Modelling dependence in finance using copulas - Thierry Roncalli's ...

Modelling dependence in finance using copulas - Thierry Roncalli's ...

Modelling dependence in finance using copulas - Thierry Roncalli's ...

SHOW LESS

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

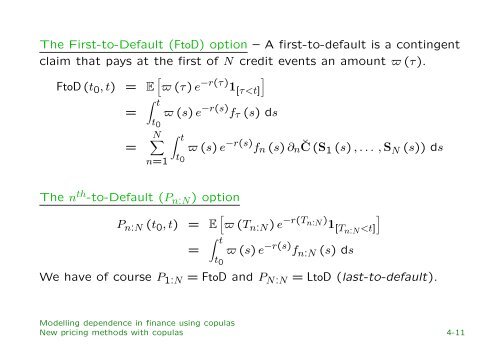

The First-to-Default (FtoD) option – A first-to-default is a cont<strong>in</strong>gent<br />

claim that pays at the first of N credit events an amount ϖ (τ).<br />

FtoD (t 0 , t) = E [ ϖ (τ) e −r(τ) ]<br />

1 [τ