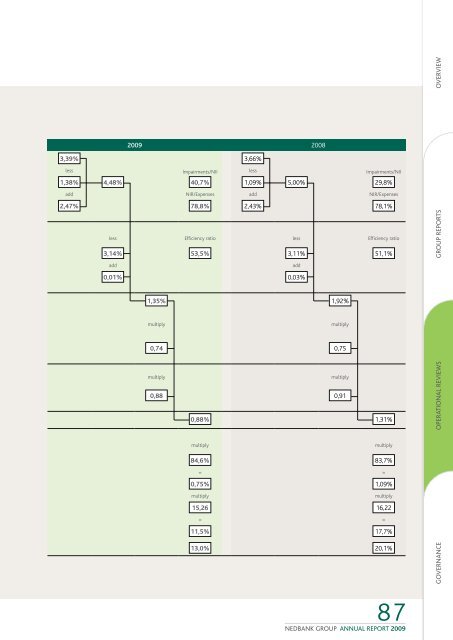

OVERVIEW2009 20083,39%3,66%lessImpairments/NIIlessImpairments/NII1,38%4,48% 40,7%1,09%5,00% 29,8%addNIR/ExpensesaddNIR/Expenses2,47% 78,8% 2,43% 78,1%less Efficiency ratio less Efficiency ratio3,14%53,5% 3,11%51,1%GROUP REPORTSadd0,01% 0,03%add1,35% 1,92%multiplymultiply0,74 0,75multiplymultiply0,88 0,910,88% 1,31%OPERATIONAL REVIEWSmultiply84,6%=0,75%multiply15,26=11,5%13,0%multiply83,7%=1,09%multiply16,22=17,7%20,1%87<strong>NEDBANK</strong> GROUP ANNUAL REPORT 2009GOVERNANCE

CHIEF FINANCIAL OFFICER’S REPORT ... continuedFinancial performanceHeadline earnings decreased by 25,8%from R5 765 million toR4 277 million. Basic earnings declinedby 24,7% to R4 826 million (2008:R6 410 million).Diluted headline earnings per share(EPS) decreased by 29,8% from 1 401cents to 983 cents. Diluted basic EPSdeclined by 28,8% from 1 558 centsto 1 109 cents. These results are in linewith the guidance given in the thirdquartertrading update.A key feature of the year’s performancewas the strengthening of thegroup’s capital ratios, which are nowcomfortably above our target ranges.The core Tier 1 capital adequacy ratioincreased from 8,2% to 9,9%, the Tier1 capital adequacy ratio from 9,6% to11,5% and the total ratio from 12,4%to 14,9%.The group’s ROE, excluding goodwill,decreased from 20,1% to 13,0%.ROE decreased from 17,7% to 11,5%for the year. These declines weredriven primarily by increasing retailimpairment levels and the negativeimpact from lower endowment earningsthat reduced the return on assets,together with strengthened capitallevels as shareholders’ equity growth farexceeded growth in total assets.Strengthening the balance sheet remainsa major focus and we continued to growthe net asset value (NAV) and tangibleNAV per share.An interim dividend of 210 cents pershare and a final dividend of 230 centsper share were declared, maintaining thedividend cover at 2,29 times similar levelsas last year.The interest margin was compressed by27 basis points to 3,39%, which wasslightly better than the 30 to 35 basispoints expected.We saw the credit loss ratio peak inthe first quarter at 167 basis pointsand decrease to 147 basis pointsfor the year-end. Although interestrates decreased by 450 basis pointsduring 2009, unemployment and theweak housing market exacerbatedcredit stress. <strong>Nedbank</strong> Retail’s creditquality deteriorated, with impairmentsworsening significantly, although the rateof new defaults slowed in the second half.Business banking and wholesale bankingimpairments ended the year at betterlevels than originally anticipated.Preprovisioning operating profit, ameasure that shows the underlyingstrength of the franchise beforeimpairments, decreased by 1,6% toR12,1 billion. This shows the significanceof the impact from the higherimpairments and loss of endowment, butdemonstrates the underlying strength ofour business.The NIR/expenses ratio is a new ratio weare tracking. A key focus for the group isto grow NIR as this is an important areawhere we lag our peers.We have therefore set a medium-tolong-termtarget for NIR/expenses ofgreater than 85% and are using thistarget to ensure clusters focus on thismeasure.The efficiency ratio deteriorated to53,5%, mostly as a result of lower NII.Assets under management grew by11,0% to R93,6 billion, primarily throughour domestic asset managementbusiness, which experienced strong netinflows of R7,2 billion on the back ofgood fund performance.Strong growth in the value of newbusiness supported growth of 40,5% inembedded value in Nedgroup Life, dueto good growth in credit life and funeralproducts, as well as improved sales intothe retail home loan base.EP is a measure of earnings afterdeducting the cost of capital. The grouphas increased surplus capital throughthese challenging economic timeseven though it has been impactedby the higher impairments and lowerinterest rates. Overall this led to a smalleconomic loss of R74 million.The bank’s funding and liquidity levelshave remained sound as a resultof an ongoing focus on increasingand strengthening liquidity buffers,lengthening the funding profile,maintaining a low reliance on interbank,foreign and capital markets, as well asrobust balance sheet management. Astrong, broad-based deposit franchisealso provides the group with diversefunding sources.88<strong>NEDBANK</strong> GROUP ANNUAL REPORT 2009