Modelling Dependence with Copulas - IFOR

Modelling Dependence with Copulas - IFOR

Modelling Dependence with Copulas - IFOR

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

2.4 <strong>Copulas</strong> and Random Variables<br />

M<br />

W<br />

Y1<br />

0.0 0.2 0.4 0.6 0.8 1.0<br />

••<br />

••<br />

••<br />

••<br />

•<br />

•<br />

•<br />

•<br />

•<br />

••<br />

••<br />

••<br />

•<br />

•<br />

•<br />

•<br />

•<br />

•<br />

•<br />

•<br />

••<br />

• •<br />

•<br />

•<br />

•<br />

•<br />

•<br />

•<br />

••<br />

•<br />

•<br />

•<br />

•<br />

•<br />

•<br />

•<br />

•<br />

•<br />

•<br />

••<br />

••<br />

•<br />

•<br />

••<br />

•<br />

•<br />

•<br />

•<br />

•<br />

•<br />

Y2<br />

0.0 0.2 0.4 0.6 0.8 1.0<br />

•<br />

••<br />

•<br />

•<br />

•<br />

•<br />

•<br />

•<br />

••<br />

•<br />

•<br />

•<br />

•<br />

•<br />

•<br />

••<br />

•<br />

•<br />

•<br />

•<br />

•• •<br />

•<br />

•<br />

••<br />

•<br />

•<br />

•<br />

•<br />

•<br />

•<br />

•<br />

•<br />

•<br />

•<br />

•<br />

•<br />

•<br />

•<br />

•<br />

•<br />

•<br />

••<br />

•<br />

•<br />

•<br />

••<br />

•<br />

•<br />

•<br />

0.0 0.2 0.4 0.6 0.8 1.0<br />

0.0 0.2 0.4 0.6 0.8 1.0<br />

X1<br />

X2<br />

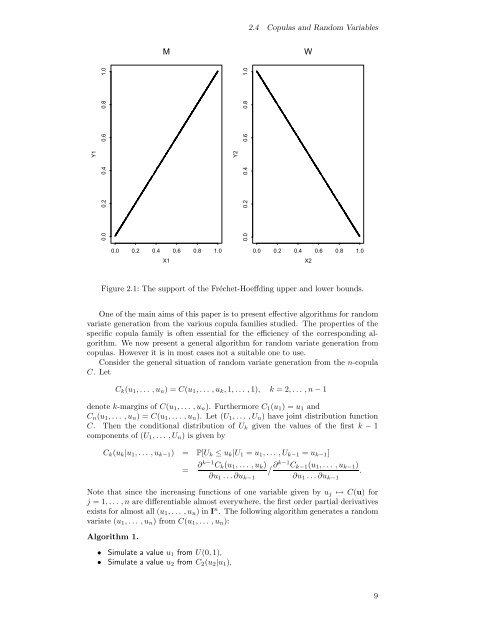

Figure 2.1: The support of the Fréchet-Hoeffding upper and lower bounds.<br />

One of the main aims of this paper is to present effective algorithms for random<br />

variate generation from the various copula families studied. The properties of the<br />

specific copula family is often essential for the efficiency of the corresponding algorithm.<br />

We now present a general algorithm for random variate generation from<br />

copulas. However it is in most cases not a suitable one to use.<br />

Consider the general situation of random variate generation from the n-copula<br />

C. Let<br />

C k (u 1 ,... ,u n )=C(u 1 ,... ,u k , 1,... ,1), k =2,... ,n− 1<br />

denote k-margins of C(u 1 ,... ,u n ). Furthermore C 1 (u 1 )=u 1 and<br />

C n (u 1 ,... ,u n )=C(u 1 ,... ,u n ). Let (U 1 ,... ,U n ) have joint distribution function<br />

C. Then the conditional distribution of U k given the values of the first k − 1<br />

components of (U 1 ,... ,U n )isgivenby<br />

C k (u k |u 1 ,... ,u k−1 ) = P[U k ≤ u k |U 1 = u 1 ,... ,U k−1 = u k−1 ]<br />

= ∂k−1 C k (u 1 ,... ,u k ) /∂ k−1 C k−1 (u 1 ,... ,u k−1 )<br />

.<br />

∂u 1 ...∂u k−1 ∂u 1 ...∂u k−1<br />

Note that since the increasing functions of one variable given by u j ↦→ C(u) for<br />

j =1,... ,n are differentiable almost everywhere, the first order partial derivatives<br />

exists for almost all (u 1 ,... ,u n )inI n . The following algorithm generates a random<br />

variate (u 1 ,... ,u n ) from C(u 1 ,... ,u n ):<br />

Algorithm 1.<br />

• Simulate a value u 1 from U(0, 1),<br />

• Simulate a value u 2 from C 2 (u 2 |u 1 ),<br />

9