Feasibility Study of a Digital Platform for the delivery of UK ... - BFI

Feasibility Study of a Digital Platform for the delivery of UK ... - BFI

Feasibility Study of a Digital Platform for the delivery of UK ... - BFI

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>UK</strong> FILM COUNCIL<br />

The impact <strong>of</strong> BSkyB’s approach is likely to have a stifling effect on <strong>the</strong> immediate development <strong>of</strong> <strong>the</strong> a la carte Internet VoD market in<br />

<strong>the</strong> <strong>UK</strong> – given <strong>the</strong> plat<strong>for</strong>m’s scope and access to content. However, with studios now proactively encouraging <strong>the</strong> open Internet as a<br />

viable distribution plat<strong>for</strong>m, <strong>the</strong>re will be a replication <strong>of</strong> existing TV models by 2006 – that is, titles with <strong>the</strong> earlier PPV window finding<br />

an audience seeking newer titles, but not quite reaching <strong>the</strong> value <strong>of</strong> <strong>the</strong> pay-TV deals.<br />

Added to <strong>the</strong> equation are Apple and Sony, who are currently <strong>of</strong>fering video downloads via iTunes to <strong>the</strong> iPod (worldwide) and<br />

SonyConnect to PSPs (in Japan only). Apple is likely to quickly expand its premium content <strong>of</strong>fering out <strong>of</strong> <strong>the</strong> US, whilst Sony is planning<br />

to translate its model to <strong>the</strong> <strong>UK</strong> and Europe in 2006, <strong>of</strong>fering approximately 500 titles <strong>for</strong> PPV download, and, as suspected, <strong>for</strong> ‘digital<br />

sell-through’. The latter is a model which a number <strong>of</strong> o<strong>the</strong>r studios, including Disney and Warner Bros, are also seeking to exploit in <strong>the</strong><br />

longer term. The digital retail model might eventually debut simultaneously with DVD retail, and, as such, marry <strong>the</strong> pr<strong>of</strong>itable margins <strong>of</strong><br />

retail and on-demand <strong>delivery</strong> in one proposition. The key technical issue to be resolved yet is how to allow <strong>for</strong> download-to-burn rights<br />

whilst retaining copy protection on <strong>the</strong> home-made DVD. O<strong>the</strong>r service providers to watch include ISPs AOL (which is expected to launch<br />

services independently with Warner Bros and possibly in conjunction with an online DVD rentailer), and search engines Yahoo! and<br />

Google – both <strong>of</strong> which are in <strong>the</strong> early years <strong>of</strong> ambitious content distribution plans. As <strong>the</strong> situation stands, <strong>the</strong> first digital sell-through<br />

<strong>of</strong>fers should appear in <strong>the</strong> <strong>UK</strong> in 2006 and are likely to drive <strong>the</strong> market into 2010.<br />

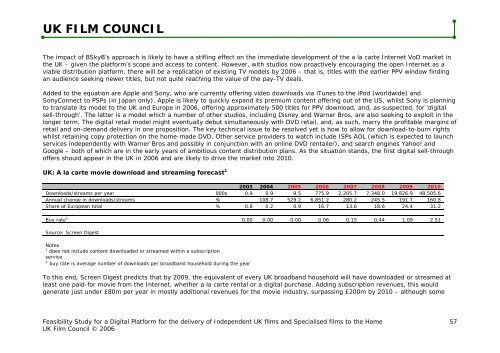

<strong>UK</strong>: A la carte movie download and streaming <strong>for</strong>ecast 1<br />

2003 2004 2005 2006 2007 2008 2009 2010<br />

Downloads/streams per year 000s 0.9 0.9 9.5 775.9 2,205.7 7,348.0 19,826.9 48,505.6<br />

Annual change in downloads/streams % 108.7 529.2 6,851.2 280.2 245.5 191.7 160.8<br />

Share <strong>of</strong> European total % 0.8 0.2 0.9 16.7 13.6 18.6 24.4 31.2<br />

Buy rate 2<br />

Source: Screen Digest<br />

Notes<br />

1<br />

does not include content downloaded or streamed within a subscription<br />

service<br />

2<br />

buy rate is average number <strong>of</strong> downloads per broadband household during <strong>the</strong> year<br />

0.00 0.00 0.00 0.06 0.15 0.44 1.09 2.51<br />

To this end, Screen Digest predicts that by 2009, <strong>the</strong> equivalent <strong>of</strong> every <strong>UK</strong> broadband household will have downloaded or streamed at<br />

least one paid-<strong>for</strong> movie from <strong>the</strong> Internet, whe<strong>the</strong>r a la carte rental or a digital purchase. Adding subscription revenues, this would<br />

generate just under £80m per year in mostly additional revenues <strong>for</strong> <strong>the</strong> movie industry, surpassing £200m by 2010 – although some<br />

<strong>Feasibility</strong> <strong>Study</strong> <strong>for</strong> a <strong>Digital</strong> <strong>Plat<strong>for</strong>m</strong> <strong>for</strong> <strong>the</strong> <strong>delivery</strong> <strong>of</strong> Independent <strong>UK</strong> films and Specialised films to <strong>the</strong> Home<br />

<strong>UK</strong> Film Council © 2006<br />

57