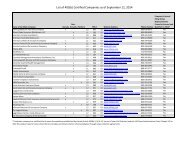

TRS 2011 Comprehensive Annual Financial Report

TRS 2011 Comprehensive Annual Financial Report

TRS 2011 Comprehensive Annual Financial Report

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

TEACHER RETIREMENT SYSTEM OF TEXAS COMPREHENSIVE ANNUAL FINANCIAL REPORT <strong>2011</strong><br />

Notes to the <strong>Financial</strong> Statements<br />

At August 31, <strong>2011</strong>, OPEB membership before actuarial adjustments consisted of the following:<br />

Retirees and beneficiaries<br />

receiving benefits 179,877*<br />

Active plan members 681,457<br />

Total 861,334<br />

*Excludes 6,182 dependent children<br />

B. CONTRIBUTIONS<br />

Funding for free basic coverage is provided by the program based upon public school district payroll. The State of Texas, active<br />

public school employee and reporting entities contribution rates and amounts collected are reflected in the table below for fiscal year<br />

<strong>2011</strong>. Per Texas Insurance Code, Chapter 1575, the public school contribution may not be less than 0.25% or greater than 0.75% of the<br />

salary of each active employee of the public school. Funding for optional coverage is provided by those participants selecting the optional<br />

coverage. Actuarial implications of the overall funding are determined by the system’s actuary.<br />

Contribution<br />

Rate<br />

Amount<br />

Active Employee .65% $ 183,808,580<br />

State 1.00 257,105,886<br />

<strong>Report</strong>ing Entities .55 155,471,641<br />

Federal or Private Funding Sources 1.00 25,784,985<br />

Total $ 622,171,092<br />

C The contributions shown above and premium contributions of $345,164,271 contribute toward the total plan expenditures of<br />

$1,039,738,174. Expenses for <strong>TRS</strong>-Care are recognized as retirees report claims and include a provision for estimated claims incurred<br />

but not yet received.<br />

The actuarial valuation as of August 31, <strong>2011</strong>, is similar to the actuarial valuations performed for the pension plan; however, certain<br />

economic and behavioral assumptions are unique to medical benefits. The demographic assumptions are identical to those used in the<br />

August 31, <strong>2011</strong> valuation for the pension plan.<br />

Additional valuation information follows:<br />

Valuation Date August 31, <strong>2011</strong><br />

Actuarial Cost Method<br />

Projected Unit Credit<br />

Amortization Method<br />

Level Percent, Open<br />

Remaining Amortization Period<br />

30 Years<br />

Asset Valuation Method<br />

Market<br />

Actuarial Assumptions:<br />

Investment Rate of Return * 5.25 %<br />

Projected Salary Increases * 4.25% to 7.25 %<br />

Weighted-Average at Valuation Date 5.62 %<br />

Payroll Growth Rate 3.50 %<br />

Health Care Trend Rates * 10.00% to 4.25 %**<br />

* Includes Inflation at 3.00%<br />

** .Initial rates are 10% for medical and 9.5% for prescriptions. The ultimate rate is 4.25% for both<br />

medical and prescriptions.<br />

FINANCIAL SECTION<br />

59