Modelling Dependence with Copulas - IFOR

Modelling Dependence with Copulas - IFOR

Modelling Dependence with Copulas - IFOR

SHOW LESS

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

9.2 The Perfect Storm<br />

30<br />

25<br />

Expected Shortfall<br />

20<br />

15<br />

10<br />

5<br />

0.9 0.91 0.92 0.93 0.94 0.95 0.96 0.97 0.98 0.99 1<br />

q<br />

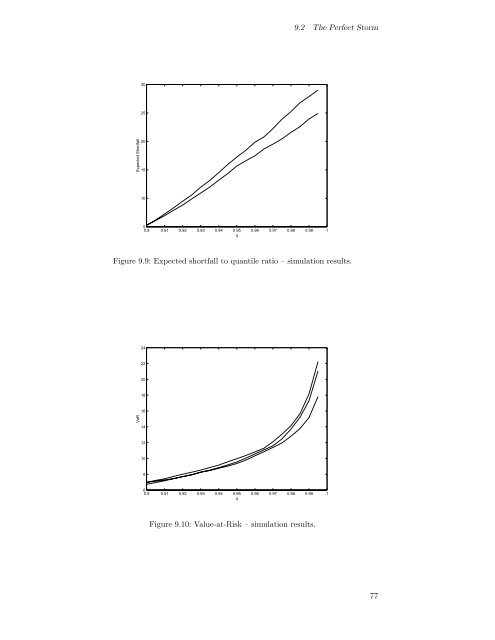

Figure 9.9: Expected shortfall to quantile ratio – simulation results.<br />

24<br />

22<br />

20<br />

18<br />

16<br />

VaR<br />

14<br />

12<br />

10<br />

8<br />

6<br />

0.9 0.91 0.92 0.93 0.94 0.95 0.96 0.97 0.98 0.99 1<br />

q<br />

Figure 9.10: Value-at-Risk – simulation results.<br />

77