Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

2019 Global Economic and Market Outlook<br />

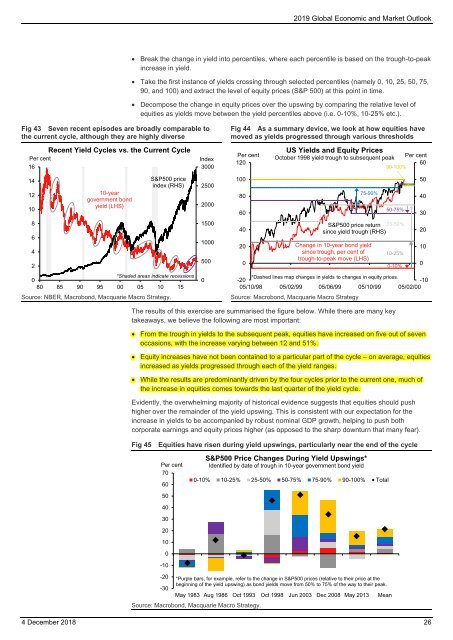

Break the change in yield into percentiles, where each percentile is based on the trough-to-peak<br />

increase in yield.<br />

Take the first instance of yields crossing through selected percentiles (namely 0, 10, 25, 50, 75,<br />

90, and 100) and extract the level of equity prices (S&P 500) at this point in time.<br />

Decompose the change in equity prices over the upswing by comparing the relative level of<br />

equities as yields move between the yield percentiles above (i.e. 0-10%, 10-25% etc.).<br />

Fig 43 Seven recent episodes are broadly comparable to<br />

the current cycle, although they are highly diverse<br />

Recent Yield Cycles vs. the Current Cycle<br />

Per cent<br />

16<br />

Index<br />

3000<br />

Fig 44 As a summary device, we look at how equities have<br />

moved as yields progressed through various thresholds<br />

Per cent<br />

120<br />

US Yields and Equity Prices<br />

October 1998 yield trough to subsequent peak<br />

Per cent<br />

60<br />

90-100%<br />

14<br />

12<br />

10<br />

8<br />

6<br />

4<br />

2<br />

10-year<br />

government bond<br />

yield (LHS)<br />

S&P500 price<br />

index (RHS)<br />

*Shaded areas indicate recessions<br />

0<br />

80 85 90 95 00 05 10 15<br />

Source: NBER, Macrobond, Macquarie Macro Strategy.<br />

2500<br />

2000<br />

1500<br />

1000<br />

500<br />

0<br />

100<br />

80<br />

60<br />

40<br />

20<br />

0<br />

*Dashed lines map changes in yields to changes in equity prices.<br />

-20<br />

-10<br />

05/10/98 05/02/99 05/06/99 05/10/99 05/02/00<br />

Source: Macrobond, Macquarie Macro Strategy<br />

75-90%<br />

S&P500 price return 25-50%<br />

since yield trough (RHS)<br />

Change in 10-year bond yield<br />

since trough, per cent of<br />

trough-to-peak move (LHS)<br />

50-75%<br />

10-25%<br />

0-10%<br />

50<br />

40<br />

30<br />

20<br />

10<br />

0<br />

The results of this exercise are summarised the figure below. While there are many key<br />

takeaways, we believe the following are most important:<br />

From the trough in yields to the subsequent peak, equities have increased on five out of seven<br />

occasions, with the increase varying between 12 and 51%.<br />

Equity increases have not been contained to a particular part of the cycle – on average, equities<br />

increased as yields progressed through each of the yield ranges.<br />

While the results are predominantly driven by the four cycles prior to the current one, much of<br />

the increase in equities comes towards the last quarter of the yield cycle.<br />

Evidently, the overwhelming majority of historical evidence suggests that equities should push<br />

higher over the remainder of the yield upswing. This is consistent with our expectation for the<br />

increase in yields to be accompanied by robust nominal GDP growth, helping to push both<br />

corporate earnings and equity prices higher (as opposed to the sharp downturn that many fear).<br />

Fig 45 Equities have risen during yield upswings, particularly near the end of the cycle<br />

Per cent<br />

70<br />

60<br />

50<br />

S&P500 Price Changes During Yield Upswings*<br />

Identified by date of trough in 10-year government bond yield<br />

0-10% 10-25% 25-50% 50-75% 75-90% 90-100% Total<br />

40<br />

30<br />

20<br />

10<br />

0<br />

-10<br />

-20<br />

-30<br />

*Purple bars, for example, refer to the change in S&P500 prices (relative to their price at the<br />

beginning of the yield upswing) as bond yields move from 50% to 75% of the way to their peak.<br />

May 1983 Aug 1986 Oct 1993 Oct 1998 Jun 2003 Dec 2008 May 2013 Mean<br />

Source: Macrobond, Macquarie Macro Strategy.<br />

4 December 2018 26