MacroeconomicsI_working_version (1)

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

Introduction into Macroeconomics 7<br />

Abstractions – We must bear in minds that economic principles, or theories, are<br />

simplifications (abstractions), which exclude irrelevant facts and circumstances. Such<br />

models cannot to depict the full complexity of the real world. The very process of sorting<br />

out and analysing facts involves simplification and removal of clutter.<br />

Economic principles and theories present meaningful statements about economic<br />

behaviour of the economy. Economic principles could be explained as tendencies of<br />

average or typical consumers, workers, or firms. Accordingly economic principles are<br />

generalisations associated with economic behaviour of individuals or with the economy as<br />

a whole.<br />

For example, when economists say that increase in personal income causes the rise in<br />

consumer spending, it is obvious that some households may save all of an increase in their<br />

incomes (and not to spend it). However, in general - on average, and for the entire<br />

economy, spending rises when income increases.<br />

Ceteris Paribus – “Other Things Equal” Assumption is used for creation of economic<br />

generalisations. They are based on assumption that all other variables apart from those<br />

under consideration remain unchanged (constant).<br />

1.5. The Use of Economic Models<br />

In economics we often use the simplified theories called models. Models examine the<br />

relations among economic variables (often in mathematical terms). The real world is full of<br />

complexity and the sense of models is to help us to omit the irrelevant details, remove<br />

clutter and to focus on relevant economic connections and relations. The function of<br />

models is to make things clear and understandable.<br />

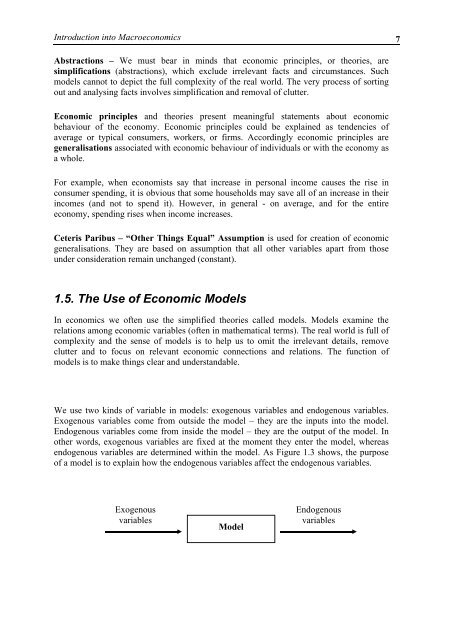

We use two kinds of variable in models: exogenous variables and endogenous variables.<br />

Exogenous variables come from outside the model – they are the inputs into the model.<br />

Endogenous variables come from inside the model – they are the output of the model. In<br />

other words, exogenous variables are fixed at the moment they enter the model, whereas<br />

endogenous variables are determined within the model. As Figure 1.3 shows, the purpose<br />

of a model is to explain how the endogenous variables affect the endogenous variables.<br />

Exogenous<br />

variables<br />

Model<br />

Endogenous<br />

variables