Annual Financial Statements 2011 of Bank Austria

Annual Financial Statements 2011 of Bank Austria

Annual Financial Statements 2011 of Bank Austria

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Management Report<br />

Management Report (CONTINUED)<br />

� UniCredit’s business model has proved effective especially in<br />

the difficult years following the financial market crisis, when customer<br />

centricity and customer business were the top priorities.<br />

– In early <strong>2011</strong> we completed organisational projects such as One4C.<br />

Proximity to customers was also the main idea behind strengthening<br />

local management in the matrix <strong>of</strong> Divisions and regions. More specifically,<br />

we streamlined the organisational structure and more<br />

clearly defined sub-segments <strong>of</strong> our sales network based on customer<br />

proximity, simplicity and specific needs. The main step in 2010<br />

was to combine customer-driven capital market activities with commercial<br />

banking business to form the Corporate & Investment <strong>Bank</strong>ing<br />

(CIB) Division and the bundling <strong>of</strong> proprietary trading activities in<br />

UniCredit <strong>Bank</strong>, Munich (previously Bayerische Hypo- und Vereinsbank<br />

AG), which involved the intra-group sale <strong>of</strong> UniCredit CAIB. The transfer<br />

<strong>of</strong> the SME sub-segment (small and medium-sized enterprises),<br />

also initiated in 2010, from the CIB Division to the F&SME <strong>Bank</strong>ing<br />

Division took place at the beginning <strong>of</strong> <strong>2011</strong>. For medium-sized<br />

companies (defined according to qualitative criteria and/or turnover<br />

between € 3 m and € 50 m), we introduced a targeted service model,<br />

implementing a decentralised sales network step by step with <strong>of</strong>fices<br />

in selected locations. At the end <strong>of</strong> <strong>2011</strong>, specialised customer service<br />

centres were available to this group <strong>of</strong> customers in 54 locations.<br />

After defining the target group <strong>of</strong> the top segment <strong>of</strong> private customers<br />

for Private <strong>Bank</strong>ing and completing the necessary transfer <strong>of</strong> customers<br />

from other segments in 2010, we set up a competence centre<br />

serving foundations in the Private <strong>Bank</strong>ing Division in <strong>2011</strong> and<br />

transferred customers from other business segments. ➔ For a meaningful<br />

comparison with the previous year, segment reporting figures<br />

for <strong>2011</strong> were adjusted to the new structure.<br />

– Our range <strong>of</strong> instruments for raising customer satisfaction –<br />

including customer surveys, feedback talks, mystery shopping, customer<br />

dialogues, internal standards <strong>of</strong> service and advice provided,<br />

training and ongoing measurement <strong>of</strong> customer satisfaction – is an<br />

integral part <strong>of</strong> business and has proved effective. This was confirmed<br />

in an audit, performed by specialists from the University <strong>of</strong> St. Gallen<br />

in <strong>2011</strong>, which resulted in <strong>Bank</strong> <strong>Austria</strong> being voted “<strong>Austria</strong>’s most<br />

customer-oriented service provider”. To maintain reputation levels<br />

and regain general confidence in banks following the disruptions<br />

caused by the financial market crisis, we simplified the product range,<br />

adjusted our internal performance incentives to focus on customer<br />

satisfaction and revised the way in which the bank presents itself to<br />

the public. With a number <strong>of</strong> charitable initiatives and a new overall<br />

sponsoring strategy, <strong>Bank</strong> <strong>Austria</strong> and its employees moreover underlined<br />

their intention to display solidarity within the community. ➔<br />

More details are included in the section on “<strong>Financial</strong> and non-<br />

financial performance indicators”.<br />

– External pressure on the banking sector to build risk buffers,<br />

increase capital ratios and fund business on a sustainable basis<br />

from local commercial sources as far as possible also prompted<br />

<strong>Bank</strong> <strong>Austria</strong> to adopt a more restrained approach in the growth<br />

markets <strong>of</strong> Central and Eastern Europe (CEE). While the commitment<br />

<strong>of</strong> <strong>Bank</strong> <strong>Austria</strong> and the entire UniCredit Group to CEE is<br />

unchanged, we are now differentiating on the basis <strong>of</strong> criteria such<br />

as market size and market position, in line with the requirement <strong>of</strong><br />

capital efficiency. We have suspended the ambitious branch expansion<br />

programme, which started in 2009, for the time being; in<br />

some cases, e.g. Hungary, the local investment climate was a<br />

factor considered in this decision. Quite generally, and despite the<br />

cross-regional approach, the business policy in CEE aimed at funding<br />

lending business from local sources to the -largest possible<br />

extent. The focal points <strong>of</strong> business policy were set out in a new<br />

multi-year plan in the third quarter <strong>of</strong> <strong>2011</strong>. ➔ See “Outlook for<br />

<strong>Bank</strong> <strong>Austria</strong>’s performance”.<br />

– In <strong>2011</strong> we made significant progress on the way towards the<br />

cross-regional bundling <strong>of</strong> back-<strong>of</strong>fice production and settlement<br />

functions (All4 Quality project) and unlocked cross-regional<br />

synergies with a view to reducing costs. We combined IT, transaction<br />

settlement, facility management, security and procurement in<br />

several steps. The first step was the bundling <strong>of</strong> the former IT companies<br />

UGIS (UniCredit Global Information Services) and BAGIS<br />

(<strong>Bank</strong> <strong>Austria</strong> Global Information Services) in UGIS <strong>Austria</strong> as at<br />

1 July <strong>2011</strong>. In a second step, carried out in the course <strong>of</strong> <strong>2011</strong>,<br />

some units <strong>of</strong> <strong>Bank</strong> <strong>Austria</strong> Procurement and Security and the Strategic<br />

Procurement Coordination CEE unit were integrated in UGIS<br />

<strong>Austria</strong>. The third step was the integration <strong>of</strong> the back-<strong>of</strong>fice services<br />

provider UCBP (UniCredit Business Partner GmbH), including<br />

its branches in Poland and Romania, with UGIS <strong>Austria</strong> turning into<br />

UBIS <strong>Austria</strong>, a subsidiary <strong>of</strong> the global UniCredit Business Integrated<br />

Solutions S.C.p.A. based in Milan, as at 1 February 2012.<br />

This service provider is unique in the European financial sector and<br />

gives customers – i.e. the banks in UniCredit Group – the required<br />

local support and international developments using significant<br />

synergies. In <strong>2011</strong>, some units <strong>of</strong> s<strong>of</strong>tware devel opment, <strong>of</strong> the<br />

computer operations centre and <strong>of</strong> support functions were outsourced<br />

to Blue IT Services gmbH, a subsidiary <strong>of</strong> IBM <strong>Austria</strong>,<br />

under a cooperation agreement.<br />

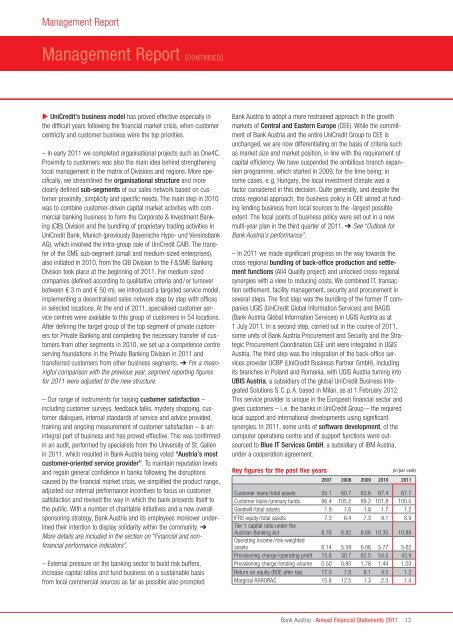

Key figures for the past five years (in per cent)<br />

2007 2008 2009 2010 <strong>2011</strong><br />

Customer loans/total assets 55.1 60.7 63.6 67.4 67.7<br />

Customer loans/primary funds 96.4 105.2 89.2 101.8 100.0<br />

Goodwill/total assets 1.9 1.6 1.8 1.7 1.2<br />

IFRS equity/total assets 7.3 6.4 7.3 9.1 8.9<br />

Tier 1 capital ratio under the<br />

<strong>Austria</strong>n <strong>Bank</strong>ing Act 8.76 6.82 8.68 10.35 10.88<br />

Operating income/risk-weighted<br />

assets 6.14 5.59 6.06 5.77 5.62<br />

Provisioning charge/operating pr<strong>of</strong>it 15.8 30.7 62.5 54.5 43.9<br />

Provisioning charge/lending volume 0.50 0.80 1.78 1.44 1.03<br />

Return on equity (ROE after tax) 17.0 7.8 8.1 4.5 1.2<br />

Marginal RARORAC 15.8 12.5 1.3 2.3 1.4<br />

<strong>Bank</strong> <strong>Austria</strong> · <strong>Annual</strong> <strong>Financial</strong> <strong>Statements</strong> <strong>2011</strong><br />

13