The Inflation Cycle of 2002 to 2015 - Uhlmann Price Securities

The Inflation Cycle of 2002 to 2015 - Uhlmann Price Securities

The Inflation Cycle of 2002 to 2015 - Uhlmann Price Securities

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

Industrial Portfolio Strategy<br />

<strong>The</strong> <strong>Inflation</strong> <strong>Cycle</strong> <strong>of</strong> <strong>2002</strong> <strong>to</strong> <strong>2015</strong> ⎯ April 19, <strong>2002</strong> -31- Legg Mason Wood Walker, Inc.<br />

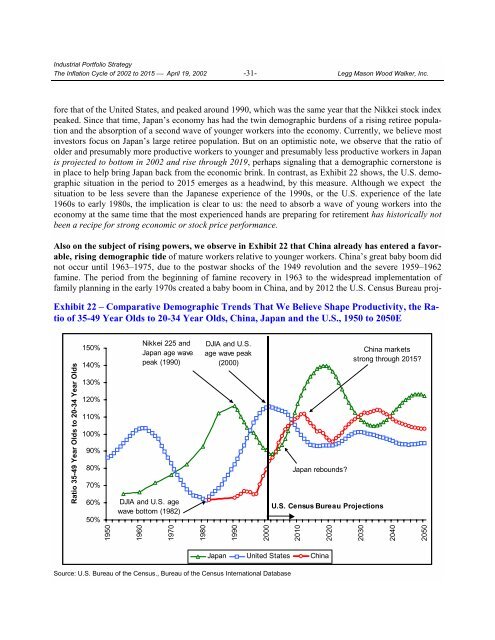

fore that <strong>of</strong> the United States, and peaked around 1990, which was the same year that the Nikkei s<strong>to</strong>ck index<br />

peaked. Since that time, Japan’s economy has had the twin demographic burdens <strong>of</strong> a rising retiree population<br />

and the absorption <strong>of</strong> a second wave <strong>of</strong> younger workers in<strong>to</strong> the economy. Currently, we believe most<br />

inves<strong>to</strong>rs focus on Japan’s large retiree population. But on an optimistic note, we observe that the ratio <strong>of</strong><br />

older and presumably more productive workers <strong>to</strong> younger and presumably less productive workers in Japan<br />

is projected <strong>to</strong> bot<strong>to</strong>m in <strong>2002</strong> and rise through 2019, perhaps signaling that a demographic corners<strong>to</strong>ne is<br />

in place <strong>to</strong> help bring Japan back from the economic brink. In contrast, as Exhibit 22 shows, the U.S. demographic<br />

situation in the period <strong>to</strong> <strong>2015</strong> emerges as a headwind, by this measure. Although we expect the<br />

situation <strong>to</strong> be less severe than the Japanese experience <strong>of</strong> the 1990s, or the U.S. experience <strong>of</strong> the late<br />

1960s <strong>to</strong> early 1980s, the implication is clear <strong>to</strong> us: the need <strong>to</strong> absorb a wave <strong>of</strong> young workers in<strong>to</strong> the<br />

economy at the same time that the most experienced hands are preparing for retirement has his<strong>to</strong>rically not<br />

been a recipe for strong economic or s<strong>to</strong>ck price performance.<br />

Also on the subject <strong>of</strong> rising powers, we observe in Exhibit 22 that China already has entered a favorable,<br />

rising demographic tide <strong>of</strong> mature workers relative <strong>to</strong> younger workers. China’s great baby boom did<br />

not occur until 1963–1975, due <strong>to</strong> the postwar shocks <strong>of</strong> the 1949 revolution and the severe 1959–1962<br />

famine. <strong>The</strong> period from the beginning <strong>of</strong> famine recovery in 1963 <strong>to</strong> the widespread implementation <strong>of</strong><br />

family planning in the early 1970s created a baby boom in China, and by 2012 the U.S. Census Bureau proj-<br />

Exhibit 22 – Comparative Demographic Trends That We Believe Shape Productivity, the Ratio<br />

<strong>of</strong> 35-49 Year Olds <strong>to</strong> 20-34 Year Olds, China, Japan and the U.S., 1950 <strong>to</strong> 2050E<br />

Ratio 35-49 Year Olds <strong>to</strong> 20-34 Year Olds<br />

150%<br />

140%<br />

130%<br />

120%<br />

110%<br />

100%<br />

90%<br />

80%<br />

70%<br />

60%<br />

50%<br />

Nikkei 225 and<br />

Japan age wave<br />

peak (1990)<br />

DJIA and U.S. age<br />

wave bot<strong>to</strong>m (1982)<br />

DJIA and U.S.<br />

age wave peak<br />

(2000)<br />

Japan rebounds?<br />

U.S. Census Bureau Projections<br />

China markets<br />

strong through <strong>2015</strong>?<br />

1950<br />

1960<br />

1970<br />

1980<br />

1990<br />

2000<br />

2010<br />

2020<br />

2030<br />

2040<br />

2050<br />

Japan United States China<br />

Source: U.S. Bureau <strong>of</strong> the Census., Bureau <strong>of</strong> the Census International Database