Benchlearning methodology and data gathering template

Benchlearning methodology and data gathering template

Benchlearning methodology and data gathering template

- No tags were found...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

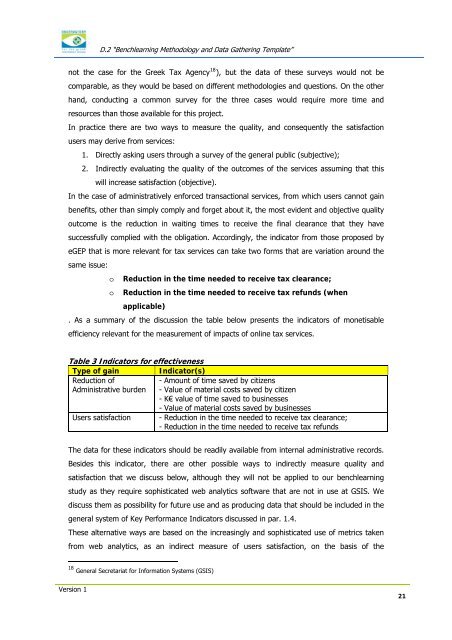

D.2 “<strong>Benchlearning</strong> Methodology <strong>and</strong> Data Gathering Template”not the case for the Greek Tax Agency 18 ), but the <strong>data</strong> of these surveys would not becomparable, as they would be based on different methodologies <strong>and</strong> questions. On the otherh<strong>and</strong>, conducting a common survey for the three cases would require more time <strong>and</strong>resources than those available for this project.In practice there are two ways to measure the quality, <strong>and</strong> consequently the satisfactionusers may derive from services:1. Directly asking users through a survey of the general public (subjective);2. Indirectly evaluating the quality of the outcomes of the services assuming that thiswill increase satisfaction (objective).In the case of administratively enforced transactional services, from which users cannot gainbenefits, other than simply comply <strong>and</strong> forget about it, the most evident <strong>and</strong> objective qualityoutcome is the reduction in waiting times to receive the final clearance that they havesuccessfully complied with the obligation. Accordingly, the indicator from those proposed byeGEP that is more relevant for tax services can take two forms that are variation around thesame issue:o Reduction in the time needed to receive tax clearance;o Reduction in the time needed to receive tax refunds (whenapplicable). As a summary of the discussion the table below presents the indicators of monetisableefficiency relevant for the measurement of impacts of online tax services.Table 3 Indicators for effectivenessType of gainIndicator(s)Reduction of- Amount of time saved by citizensAdministrative burden - Value of material costs saved by citizen- K€ value of time saved to businesses- Value of material costs saved by businessesUsers satisfaction - Reduction in the time needed to receive tax clearance;- Reduction in the time needed to receive tax refundsThe <strong>data</strong> for these indicators should be readily available from internal administrative records.Besides this indicator, there are other possible ways to indirectly measure quality <strong>and</strong>satisfaction that we discuss below, although they will not be applied to our benchlearningstudy as they require sophisticated web analytics software that are not in use at GSIS. Wediscuss them as possibility for future use <strong>and</strong> as producing <strong>data</strong> that should be included in thegeneral system of Key Performance Indicators discussed in par. 1.4.These alternative ways are based on the increasingly <strong>and</strong> sophisticated use of metrics takenfrom web analytics, as an indirect measure of users satisfaction, on the basis of the18 General Secretariat for Information Systems (GSIS)Version 121