Finance for Small and Medium-Sized Enterprises - DTI Home Page

Finance for Small and Medium-Sized Enterprises - DTI Home Page

Finance for Small and Medium-Sized Enterprises - DTI Home Page

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>Finance</strong> <strong>for</strong> <strong>Small</strong> <strong>and</strong> <strong>Medium</strong>-<strong>Sized</strong> <strong>Enterprises</strong>: A Report on the 2004 UK Survey of SME <strong>Finance</strong>s<br />

eligible <strong>for</strong><br />

assistance under the SFLG, although further analysis of these businesses’<br />

characteristics<br />

would be required to establish this eligibility.<br />

The high proportion of businesses reporting ‘no reason given’ <strong>for</strong> an overdraft<br />

rejection is notable (25%). Also, the proportion who ‘don’t know’ the reason <strong>for</strong><br />

reject ion is generally high. These findings are indicative of poor communications<br />

between the lender <strong>and</strong> rejected applicant. We can only speculate about the likely<br />

quality of<br />

these businesses.<br />

Impact<br />

of rejection<br />

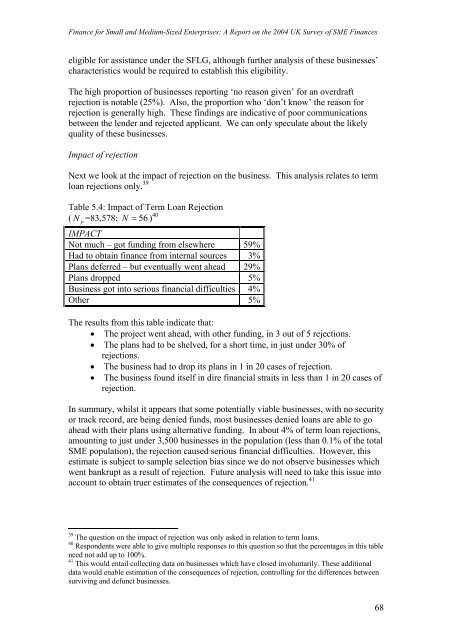

Next we look at the impact of rejection on the business. This analysis relates to term<br />

loan rejections only. 39<br />

Table<br />

5.4: Impact of Term Loan Rejection<br />

40<br />

( N =83,578; N = 56 )<br />

p<br />

IMPACT<br />

Not much – got funding from elsewhere 59%<br />

Had to obtain finance from internal sources 3%<br />

Plans deferred – but eventually went ahead 29%<br />

Plans dropped 5%<br />

Business got into serious financial difficulties 4%<br />

Other 5%<br />

The results from this table indicate that:<br />

• The project went ahead, with other funding, in 3 out of 5 rejections.<br />

• The plans had to be shelved, <strong>for</strong> a short time, in just under 30% of<br />

rejections.<br />

• The business had to drop its plans in 1 in 20 cases of rejection.<br />

• The business found itself in dire financial straits in less than 1 in 20 cases of<br />

rejection.<br />

In summary, whilst it appears that some potentially viable businesses, with no security<br />

or track record, are being denied funds, most businesses denied loans are able to go<br />

ahead with their plans using alternative funding. In about 4% of term loan rejections,<br />

amounting to just under 3,500 businesses in the population (less than 0.1% of the total<br />

SME population), the rejection caused serious financial difficulties. However, this<br />

estimate is subject to sample selection bias since we do not observe businesses which<br />

went bankrupt as a result of rejection. Future analysis will need to take this issue into<br />

account to obtain truer estimates of the consequences of rejection. 41<br />

39<br />

The question on the impact of rejection was only asked in relation to term loans.<br />

40<br />

Respondents were able to give multiple responses to this question so that the percentages in this table<br />

need not add up to 100%.<br />

41<br />

This would entail collecting data on businesses which have closed involuntarily. These additional<br />

data would enable estimation of the consequences of rejection, controlling <strong>for</strong> the differences between<br />

surviving <strong>and</strong> defunct businesses.<br />

68

![Joint Report on Social Protection and Social Inclusion [2005]](https://img.yumpu.com/19580638/1/190x132/joint-report-on-social-protection-and-social-inclusion-2005.jpg?quality=85)