ECONOMETRIA

ECONOMETRIA

ECONOMETRIA

SHOW LESS

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

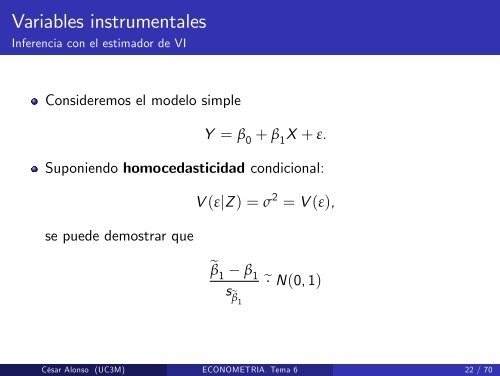

Variables instrumentales<br />

Inferencia con el estimador de VI<br />

Consideremos el modelo simple<br />

Y = β 0 + β 1 X + ε.<br />

Suponiendo homocedasticidad condicional:<br />

se puede demostrar que<br />

V (εjZ ) = σ 2 = V (ε),<br />

eβ 1 β1 seβ 1<br />

e N(0, 1)<br />

César Alonso (UC3M) <strong>ECONOMETRIA</strong>. Tema 6 22 / 70