double-digit onl<strong>in</strong>e penetration that is grow<strong>in</strong>g quickly.<br />

Categories <strong>in</strong> <strong>the</strong> upper-right corner—household essentials, kitchenware and household appliances, and<br />

HBC products—represent <strong>the</strong> “lead<strong>in</strong>g edge” categories for onl<strong>in</strong>e shopp<strong>in</strong>g. A relatively high percentage<br />

<strong>of</strong> onl<strong>in</strong>e grocery purchasers also purchase <strong>the</strong>se categories onl<strong>in</strong>e, and <strong>the</strong>y are significantly more likely<br />

than <strong>the</strong> average shopper to do so. <strong>The</strong>se lead<strong>in</strong>g edge categories represent an “expanded grocery trip,”<br />

and suggest that solution sell<strong>in</strong>g around that expanded trip might resonate strongly with onl<strong>in</strong>e grocery<br />

shoppers.<br />

450<br />

400<br />

350<br />

300<br />

250<br />

200<br />

150<br />

© 2012 <strong>Kantar</strong> <strong>Retail</strong><br />

Furniture/home furnish<strong>in</strong>gs<br />

Garden supplies<br />

Sport<strong>in</strong>g goods<br />

Figure 4: Categories Purchased <strong>Onl<strong>in</strong>e</strong> by <strong>Onl<strong>in</strong>e</strong> <strong>Grocery</strong> Purchasers<br />

Jewelry & accessories<br />

Home improvement<br />

products/tools<br />

Pet supplies<br />

Office/school supplies<br />

Baby, children, & toys<br />

- 6 -<br />

WHO Shops <strong>Onl<strong>in</strong>e</strong> for Groceries?<br />

Electronics<br />

Movies, music, Books<br />

100<br />

video games<br />

10% 20% 30% 40% 50% 60%<br />

% <strong>of</strong> <strong>Onl<strong>in</strong>e</strong> <strong>Grocery</strong> Purchasers Who Also Purchase Category<br />

Source: Compete <strong>Onl<strong>in</strong>e</strong> Intelligence Study, Spr<strong>in</strong>g 2012; <strong>Kantar</strong> <strong>Retail</strong> analysis<br />

High Penetration, High Index<br />

HH essentials<br />

Kitchenware & HH<br />

appliances<br />

Shoes<br />

Apparel<br />

HBC